Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- HARKER SAYS FED SHOULD STOP WITH US SMALL BUSINESSES STRUGGLING - BBG

- BIDEN SET TO VISIT ISRAEL WEDNESDAY TO SHOW SOLIDARITY WITH ALLY - BBG

- BORROWING UNDERSHOOT, NO ROOM FOR UK TAX CUTS - IFS - MNI BRIEF

- BOJ TO AVOID INFLATION SIGNAL AS WAGE DATA AWAITED - MNI POLICY

- NZ CPI SLOWS BELOW RBNZ, MARKET EXPECTATIONS - MNI BRIEF

- DATA, STAFF FORECASTS KEY TO NOVEMBER - RBA MINUTES - MNI BRIEF

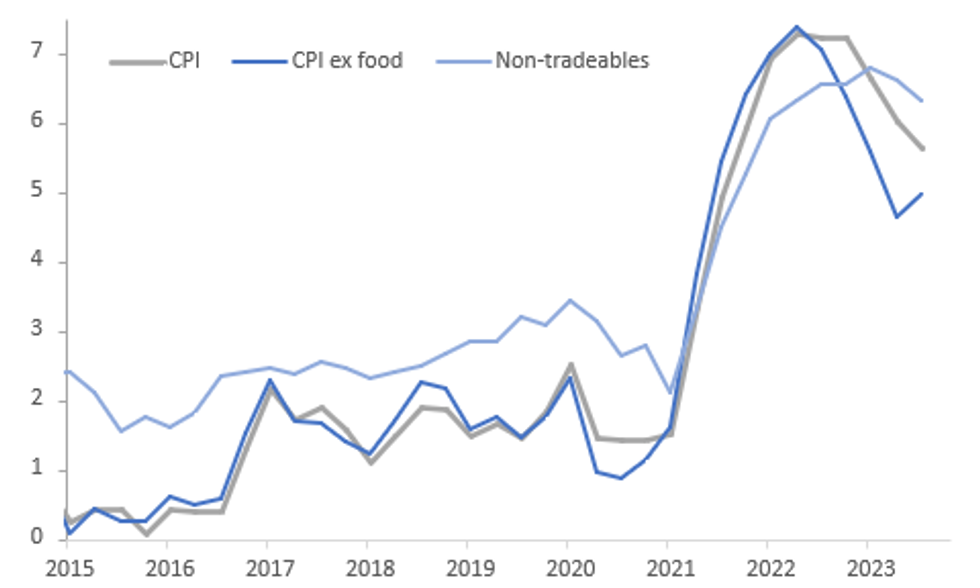

Fig. 1: NZ Q3 CPI Weaker Than Forecast

Source: MNI - Market News/Bloomberg

U.K:

FISCAL (MNI BRIEF): UK public sector borrowing is on track to come in around GBP20 billion below the official forecasts in the 2023-24 fiscal year, but borrowing in subsequent years will be a little higher than predicted and there is no room for tax cuts in the UK budget next month, according to the Institute for Fiscal Studies.

JOBS (BBG): Rolls-Royce Holdings Plc is poised to announce the deepest job cuts under Chief Executive Officer Tufan Erginbilgic as he streamlines the UK manufacturer to prepare for an upswing in demand for large aircraft engines.

COMMERCIAL PROPERTY (BBG): The number of soured commercial real estate loans has begun to rise in the UK as the rapid increase in interest rates feeds through to property valuations.

EUROPE

ECB (MNI): ECB member Philip Lane has been speaking in an interview with Het Financieele Dagblad where he emphasised the data dependent nature of the ECB and highlighted the global uncertainties currently present. Lane described the economy as being ‘pretty stagnant’ for the rest of this year and stated the ECB will remain on guard for an extended period.

ECB (BBG): The European Central Bank is watching the oil price for any inflationary impact from the Israel-Hamas conflict, President Christine Lagarde told euro-area finance ministers, according to people familiar with the matter. Lagarde spoke at a closed-door meeting of the bloc’s officials on Monday in Luxembourg, said the people, speaking on condition of anonymity. An ECB spokesman declined to comment.

