Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

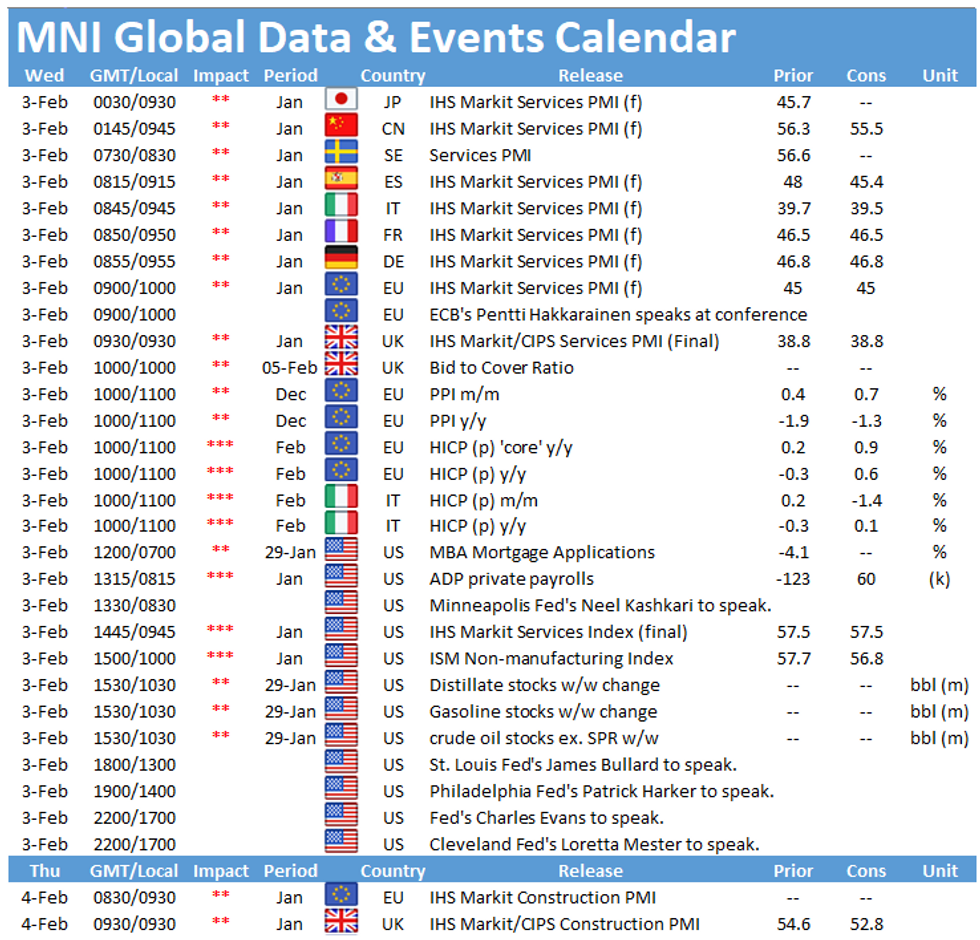

The main data to follow Wednesday include the final services PMIs for Spain (0815GMT), Italy (0845GMT), France (0850GMT), Germany (0855GMT), the EZ (0900GMT) and the UK (0930GMT) as well as flash inflation figures for the EZ at 1000GMT. In the US the release of the ISM services PMI at 1500GMT will be closely watched.

Europe's Services PMIs deep in contraction territory

Spain's and Italy's services PMIs are both expected to decline in January following improvements seen in December. Spain's index is forecast to ease to 45.4 in January after rising to 48.0 in December. The Italian services PMI only ticked up marginally in December to 39.7, but markets look for a renewed fall in January to 39.5, signalling a rapid drop in activity. However, both December reports noted a sharp rise in business sentiment due to the positive news of a vaccine.

Source: Bloomberg

The French, German, EZ and the UK services PMIs are all projected to register in line with the flash results showing monthly declines in January. The renewed strict measures to control the spread of Covid-19 weigh heavily on the service sector in all four countries. Service sector output declined in January according to the flash estimates, although the decreases were smaller than those seen in November and during the first lockdown in spring 2020.

EZ inflation seen rising

The headline HICP recorded negative readings since August 2020 and remained at the level of -0.3% for the fourth consecutive month in December. In January markets look for an uptick to 0.6% which would be the highest level since March. Already available state level data is in line with market forecasts and even suggests a slight upside risk. German flash inflation surprised in January, ticking up to 1.6% in contrast to markets looking for an increase to 0.5%. However, Destatis noted that the end of the temporary VAT cut, the new CO2 prices and an increase in the statutory minimum wage impacted price in January. French inflation rose by more than markets expected as well, increasing to 0.8% after a flat reading recorded in December.

ISM services PMI expected to edge lower

The ISM services PMI increased in December to 57.2, up from 55.9 seen in November. December's increase was mainly driven by a sharp rise of Supplier Deliveries, up 5.8pt. Business Activity and New Orders saw monthly gains as well, while Employment declined and shifted back to contraction territory. In January markets are looking for a downtick to 56.8 which would be a two-month low. Similar survey evidence provides a mixed picture. The Chicago Business Barometer as well as the IHS flash services PMI increased in January, while the Dallas Fed's services survey showed an almost unchanged reading for the general business activity index.

Wednesday's events calendar throws up a busy schedule. The main speakers to follow include ECB#s Pentti Hakkarainen, Minneapolis Fed's Neel Kashkari, St. Louis Fed's James Bullard, Philadelphia Fed's Patrick Harker, Cleveland Fed's Loretta Mester and Fed's Charles Evans.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.