Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- BIDEN: ‘UNLIKELY’ MISSILE THAT HIT POLAND FIRED FROM RUSSIA (AP)

- RUSSIA'S DEFENCE MINISTRY DENIES RUSSIAN MISSILES STRUCK POLISH TERRITORY (RTRS)

- POLAND LIKELY TO INVOKE NATO'S ARTICLE 4, WILL RAISE MISSILE BLAST WITH UN – OFFICIALS (RTRS)

- DONALD TRUMP, TWICE IMPEACHED AND UNDER FBI INVESTIGATION, LAUNCHES 2024 WHITE HOUSE BID (CNBC)

- FED’S BARR WARNS US ECONOMY WILL SEE ‘SIGNIFICANT’ SOFTENING (BBG)

- ECB WILL INCREASE INTEREST RATES FURTHER, HOLZMANN SAYS (BBG)

- ECB’S STOURNARAS: PACE OF RATES ADJUSTMENT SHOULD BE PRUDENT (BBG)

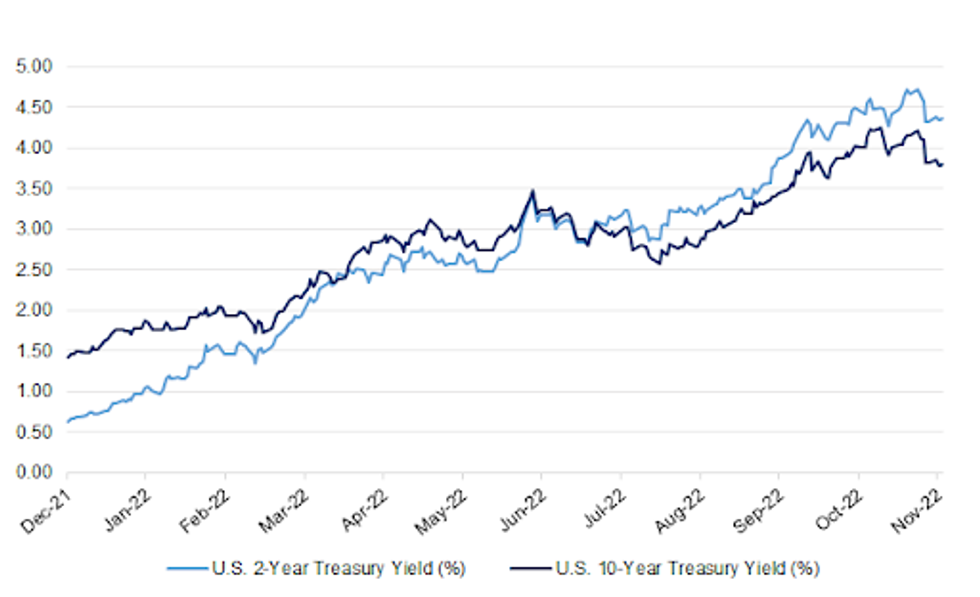

Fig. 1: U.S. 2- & 10-Year Treasury Yields

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

FISCAL/POLITICS: Chancellor Jeremy Hunt has repeatedly warned that his Autumn Statement on Thursday will be “eye-wateringly” difficult. Less has been said about how he hopes to turn this bleak exercise in fiscal discipline into a platform for a Conservative election victory in 2024. (FT)

ECONOMY: Rishi Sunak has told the UK’s top executives to rein in their pay as their workers face a cost of living crisis — but he criticised demands by nurses for a double-digit pay increase. Speaking at the G20 summit in Indonesia, the UK prime minister said: “I would say to executives to embrace pay restraint at a time like this and make sure they are also looking after all their workers.” (FT)

EUROPE

ECB: The European Central Bank will continue to increase borrowing costs, according to Governing Council member Robert Holzmann. “We’ve recently raised interest rates strongly,” he said in Vienna on Tuesday. “We will raise interest rates further.” (BBG)

ECB: “A prudent pace of adjustment is warranted in the euro area,” regarding rate hikes ECB’s, Governing Council member Yannis Stournaras says at an event in Athens. (BBG)

SNB: The Swiss National Bank gave another strong hint it will raise interest rates again, when Chairman Thomas Jordan on Tuesday said current monetary policy was too loose to tackle inflation in Switzerland. "Monetary policy is still expansionary and we have most likely to adjust monetary policy again," Jordan told an event in Zurich on Tuesday. (RTRS)

U.S.