U.S.

US/ISRAEL (BBG): President Joe Biden will travel to Israel Wednesday, in a visit designed to signal US solidarity with its closest Middle East ally and help prevent the conflict from engulfing the region.

FED (BBG): The Federal Reserve shouldn’t be thinking about additional interest-rate increases with so many US small businesses struggling to cope with its tightening to date, Philadelphia Fed President Patrick Harker said.

OTHER

JAPAN (MNI): The Bank of Japan wants to avoid sending a message about the timing of any move away from ultra-easy policy with its upcoming Outlook Report inflation forecast, and even if its core projection is raised it will stress growing uncertainty over wages and the global economy, MNI understands.

AUSTRALIA (MNI BRIEF): The Reserve Bank of Australia Board noted updated data on economic activity, inflation and the labour market, alongside a set of revised staff forecasts, will factor heavily into its Nov 4 cash rate decision, according to the minutes of its Oct 3 meeting published Tuesday.

AUSTRALIA/CHINA (RTRS): Australian Prime Minister Anthony Albanese said on Tuesday he remained "very hopeful of a breakthrough" in a trade dispute with China over wine tariffs, as a deadline for the publication of a World Trade Organization ruling nears.

NEW ZEALAND (MNI BRIEF): New Zealand’s Consumer Price Index rose 5.6% y/y in the September quarter, down from Q2’s 6%, and below the market’s 5.9% expectation, and the Reserve Bank of New Zealand’s 6.0% forecast published in its last Monetary Policy Statement, Stats NZ data showed Tuesday.

SOUTH KOREA (YONHAP/BBG): South Korea, US and Japan governments have completed setting up a trilateral communication hotline that was agreed at the Aug. summit at Camp David, Yonhap News says, citing an unidentified Korean government official.

CHINA

CREDIT (SHANGHAI SECURITIES/BBG): China is expected to continue boosting credit toward the end of this year to help drive economic recovery, Shanghai Securities News reports, citing analysts.

INFRASTRUCTURE (EID/BBG): China had 162 so-called “urban village” projects on record, Eco. Information Daily reports, citing data from Ministry of Housing and Urban-Rural Development.

CHINA/RUSSIA (BBG): President Vladimir Putin has arrived in Beijing, according to Chinese state media, a rare trip abroad for the Russian leader who has an arrest warrant issued against him by the International Criminal Court for alleged war crimes in Ukraine.

PROPERTY (RTRS): Country Garden's entire offshore debt will be deemed to be in default if China's largest property developer fails to make a $15 million coupon payment on Tuesday, the end of a 30-day grace period.Non-payment of this tranche is set to trigger cross defaults in other bonds as is standard in bond contracts.

CHINA MARKETS

MNI: PBOC Injects Net CNY4 Bln Via OMO Tues; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY71 billion via 7-day reverse repo on Tuesday, with the rate unchanged at 1.80%. The operation has led to a net injection of CNY4 billion after offsetting the maturity of CNY67 billion reverse repos today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8032% at 09:26 am local time from the close of 1.8087% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 41 on Monday, compared with the close of 42 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium

PBOC Yuan Parity Lower At 7.1796 Tuesday Vs 7.1798 Monday.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1796 on Tuesday, compared with 7.1798 set on Monday. The fixing was estimated at 7.3028 by Bloomberg survey today.

