Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI Eurozone Inflation Preview – February 2024

MNI Eurozone Inflation Preview – February 2024

EXECUTIVE SUMMARY

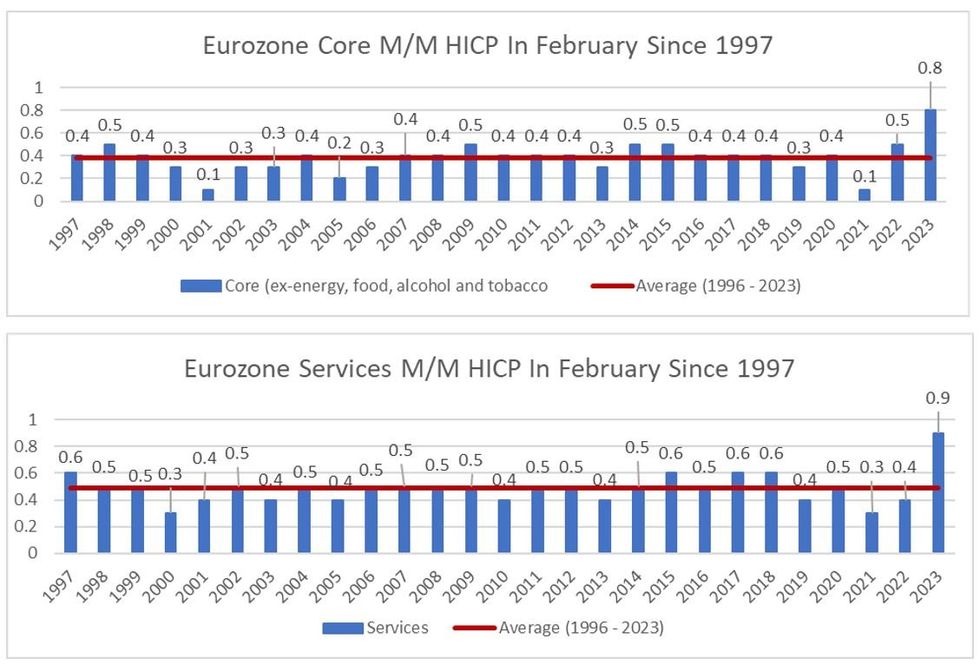

Services Under Scrutiny Ahead Of March ECB Meeting

Eurozone core and headline inflation are expected to resume their downtrends in February on an annual basis, with headline printing a 3-month low 2.5% Y/Y (vs 2.8% prior) and core returning to below 3% for the first time since February 2022 at 2.9% (3.3% prior).

- February marks the first of a two-month sequence that typically sees reaccelerations in non-seasonally adjusted HICP (both core and headline), with March being typically pronounced, though the base effects from an especially strong Feb 2023 (especially in categories such as food) will help keep a lid on the overall print.

- The main area of scrutiny will again be services, which having printed 4.0% Y/Y for 3 consecutive months is overwhelmingly expected to pull back. A figure in the 3.6-3.7% Y/Y area is the base case.

- February’s inflation data will be the last before the ECB’s March meeting and projections. It would take an extraordinary downside surprise in the data to spur even a discussion on a March cut – but the report could play a crucial role in the meeting communications and potential for an April cut.

- Our preview includes analysis of price categories to watch, assessments of underlying inflation trends, outlooks for the French, German, Spanish, and Italian national inflation prints, and sell-side analyst previews.

FOR FULL PDF ANALYSIS:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok