Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

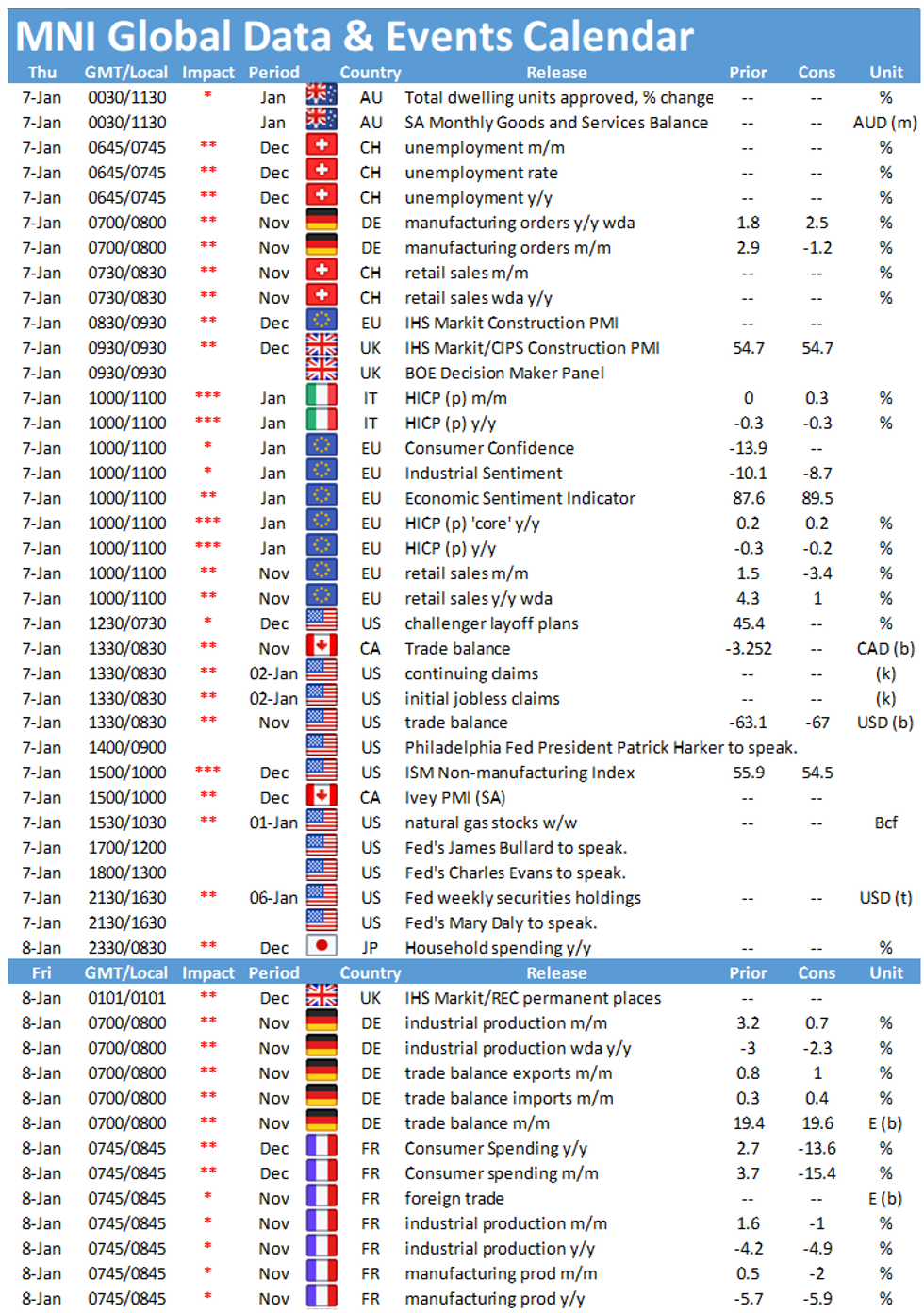

Thursday throws up a busy day of data events with the main highlights being the release of EZ retail sales figures and the European Commission's economic sentiment indicator, both published at 1000GMT. In the US, the release of the ISM services PMI will be eagerly awaited at 1500GMT.

EZ retail sales forecast to decline

Retail sales in the Eurozone are expected to decline by 3.4% in November after October's increase of 1.5%. Annual sales are forecast to decelerate to 1.0%, down from October's reading of 4.3%. Many European countries introduced a second national lockdown where shops and the hospitality sector had to close amid the second wave of Covid-19. Already available state-level data provides a mixed picture. German retail sales increased by 1.9% in contrast to markets looking for a decline, while Spanish retail trade declined by 0.8%.

EZ ESI seen higher in December

The European Commission's economic sentiment indicator is forecast to rise to 89.5 in December after November's drop to 87.6. Both industrial and service sector sentiment are expected to improve slightly in December to -8.7 and -15.0, respectively. However, both continue to register in negative territory. The index recovered from April's slump through October, but the second wave of infections led to a marked decline in November. Service, retail trade and consumer confidence took the largest hit in November as many European countries went into a second lockdown. Restrictions were eased slightly in December, but infection rates stayed high and restrictions remained tight which is likely to weigh on sentiment in the service and retail trade sector in January.

ISM Services PMI projected to fall

The ISM services PMI is expected to decrease to 54.5 in December which would mark a third successive decline. The indicator eased to 55.9 in November, mainly on the back of slowing business activity and new orders. A rise in employment and supplier deliveries held further declines back. Similar survey evidence is in line with market forecasts. The IHS services PMI eased in December, signalling a loss of growth momentum. Moreover, the Dallas Fed services outlook survey suggests another weakening of the general business activity index in December.

The main events to look out for on Thursday include speeches by regional Fed Presidents Patrick Harker, Tom Barkin, James Bullard, Charles Evans and Mary Daly.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.