MARKET DATA

SOUTH KOREA SEP IMPORT PRICES M/M 2.9%; PRIOR 4.2%

SOUTH KOREA SEP IMPORT PRICES Y/Y -9.6%; PRIOR -9.2%

SOUTH KOREA SEP EXPORT PRICES M/M 1.7%; PRIOR 4.2%

SOUTH KOREA SEP EXPORT PRICES Y/Y -8.9%; PRIOR -7.9%

SOUTH KOREA AUG MONEY SUPPLY M2 SA M/M 0.2%; PRIOR 0.7%

NEW ZEALAND Q3 CPI Q/Q 1.8%; MEDIAN 1.9%; PRIOR 1.1%

NEW ZEALAND Q3 CPI Y/Y 5.6%; MEDIAN 5.9%; PRIOR 6.0%

NEW ZEALAND Q3 CPI NON-TRADABLE Q/Q 1.7%; MEDIAN 1.8%; PRIOR 1.3%

NEW ZEALAND Q3 CPI TRADABLE Q/Q 1.8%; MEDIAN 2.4%; PRIOR 0.8%

JAPAN AUG TERTIARY INDUSTRY INDEX M/M -0.1%; MEDIAN 0.3%; PRIOR 0.9%

MARKETS

US TSYS: Pressured In Asia

TYZ3 deals at 107-00+, -0-06, a 0-10 range has been observed on volume of ~153k.

- Cash tsys sit 1-5bps cheaper across the major benchmarks, the curve has bear steepened.

- Tsys were pressured in the Asian session on spillover from ACGBs, in lieu of the minutes of the RBA October policy meeting.

- Losses extended through the session alongside US Equity futures ticking lower and the USD firming. TY broke support at 107-02+ and the next support level is 106-03+, low from Sep 4.

- Fedpseak from Harker crossed early in today's Asian session, he noted that the Fed shouldn't be thinking about rate increases as many small businesses are struggling with the tightening to date.

- The data docket is relatively light in Europe today, further out we have retail sales, business inventories and industrial production. Fedpeak from NY Fed President Williams, Gov Bowman and Richmond Fed President Barkin is due.

JGBS: Futures At Tokyo Session Cheaps & Curve Steepens After Poor Absorption Of 20Y Supply

JGB futures are cheaper, -28 compared to settlement levels, after pushing to Tokyo session lows following the results of today’s 20-year supply. 20-year supply saw poor digestion as the low-price printed below dealer expectations and the cover ratio at 2.973x declined sharply versus 3.942x at last month’s auction. The auction tail also lengthened dramatically.

- The local calendar was light today, with the Tertiary Industry Index (-0.1% m/m vs. +0.3% est. and +1.1% prior) as the sole release.

- In addition to domestic supply concerns, local participants have likely eyed US tsys in the Asia-Pac session after the bear-steepening observed during the NY session. Cash US tsys are flat to 5bps cheaper, with the curve steeper.

- The cash JGB curve has bear-steepened today, with yields 0.3bp to 5.2bps higher. The benchmark 10-year yield is 1.6bps higher at 0.777% versus the cycle high of 0.814%.

- The 20-year JGB is dealing 4-5bps cheaper at 1.598%, just shy of the cycle high of 1.606%, in post-auction dealings.

- The swaps curve has also bear-steepened, with rates 0.5bp lower to 6.6bps higher. Swap spreads are mixed across maturities.

- Tomorrow, the local calendar is light again, with Tokyo Condominiums for Sale data as the only release.

AUSSIE BONDS: Sharply Cheaper Post-RBA Minutes, US Tsys Extend Bear-Steepening In Asia-Pac Dealings

ACGBs (YM -14.0 & XM -9.5) sit sharply cheaper and at Sydney session lows. The weak performance can be attributed to both domestic and offshore factors.

- On the domestic front, the minutes from the October RBA meeting showed that the Board had discussed both leaving rates unchanged and a 25bp hike but it felt that there hadn’t been “sufficient new information” to warrant tightening policy further. But November is clearly live as there will be updated forecasts and more data (Q3 CPI on October 25).

- Abroad, US tsys have extended the bear-steepening observed in yesterday’s NY session into today’s Asia-Pac session. Cash US tsy yields are flat to 5bps higher in recent dealings, with the curve steeper.

- Cash ACGBs are 9-13bps cheaper, with the AU-US 10-year yield differential unchanged higher at -19bps.

- Swap rates are 10-13bps higher, with EFPs slightly wider.

- The bills strip has sharply bear-steepened, with pricing -6 to -16.

- RBA-dated OIS pricing is 4-15bps firmer across meetings, with terminal rate expectations 8bps firmer at 4.29%.

