Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

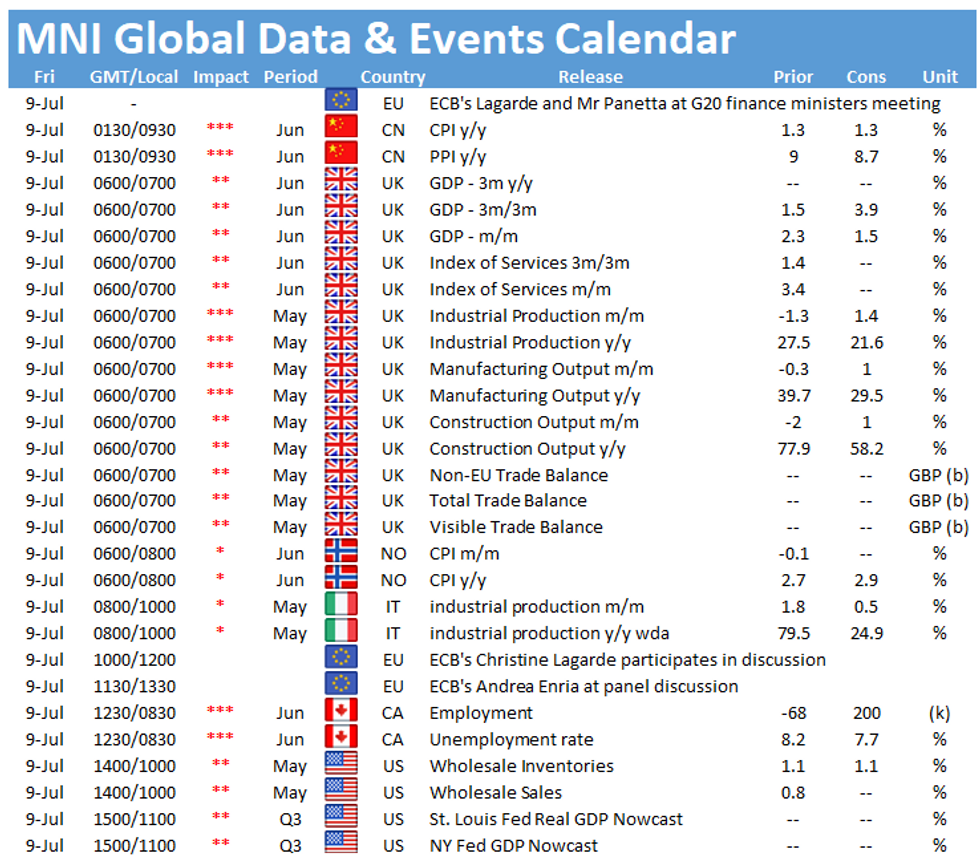

The week ends with several data releases of note, starting with the publication of the UK's short-term monthly indicators at 0700BST. At 0900BST the release of Italian industrial production will be closely watched before the focus turns to the publication of the Canadian labour force survey at 1330BST.

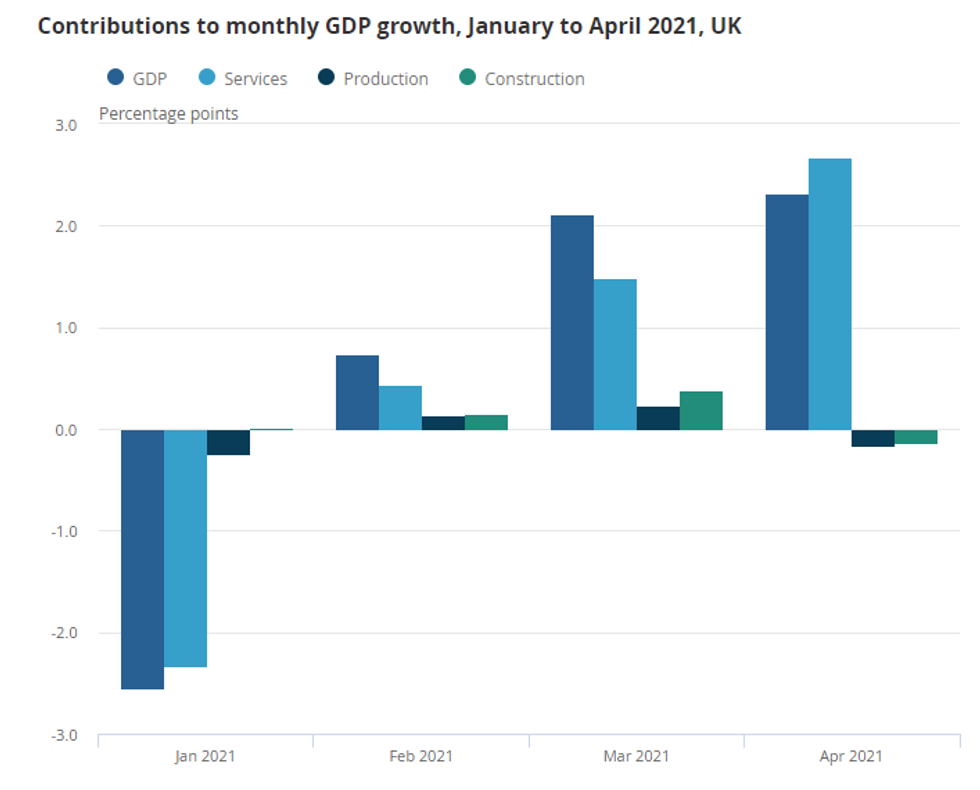

UK monthly GDP forecast to grew

Monthly GDP is forecast to decelerate slightly in May to 1.5%, after rising by 2.3% in April. Economic growth in April was still 3.7% lower than in February 2020. Nevertheless, the gradual reopening of the economy continues to push up business activity and should result in a solid increase of economic growth in the second quarter. The index of services is expected to increase by 1.6% in May, a slightly slower increase than in the previous month where services expanded by 3.4%. Industrial and manufacturing output are both forecast to rebound in May and rise by 1.5% and 1.0%, respectively.

Looking ahead, the spread of the Delta variant must be closely watched as it might pose a downside risk for the pace of recovery. Moreover, a lack of staff availability as suggested by the KPMG/REC jobs report, might also weigh on the pace of the recovery.

Source: Office for National Statistics

Italian industrial production seen rising

Industrial production increased by 1.8% in April, after easing slightly in the previous month. Markets expect another uptick in May, although at a slower pace of 0.3%. Annual output surged to 79.5% in April, which was mainly due to base effects as many factories were closed in April 2020. The index is expected to post another strong reading in May at 24.8%.

Survey evidence suggests that the recovery of the manufacturing sector is ongoing. The June manufacturing PMI recorded the second highest reading in the survey's history, while Istat's manufacturing confidence index rose further in June as well.

Canadian jobless rate projected to tick down

Canada's unemployment rate was broadly unchanged in May at 8.2% and markets expect the index to edged down by just 0.1pp to 8.1% in June. The employment rate declined for the second successive month in May by 68,000 with almost all of the decrease being recorded in part-time work, as strict covid-restrictions remained in place. The biggest decline of employment was seen in the goods-producing sector - the first drop since April 2020 - followed by retail trade and other services. In June, markets expect an increase by 40,000 for employment.

The main events to follow on Friday include speeches by ECB's Christine Lagarde and Andrea Enria.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.