FED: Federal Reserve Vice Chair for Supervision Michael Barr cautioned the US economy would take a hit as the central bank confronts high inflation. (BBG)

FISCAL: The White House is asking Congress to approve $37.7 billion in additional aid for Ukraine during the post-election session, according to administration officials, as Republican lawmakers vow to more closely scrutinize US funding for the country. (BBG)

POLITICS: Former President Donald Trump announced Tuesday night that he was running for president in 2024, laying out an aggressively conservative agenda that includes executing people convicted of dealing drugs. (CNBC)

POLITICS: Senate Minority Leader Mitch McConnell (R-Ky.) and House Minority Leader Kevin McCarthy (R-Calif.) have been drawn into battles for control over their respective conferences, inflaming a GOP civil war that's getting uglier by the hour. (Axios)

EQUITIES: Elon Musk’s Twitter is on a “collision course” with Brussels, as the social media platform faces new scrutiny under landmark EU laws to police Big Tech that come into force on Wednesday. (FT)

OTHER

GLOBAL TRADE: Apple Inc. is preparing to begin sourcing chips for its devices from a plant under construction in Arizona, marking a major step toward reducing the company’s reliance on Asian production. (BBG)

GLOBAL TRADE: October volume at the busiest U.S. seaport fell to its lowest level since 2009 as shippers sent cargo to alternate trade gateways to avoid potential disruptions from ongoing West Coast port labor talks, Port of Los Angeles Executive Director Gene Seroka said on Tuesday. (RTRS)

GLOBAL TRADE: The head of the World Trade Organization (WTO) warned on Wednesday that several major economies face a real risk of sliding into recession as the war in Ukraine, rising food and fuel costs, and soaring inflation cloud the global outlook. (RTRS)

U.S./CHINA: A few weeks after House Speaker Nancy Pelosi‘s August visit to Taiwan, advisers to President Biden quietly opened back-channel talks with a senior Chinese diplomat. Beijing had largely severed lines of communication with the U.S. government, and the two sides were looking for a way forward. (WSJ)

U.S./CHINA: U.S. Vice President Kamala Harris will visit the Philippine islands of Palawan in the South China Sea, a senior administration official said on Tuesday, in a move that may be interpreted by Beijing as a sharp rebuke. (RTRS)

U.S./CHINA: U.S. Treasury Secretary Janet Yellen met for two hours of talks with China's central bank governor Yi Gang on Wednesday at the G20 summit in Bali, a U.S. treasury official said. (RTRS)

U.S./CHINA: Federal Bureau of Investigation Director Christopher Wray told lawmakers Tuesday that he is “extremely concerned” about TikTok’s operations in the U.S. (CNBC)

AUSTRALIA: Australia should keep tightening monetary and fiscal policy to help cool domestic demand and keep inflation expectations in check, the International Monetary Fund said. (BBG)

BRAZIL: Central Bank President Roberto Campos Neto said Tuesday that although much of the recent improvement in inflation is the result of government measures, “leading indicators show a qualitative improvement.” (BBG)

RUSSIA: President Joe Biden said Wednesday it was “unlikely” that a missile that killed two in NATO-ally Poland was fired from Russia, but he pledged support for Poland’s investigation into what it had called a “Russian-made” missile. (AP)

RUSSIA: Russia's defence ministry on Tuesday denied reports that Russian missiles had hit Polish territory, describing them as "a deliberate provocation aimed at escalating the situation". (RTRS)

RUSSIA: Poland has no conclusive evidence showing who fired the missile that caused an explosion in a village near the Ukrainian border, the president said on Wednesday, adding that Warsaw remained calm in the face of what he described as a "one-off" incident. (RTRS)

RUSSIA: Three U.S. officials said preliminary assessments suggested the missile was fired by Ukrainian forces at an incoming Russian one amid the crushing salvo against Ukraine’s electrical infrastructure Tuesday. The officials spoke on condition of anonymity because they were not authorized to discuss the matter publicly. (AP)

RUSSIA: Poland is likely to request consultations under NATO's Article 4. (RTRS)