- Tomorrow, the local calendar sees a Fireside chat with RBA Governor Bullock at the AFSA Annual Summit Panel.

- The AOFM announced today that a new 4.75% Jun-54 bond had been issued via syndication and priced at a yield to maturity of 4.93%. The issue size was A$8bn.

NZGBS: Post-CPI Rally Held Into The Close, Outperforms The $-Bloc

NZGBs closed with a twist-steepening of the curve. Yields closed 3bps lower to 3bps higher on the day and 1-4bps lower than pre-CPI levels after Q3 data printed on the downside of expectations. Headline CPI showed +1.8% q/q and +5.6% y/y versus estimates of +1.9% and +5.9% and prior +1.1% and +6.0%.

- Tradable and non-tradeable inflation also printed on the downside of expectations at +1.7% q/q and +1.8% q/q respectively versus estimates of +1.8% and +2.4% and prior +1.3% and +0.8%.

- NZ-US and NZ-AU 10-year yield differentials closed 5bps tighter on the day at +68bps and +87bps respectively.

- Non-Resident Bond Holdings dipped to 62.1% in September from 62.4% in August.

- The post-CPI rally defied the prevailing bearish mood in today's Asia-Pac session. US tsys are flat to 3bps cheaper compared to their NY closing levels.

- Swap rates closed 1-9bps lower than pre-CPI levels. The 2s10s curve twist-steepened on the day, with rates 5bps lower to 4bps higher.

- RBNZ dated OIS pricing shunted 5-9bps softer in post-CPI dealings, with terminal OCR expectations 7bps softer on the day at 5.65%.

- Tomorrow, the local calendar is empty. The next key release will be the September Trade Balance data on Friday.

FOREX: Kiwi Pressured In Asia

The Kiwi has been pressured on Tuesday after Q3 CPI, NZD/USD is down ~0.4% and sits a touch above the $0.59 handle. Technically we remain in a downtrend, bears look to break the YTD low at $0.5860. AUD/NZD is ~0.6% firmer, bulls now target a move above the $1.08 handle and 200-Day EMA ($1.0822).

- Elsewhere in G-10; AUD/USD is up ~0.2% and sits at $0.6350/55. The pair firmed post the RBA minutes, the bank noted that it had considered two options at the October meeting hiking or staying on hold. The option to stay on hold provided the more compelling case with the updated forecasts and data available ahead of the November meeting.

- Yen is a touch softer however ranges have been narrow thus far. Resistance in USD/JPY remains at ¥150.16, Oct 3 high and bull trigger. Support is at the 20-Day EMA (¥148.74).

- EUR and GBP are marginally lower and BBDXY is up ~0.1%.

- US Tsy Yields are a touch firmer across the curve. US Equity Futures are lower, e-minis are down ~0.2%. Oil is a touch lower.

- In Europe today we have the UK Earnings Data and the latest ZEW Survey from Germany.

EQUITIES: Asia Pac Shares Tracking Higher

Regional equities are higher across the board, taking a positive cue from US market gains on Monday. Most markets are seeing gains of less than 1% (although the Kospi sits +1.15% higher). US equity futures are down a touch in the first part of Tuesday trade, but losses are modest and haven't impacted broader risk appetite. Eminis were last near 4396, down 0.11%, while Nasdaq futures are off by a similar amount.

- US President Biden will travel to Israel on Wednesday as part of a broader trip to the Middle East to show both support to Israel but also prevent the conflict from broadening (see this BBG link).

- Lack of escalation in the conflict over the past week has been a factor cited as aiding risk appetite in recent sessions. US yields continue to recover ground, but this isn't meaningfully impacting the equity space yet.

- At the break, the HSI is up 0.70%, while the CSI 300 has firmed 0.46%. China state owned companies have revealed plans to buy back shares late on Monday (see this link). This is a positive, although the CSI 300 is only modestly above recent cyclical lows. Tomorrow, we get Q3 GDP data and September activity figures.

- Japan's Topix is up 0.60%, while the Nikkei 225 has firmed 1.0%. The South Korean Kospi is outperforming, up 1.15%. Samsung shares have outperformed.

