Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

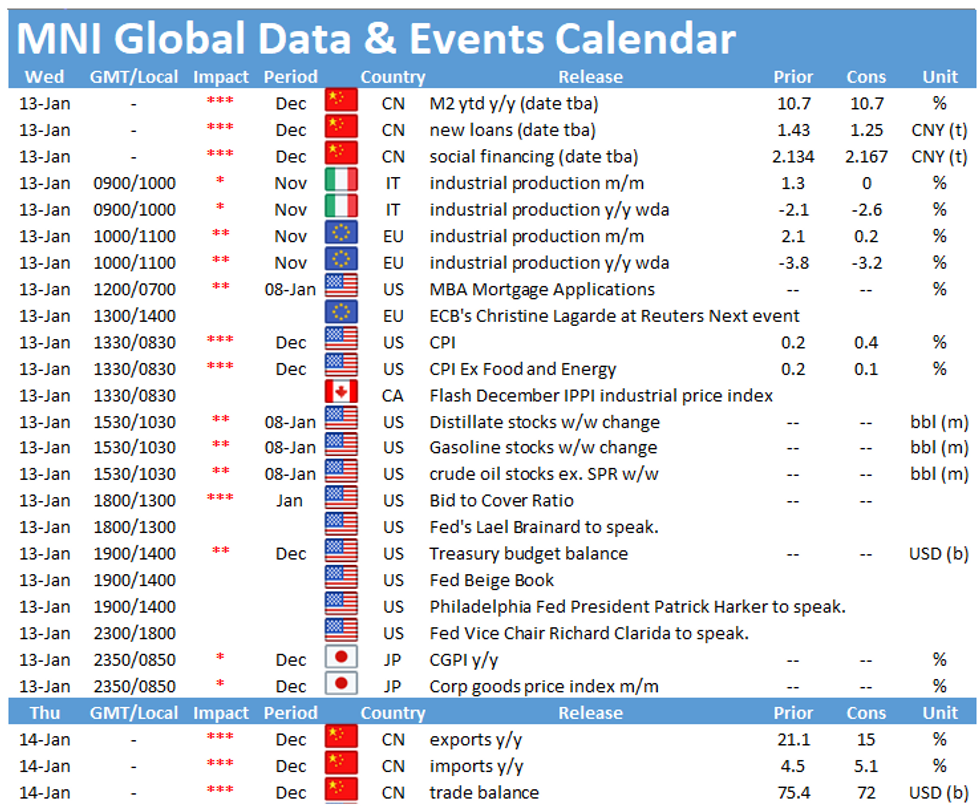

Wednesday's data highlights include Italian and EZ industrial production figures at 0900GMT and 1000GMT, respectively, with the release of US inflation figures at 1330GMT likely to be closely watched.

Italian industrial production seen flat

Market analysts expect monthly industrial output in Italy to stagnate in November amid the second lockdown. Monthly production increased by 1.3% in October following a 5.1% dip in September. Annual output is forecast to decline by 2.6% in November after falling by 2.1% previously. Survey evidence suggests a continued recovery of the Italian manufacturing sector. The manufacturing PMI ticked up in December, showing an increase in new orders and production. Moreover, Istat's manufacturing confidence index also rose in December.

EZ Industrial output expected to slow

Source: Bloomberg

Industrial production across the Eurozone is projected to decelerate to 0.2% in November as many European countries tightened restrictions amid rising infection rates. Monthly industrial production increased 2.1% in October after edging up 0.1% in the previous month. The recovery of the industrial sector slowed from July onwards before picking up in October. However, Covid-19 cases remained elevated well into the new year and subsequent restrictions are likely to weigh on the industrial sector going forward. Already available state-level data suggests a deceleration in November. German industrial production increased 0.9% in November, while French and Spanish output both declined by 0.9% in the same period.

US inflation forecast to accelerate

Source: Bloomberg

The US consumer price index rose 0.2% in November on a monthly basis and markets are looking for an increase to 0.4% for December. Food inflation eased in November by 0.1%, which was led by falling prices for groceries (-0.3%), while energy prices rose by 0.4% after growing by 0.1% in October. Excluding food and energy, prices increased 0.2% in November and markets expect core inflation to tick down to 0.1% in December. Against that, annual inflation is expected to increase by 1.3% in December following November's reading of 1.2%.

The events calendar throws up a busy session Wednesday including speeches by ECB President Christine Lagarde, St. Louis Fed's James Bullard, Philadelphia Fed's Patrick Harker and Fed Vice Chair Richard Clarida.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.