METALS: Workers of Chile's Escondida mine, the world's largest copper mine, decided to go on strike on Nov. 21 and 23 due to labor demands, their union said on Tuesday. (RTRS)

ENERGY: Federal pipeline safety regulators released on Tuesday a heavily redacted consultant's report that blamed inadequate operating and testing procedures, human error and fatigue for the June 8 explosion that shut Freeport LNG's export plant in Texas. (RTRS)

OIL: Iraq wants a review of the production quota allocated to it by oil producer group OPEC, state news agency (INA) reported on Tuesday, citing Prime Minister Mohammed Shia al-Sudani. (RTRS)

OIL: Oil supply to parts of Eastern and Central Europe via a section of the Druzhba pipeline has been temporarily suspended, according to oil pipeline operators in Hungary and Slovakia. (RTRS)

CHINA

PBOC: Market analysts are divided on outlook for further cuts to the reserve requirement ratio and interest rates, with some analysts seeing the possibility of a RRR cut in December or January, Shanghai Securities News reported. (MNI)

PBOC: The benchmark 5-year Loan Prime Rate, which lenders based their mortgage rates on, is expected to be lowered this year as policymakers aim for a soft landing in the real estate sector to help stabilise growth and control financial risks, Securities Times reported citing Wang Qing, chief analyst at Golden Credit Rating. (MNI)

PROPERTY: Recent policies to improve property developers’ financing environment cannot be considered as a rescue for the industry, as these measures aim to provide liquidity relief rather than prevent a balance sheet recession, Yicai.com said in an editorial. (MNI)

INVESTMENT: China's state planner, the National Development and Reform Commission (NDRC), in October approved eight fixed-asset investment projects worth 9 billion yuan ($1.27 billion), Meng Wei, an NDRC spokesperson told a news conference on Wednesday. (RTRS)

CHINA MARKETS

PBOC NET INJECTS CNY63 BILLION VIA OMOS WEDNESDAY

The People's Bank of China (PBOC) on Wednesday injected CNY71 billion via 7-day reverse repos with the rates unchanged at 2.00%. The operation has led to a net injection of CNY63 billion after offsetting the maturity of CNY8 billion reverse repos today, according to Wind Information.

- The operation aims to keep liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.9579% at 9:44 am local time from the close of 1.9429% on Tuesday.

- The CFETS-NEX money-market sentiment index closed at 52 on Tuesday vs 57 on Monday.

PBOC SETS YUAN CENTRAL PARITY AT 7.0363 WEDS VS 7.0421 TUES

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0363 on Wednesday, compared with 7.0421 set on Tuesday.

OVERNIGHT DATA

CHINA OCT NEW HOME PRICES -0.37% M/M; SEP -0.28%

JAPAN OCT CORE MACHINE ORDERS -4.6% M/M; MEDIAN +0.7%; SEP -5.8%

JAPAN OCT CORE MACHINE ORDERS +2.9% Y/Y; MEDIAN +8.0%; SEP +9.7%

JAPAN SEP TERTIARY INDUSTRY INDEX -0.4% M/M; MEDIAN +0.6%; AUG +0.7%

AUSTRALIA Q3 WAGE PRICE INDEX +3.1% Y/Y; MEDIAN +3.0%; Q2 +2.6%

AUSTRALIA Q3 WAGE PRICE INDEX +1.0% Q/Q; MEDIAN +0.9%; Q2 +0.8%

AUSTRALIA OCT WESTPAC LEADING INDEX -0.05% M/M; SEP -0.07%

As the growth rate continues to fall – albeit at a much slower pace than we saw last month – we continue to get further support from the Leading Index that growth will slow substantially in 2023. (Westpac)

NEW ZEALAND OCT NON-RESIDENT BOND HOLDINGS 58.4%; SEP 57.7%

MARKETS

SNAPSHOT: Russia Seemingly Not To Blame For Missile Hitting Poland

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 up 41.11 points at 28029.32