- In SEA, most indices are higher, but Philippine shares are the standout, up a little over 1% at this stage.

OIL: Prices Tentatively Trend Lower As Monitoring Middle East Developments

Oil prices have been trending marginally lower during APAC trading today but are off intraday lows. WTI is down 0.2% to $86.50/bbl after falling to $86.11 earlier. Brent has traded below $90 today but is steady at $89.65 after a low of $89.22. The USD index is flat. Later US API crude and product inventory data are published.

- Oil has moderated in recent sessions driven by hopes that conflict in Israel/Gaza won’t spread on the back of US efforts to contain it. Secretary of State Blinken spoke to leaders in the region including Saudi Arabia and returned to Israel. In the interests of containment, President Biden is due to visit Israel and Jordan on Wednesday to speak with not only Israeli PM Netanyahu but also Jordanian King Abdullah II, Egyptian President el-Sisi and President Abbas of the State of Palestine.

- Biden’s visit comes at a crucial time after Iranian foreign minister Amirabdollahian said yesterday that “time for political solutions is running out” and the expansion of the war is “approaching the inevitable stage”, Bloomberg is reporting. There has also been unofficial communication between the US and Iran. The main risk to oil is if Iran directly joins the conflict or if it retaliates to a tightening of sanctions by blocking the Strait of Hormuz. Prices seem in “wait-and-see” mode.

- Talks continue to allow fair elections in Venezuela which would allow an easing of sanctions on its oil exports.

- Later the Fed’s Williams, Bowman, Barkin and Kashkari speak and US September retail sales, IP and NAHB housing index are released. The ECB’s de Guindos also appears and UK labour market data and Canadian September CPI print.

GOLD: Lower Despite A Weaker USD, Higher US Yields Weigh As Haven Demand Tapers

Gold is 0.2% lower in the Asia-Pac session, after closing 0.7% lower at $1920.20 on Monday. A softer USD provided little support for bullion after its strong push higher over recent days. Indeed, according to MNI’s technicals team, gold’s strong circa $60 increase on Friday has left it elevated compared to support at $1898.3 (50-day EMA).

- Higher US Treasury yields likely weighed on the yellow metal. US Treasury yields finished 5-11bps cheaper across the major benchmarks, with the curve steeper. Monday’s move reversed the bull flattening seen on Friday. Although geopolitical tensions remain high the reversal is attributed to no further escalation in the Israel/Hamas conflict as of yet.

- Moreover, President Joe Biden is set to travel to Israel on Wednesday. The visit is designed to signal US solidarity with its closest Middle East ally and prevent the conflict from widening.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/10/2023 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 17/10/2023 | 0900/1100 | *** |  | DE | ZEW Current Conditions Index |

| 17/10/2023 | 0900/1100 | *** | | DE | ZEW Current Expectations Index |

| 17/10/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 17/10/2023 | 1200/0800 |  | US | New York Fed's John Williams | |

| 17/10/2023 | - |  | EU | ECB's de Guindos attends Luxembourg Ecofin meeting | |

| 17/10/2023 | 1230/0830 | * |  | CA | International Canadian Transaction in Securities |

| 17/10/2023 | 1230/0830 | *** | | CA | CPI |

| 17/10/2023 | 1230/0830 | *** | | US | Retail Sales |

| 17/10/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 17/10/2023 | 1315/0915 | *** | | US | Industrial Production |

| 17/10/2023 | 1320/0920 | | US | Fed Governor Michelle Bowman | |

| 17/10/2023 | 1400/1000 | ** | | US | NAHB Home Builder Index |

| 17/10/2023 | 1400/1000 | * | | US | Business Inventories |

| 17/10/2023 | 1445/1045 | | US | Richmond Fed's Tom Barkin | |

| 17/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 17/10/2023 | 1700/1900 | | EU | ECB's De Guindos Speech at Conference | |

| 17/10/2023 | 2000/1600 | ** | | US | TICS |

| 17/10/2023 | 2100/1700 | | US | Minneapolis Fed's Neel Kashkari |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.