Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

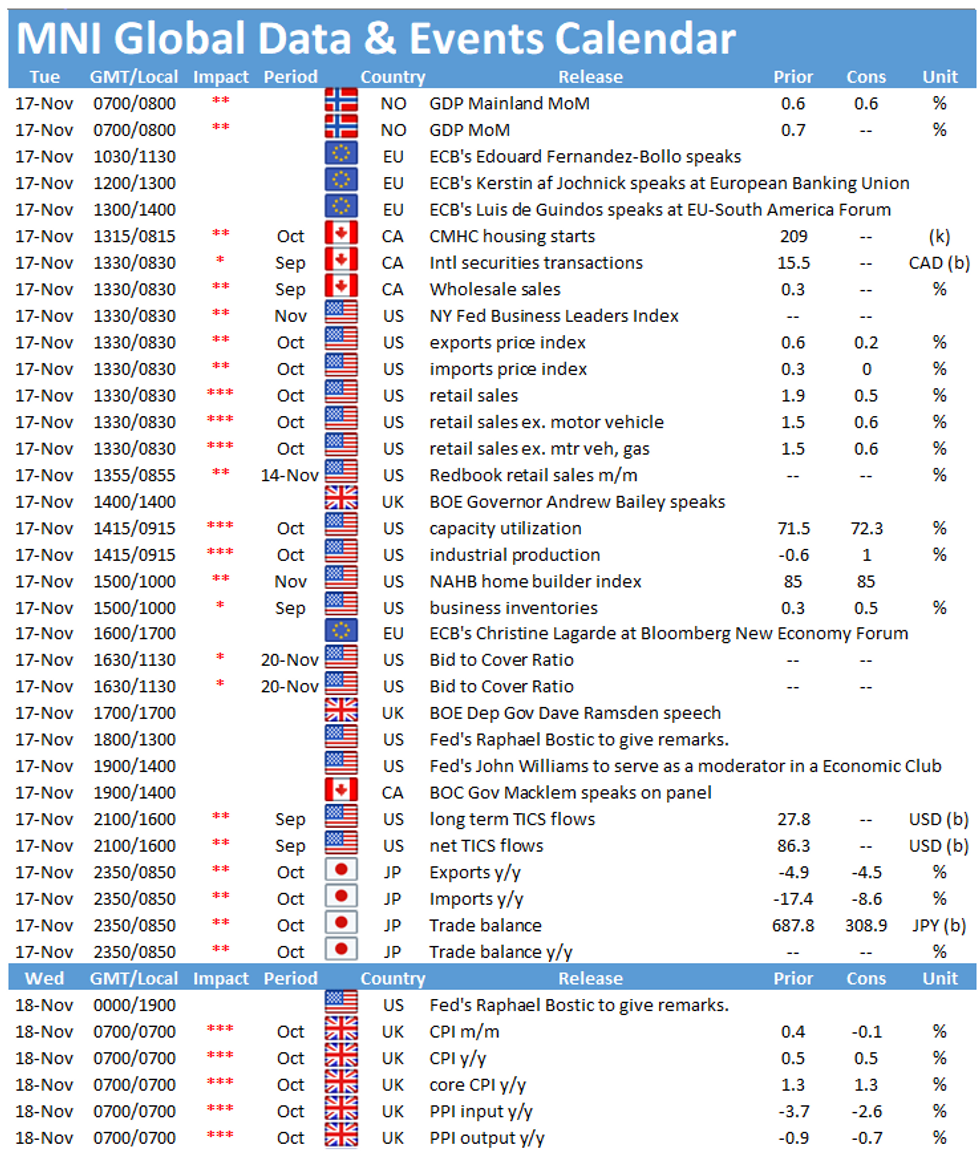

Tuesday kicks off with the release of Norwegian GDP figures at 0700GMT followed by US retail sales at 1330GMT and US industrial production at 1415GMT.

Norwegian GDP set to rebound in Q3

Tuesday's GDP release is expected to show a rebound of economic activity in Q3 with markets pencilling in an increase of 5.2% for quarterly Mainland GDP. The economy contracted by 6.3% in the second quarter of the year due the national lockdown. Household consumption and imports showed the largest declines in Q2. Monthly Mainland GDP is expected to remain August's level of 0.6% in September. Infection rates are also rising in Norway but at a slower pace than in its European pears which battle the second wave of Covid-19 at the moment. However, the deteriorating situation regarding the pandemic is likely to weigh on household spending even in the absence of a second national lockdown.

US retail sales growth forecast to slow

Sales should rise 0.5% in October, according to Bloomberg, nearly four times slower than September's 1.9% increase that was the smallest since May. That would be the smallest monthly increase since October 2019 when sales were up 0.4%. Excluding motor vehicle and gas station sales, retail sales should be up 0.6%. Surging Covid-19 infections likely curbed in-store business activity in some states, but online shopping should still keep spending relatively high.

US industrial production expected to rise

Industrial output eased in September by 0.6% after four consecutive months of growth, although the pace of the recovery slowed in recent months. Production increased by 0.4% in August following a 4.2% increase in the previous month. However, last month's report noted that industrial production was still 7.1% below the pre-pandemic level. Manufacturing output declined by 0.3% in September and markets expect the index to rebound to 1.0% in October. Survey evidence is in line with market forecasts. The ISM manufacturing PMI ticked up 3.9 points in October, while the IHS manufacturing PMI improved to the highest level since January 2019.

The events calendar throws up a busy schedule on Tuesday including speeches by ECB's Edouard Fernandez-Bollo, Kerstin af Jochnick, Luis de Guindos and Christine Lagarde as well as BOE's Andrew Bailey and Dave Ramsden, Fed's Raphael Bostic and John Williams and BOC's Tiff Macklem.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.