- ASX 200 down 19.435 points at 7122.2

- Shanghai Comp. down 10.284 points at 3123.794

- JGB 10-Yr future down 3 ticks at 149.40, yield up 0.1bp at 0.246%

- Aussie 10-Yr future up 3.5 ticks at 96.270, yield down 3.3bp at 3.726%

- U.S. 10-Yr future down 0-05 at 112-13, yield up 4.84bp at 3.818%

- WTI crude down $0.52 at $86.40, Gold down $5.23 at $1773.63

- USD/JPY up 62 pips at Y139.90

- BIDEN: ‘UNLIKELY’ MISSILE THAT HIT POLAND FIRED FROM RUSSIA (AP)

- RUSSIA'S DEFENCE MINISTRY DENIES RUSSIAN MISSILES STRUCK POLISH TERRITORY (RTRS)

- POLAND LIKELY TO INVOKE NATO'S ARTICLE 4, WILL RAISE MISSILE BLAST WITH UN – OFFICIALS (RTRS)

- DONALD TRUMP, TWICE IMPEACHED AND UNDER FBI INVESTIGATION, LAUNCHES 2024 WHITE HOUSE BID (CNBC)

- FED’S BARR WARNS US ECONOMY WILL SEE ‘SIGNIFICANT’ SOFTENING (BBG)

- ECB WILL INCREASE INTEREST RATES FURTHER, HOLZMANN SAYS (BBG)

- ECB’S STOURNARAS: PACE OF RATES ADJUSTMENT SHOULD BE PRUDENT (BBG)

US TSYS: Signs Of ‘Friendly Fire’ On Poland Allow Tsys To Cheapen

Tsys cheapened a touch in Asia, as U.S. President Biden suggested that the missile that hit Polish soil on Tuesday (killing 2 civilians) was “unlikely” to have been fired from Russia, with subsequent source reports pointing to a ‘friendly fire’ type incident surrounding the Ukrainian defence against the ongoing Russian missile attacks. This removed worry re: a direct Russian attack on a NATO member state, pressuring Tsys and supporting e-minis. There was little else to note in the way of tier 1 headline flow.

- That leaves the major cash Tsy benchmarks 3-5bp cheaper across the curve into London hours, with the intermediate zone leading the weakness, while the wings lagged the move.

- TYZ2 deals at the base if its 0-15 overnight range, -0-06 at 112-12, on above average volume of ~125K lots.

- A TY block sale (-1.3K) headlined on the flow side in Asia, with some desks indicating regional real money demand in several pockets of the curve.

- Wednesday’s NY docket is headlined by retail sales data, 20-Year Tsy supply and Fedspeak from Williams, Waller & Barr. Also note that the 2022 U.S. Treasury Market Conference will be held on Wednesday.

JGBS: Curve Twist Flattens, Signs Of Domestic Demand Propping Up Long End

JGB futures traded off of external factors, with the previously alluded to situation surrounding Tuesday’s missile situation in Poland (which killed 2 civilians) front and centre. Ultimately blame re: the matter was not laid at the feet of Russia and signs of a ‘friendly fire’ type of incident started doing the rounds.

- This saw the contract more than unwind its overnight gains, printing -9 into the bell.

- Meanwhile, cash JGBs saw some twist flattening, running 1.5bp cheaper to 2.5bp richer, pivoting around 10s. The lack of appeal when it comes to foreign bonds on the part of Japanese investors (owing to ongoing market vol. and elevated FX-hedging costs) may have contributed to this twist flattening, with the life insurer and pension fund community perhaps enticed by outright super-long JGB yield levels given the recent downside surprises in (still elevated) U.S. inflation ppints and the BoJ’s on hold stance.

- Local headline flow was limited at best.

- Looking ahead, Thursday’s local docket will be headed by trade balance data and 20-Year JGB supply. The weekly international security flow ledger from the MoF will also cross.

AUSSIE BONDS: Local Data Vs. Geopolitics

ACGBs came under some light pressure into the bell after AP source reports suggested that the missile that hit Polish land on Tuesday (killing two Polish civilians) “was fired by Ukrainian forces at an incoming Russian one,” per preliminary assessments flagged by U.S. officials. This came after U.S. President Biden suggested that it was” unlikely” that the missile was fired from Russia, while the G7 failed to lay the blame for the events at the feet of Russia. This left YM +4.0 & XM +3.5 at the close. Wider cash ACGBs print 3.5bp richer to 2.0bp cheaper, twist steepening with a pivot around 15s.

