Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

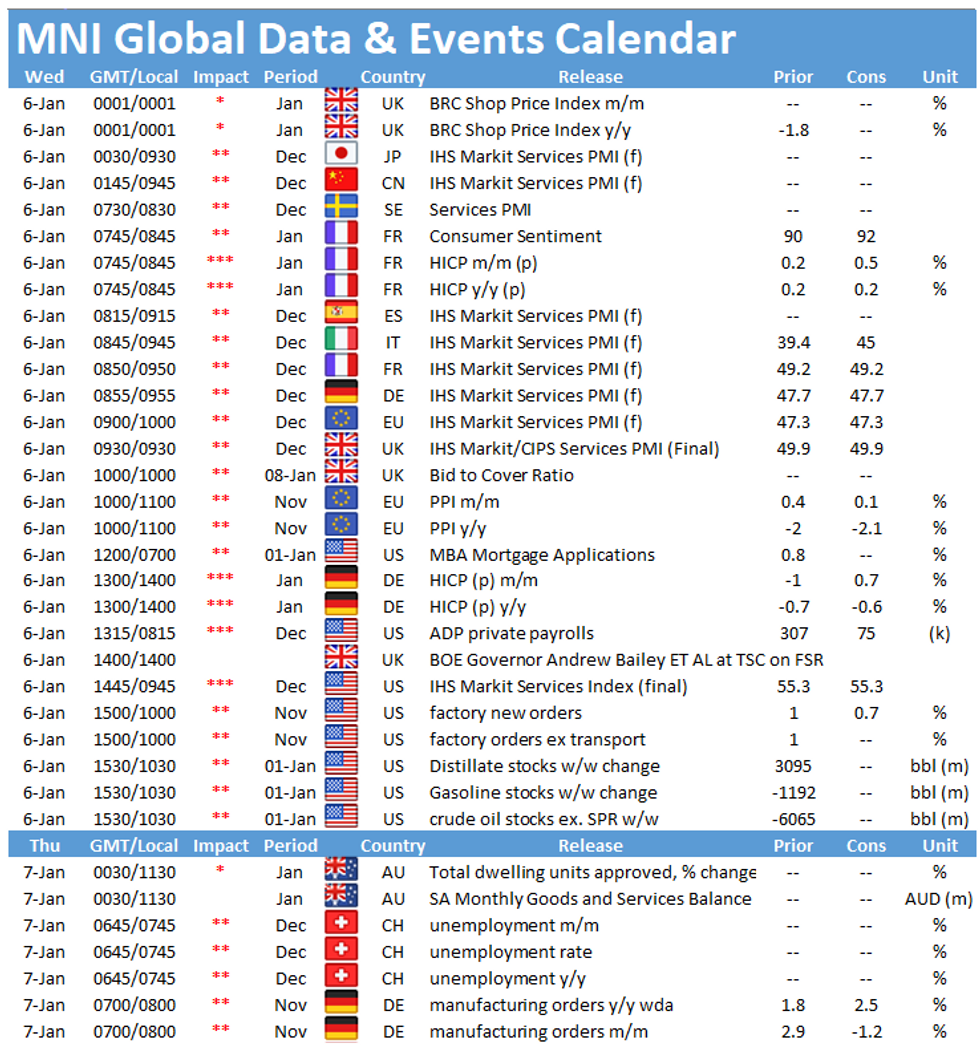

The main data events Wednesday include the publication of the final services PMIs from Spain (0815GMT), Italy (0845GMT), France (0850GMT), Germany (0855GMT), the EZ (0900GMT) and the UK (0930GMT). The highlight of the day in the US is the release of factory orders at 1500GMT.

Europe's services PMIs remain weak

The second wave of Covid-19 is hitting many European nations hard and led to further lockdowns in several countries in November. Infection rates remained elevated in December and prompted governments to prolong the tight restrictions which mainly weigh on the service sector. As a result, the services PMIs are all forecast to remain below the 50-mark which signals contraction of business activity in the sector.

Nevertheless, both Spanish and Italian services PMIs are forecast to improve modestly in December to 45 and 45.3, respectively. The French, German, EZ and UK manufacturing PMIs are all expected to register in line with the flash results showing small improvements in December to 49.2, 47.7, 47.3 and 49.9, respectively. However, all indicators remain in contraction territory as most countries continue to struggle with rising infection rates. This will keep the services PMIs subdued in the coming month. However, all flash reports noted an increase in business optimism about the year ahead, mainly driven by the positive news regarding the vaccine roll-out.

US factory orders forecast to decelerate

New orders for manufactured goods rose for the sixth consecutive month in October and markets look for another increase in November. Monthly factory orders ticked up by 1.0% in October and are expected to rise by 0.7% in the following month. Survey evidence is in line with market forecasts. The ISM manufacturing PMI ticked down slightly in November with new orders edging lower, although remaining in expansion territory. Similarly, the IHS manufacturing PMI signalled an improvement of operating conditions with new orders remaining strong in December.

The events calendar remains quiet on Wednesday with the only event scheduled being an appearance by BOE's Andrew Bailey in front of the Treasury Select Committee.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.