- Some light narrowing in EFPs provided modest support for ACGBs.

- Marginally firmer than expected Q3 WPI data was largely in line with the picture painted in the survey measures that have helped to guide monetary policy in recent months, so the readings don’t really represent much in the way of game changing information for the RBA at this juncture. This comes after the Bank slowed its pace of tightening to 25bp hikes over its last couple of meetings. Some post-data vol. ensued, before a bid came back in, aided by some firming in U.S. Tsys at the time.

- Bills were 1-11bp richer through the reds, bull flattening, generally following bonds, while RBA dated OIS was little changed on the day.

- Looking ahead, the monthly labour market report headlines the domestic docket on Thursday.

AUSSIE BONDS: ACGB Nov-33 Auction Results

The Australian Office of Financial Management (AOFM) sells A$900mn of the 3.00% 21 November 2033 Bond, issue #TB166:

- Average Yield: 3.7327% (prev. 4.1220%)

- High Yield: 3.7350% (prev. 4.1250%)

- Bid/Cover: 2.1222x (prev. 2.8062x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 65.2% (prev. 73.4%)

- Bidders 42 (prev. 45), successful 22 (prev. 22), allocated in full 13 (prev. 14)

NZGBS: Off Best Levels, But Still Richer

NZGBs finished off best levels after an extension of the early richening linked to Tuesday’s firming of global core FI markets reversed a touch as it became apparent that Western powers were not willing to lay the blame of the missile that hit Polish territory (and killed two Polish civilians) on Tuesday squarely at the feet of Russia.

- Still, cash NZGBs were 3.5-4.5bp richer across the curve come the bell, with light bull flattening in play.

- Swap spreads were little changed come the close after some mixed performance at different stages of the session.

- RBNZ dated OIS pricing was incrementally softer, with ~63bp of tightening priced for next week’s meeting, while terminal OCR pricing sits around 5.05%.

- Local data revealed an uptick in non-resident NZGB bond holdings.

- Looking ahead, tomorrow will see the release of Q3 PPI data.

OIL: Prices Range Bound Again On Difficult Political Environment

Oil prices have been trading in a tight range. Even the short-lived bounce in reaction to reports of a Russian-made missile exploding in Poland didn’t break out. WTI has been between $87.50 and $86.35/bbl and is now at the lower end of the range on the back of USD gains. Brent traded between $93.40 and $94.10 and is now around $93.40. Prices are about 0.5%below the NY close.

- US API data showed that the previous week’s build in crude was more than unwound in the latest week with stocks falling 5.835mn bbl. Distillate stocks rose slightly by 0.9mn bbl and gasoline by 1.7mn.

- The IEA noted in its November report that crude inventories in developed countries were at their lowest since 2004, making them vulnerable to further supply disruptions. It also reported that OPEC+ output remains more than 1mbd below the quota.

- Tight supply conditions balancing uncertainty regarding the demand outlook continue to keep oil prices range bound. Deterioration in the situation in the Ukraine could increase supply fears and reopening in China could improve the demand outlook and thus push prices higher again.

GOLD: Edging Away From Tuesday’s Peak

The yellow metal has ticked away from Tuesday’s highs in Asia-Pac trade, last dealing a little over $5/oz softer on the day, printing just above $1,770/oz.

- A reminder that Tuesday’s session high was a product of softer than expected U.S. PPI data, with a re-test coming on the back of news of a missile falling in Polish territory (which killed two Polish civilians).

- An Asia-Pac rally in the greenback, which has seen the broader DXY pare the bulk of Tuesday’s losses, alongside a light uptick in U.S. Tsy yields, after western powers chose not to lay the blame re: the Polish missile situation at the feet of the Russians (U.S. President Biden suggested that it was “unlikely” that the missile was launched from Russia), has weighed on gold overnight.

- Fedspeak & policy trajectory, as well as U.S. inflation dynamics, continue to present the most meaningful fundamental inputs for gold in the immediate term.

- Technically, last week’s gains resulted in the break of a number of important resistance points. The yellow metal has cleared the Oct 4 high ($1729.50/oz). This strengthens the current bullish theme and paves the way for an extension towards $1800/oz, with key resistance located above that particular round number resistance in the form of the Aug 10 high ($1807.90/oz). On the downside, initial firm support is seen at the Nov 9 low ($1,702.30/oz).

FOREX: European FX Get Reprieve From Missile Updates, Greenback Buoyed By Higher U.S. Tsy Yields

G10 currencies with exposure to Eastern European geopolitics gained after U.S. President Joe Biden said it was "unlikely" that the missile that killed two people in Poland on Tuesday was fired from Russia, based on preliminary assessment of its trajectory. While Poland has announced an international probe into the incident, the broader perception was that the blast was likely a tragic accident rather than a deliberate strike, which would reduce the risk of a direct Russia-NATO confrontation.

- Biden's comments allowed EUR to become the best performer among major currencies, with the likes of DKK and SEK also finding poise. The Norwegian Krone lagged behind its Scandie cousins amid softer crude oil prices. Spot EUR/PLN topped out at at PLN4.7848 but then trimmed the bulk of its initial gains on Biden's remarks.

- The BBDXY index came under pressure as the POTUS spoke, virtually erasing its initial 0.26% upswing. Selling interest quickly dissipated, with the index advancing to new session highs, as the greenback rebounded towards the top of the G10 scoreboard, supported by higher U.S. Tsy yields.

- The combination of geopolitical relief and sell-off in U.S. Tsys generated yen underperformance. Spot USD/JPY rallied past the Y140 mark, lodging session highs at Y140.29 but falling short of testing yesterday's peak.

- Data showing continued decline in China's new home prices facilitated the upswing in USD/CNH. The value of new residential properties fell 0.37% M/M last month, which was the fastest pace of decline since Feb 2015.

- Inflation data from the UK and Canada, U.S. advance retail sales and industrial output, as well as a busy central bank speaker slate dominated by ECB members take focus from here.

FX OPTIONS: Expiries for Nov16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0200-10(E1.8bln), $1.0250-55(E1.0bln), $1.0500(E508mln)

- USD/JPY: Y137.50($500mln), Y140.00-10($777mln), Y140.75-00($840mln), Y147.90-00($1.1bln)

- USD/CNY: Cny7.2000($2.6bln), Cny7.3000($3bln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/11/2022 | 0700/0700 | *** |  | UK | Consumer inflation report |

| 16/11/2022 | 0700/0700 | *** | | UK | Producer Prices |

| 16/11/2022 | 0900/1000 | *** |  | IT | HICP (f) |

| 16/11/2022 | 0900/1000 | ** | | IT | Italy Final HICP |

| 16/11/2022 | 0930/0930 | * | | UK | ONS House Price Index |

| 16/11/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 16/11/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 16/11/2022 | - |  | ID | G20 Summit in Indonesia | |

| 16/11/2022 | - |  | TH | APEC Leaders’ Summit | |

| 16/11/2022 | 1315/0815 | ** |  | CA | CMHC Housing Starts |

| 16/11/2022 | 1330/0830 | *** | | CA | CPI |

| 16/11/2022 | 1330/0830 | *** | | US | Retail Sales |

| 16/11/2022 | 1330/0830 | ** | | US | Import/Export Price Index |

| 16/11/2022 | 1415/0915 | *** | | US | Industrial Production |

| 16/11/2022 | 1415/1415 | | UK | BOE Treasury Select Committee hearing on Nov Monetary Policy Report | |

| 16/11/2022 | 1450/0950 | | US | New York Fed's John Williams | |

| 16/11/2022 | 1500/1000 | * | | US | Business Inventories |

| 16/11/2022 | 1500/1000 | ** | | US | NAHB Home Builder Index |

| 16/11/2022 | 1500/1600 |  | EU | ECB Lagarde Speech at European School Frankfurt Anniversary | |

| 16/11/2022 | 1500/1600 | | EU | ECB Panetta at ABI's Executive Committee Meeting | |

| 16/11/2022 | 1500/1000 | | US | Fed Vice chair for Supervision Michael Barr | |

| 16/11/2022 | 1530/1030 | ** | | US | DOE weekly crude oil stocks |

| 16/11/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 16/11/2022 | 1935/1435 | | US | Fed Governor Christopher Waller | |

| 16/11/2022 | 2100/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.