Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

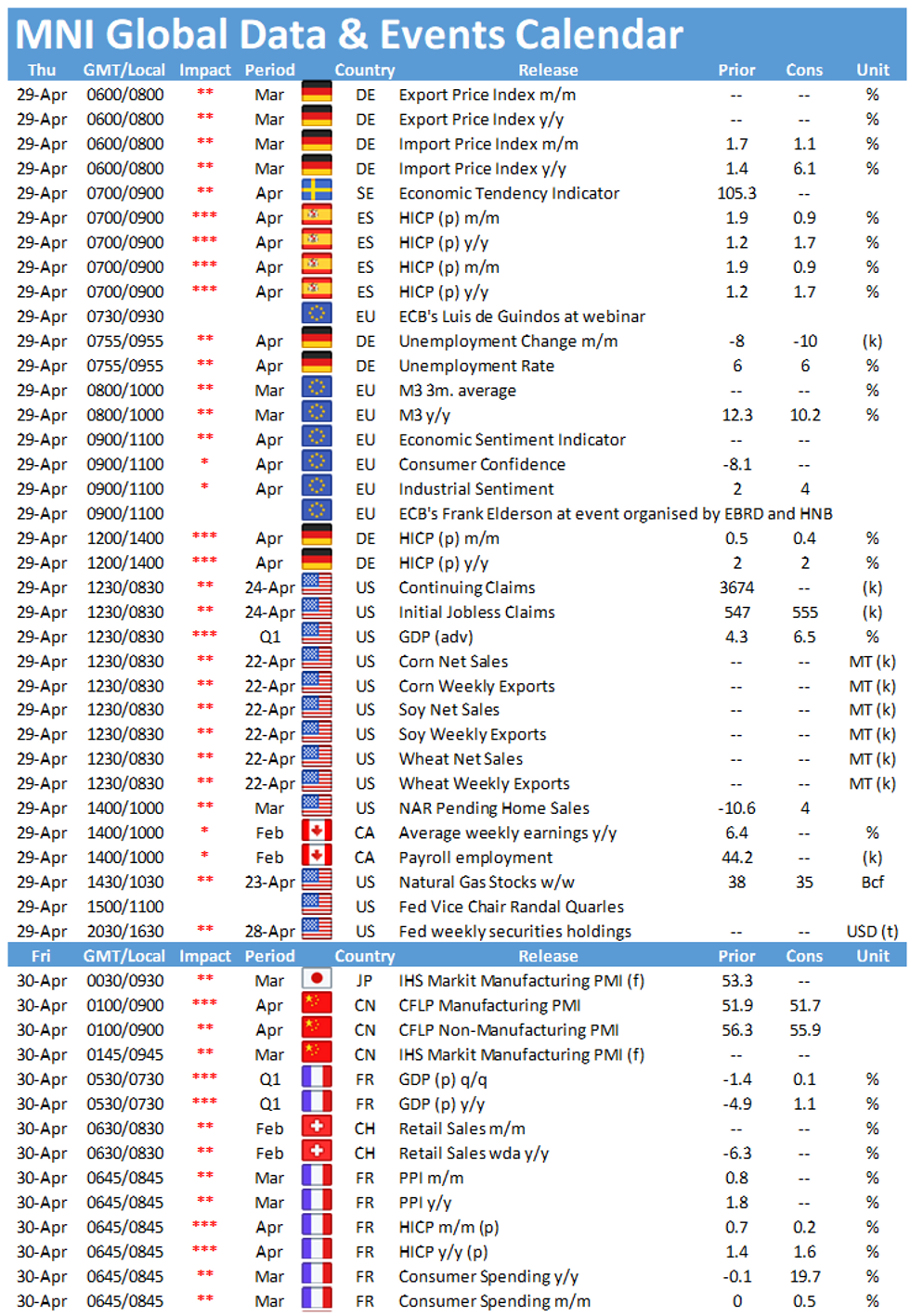

Thursday throws up a busy schedule of data events. The main highlights in Europe will be the European Commission's Economic Sentiment Indicator at 1000BST and German flash inflation at 1300BST. In the US, the release of Q1 GDP figures will be closely watched at 1330BST.

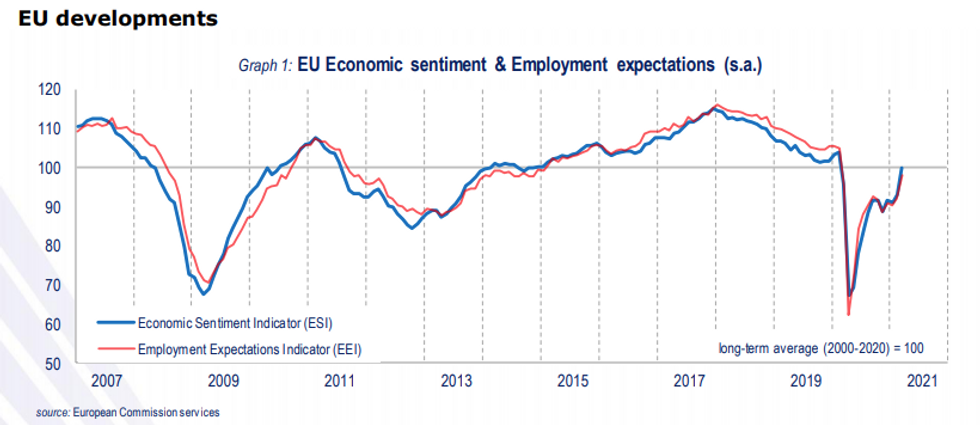

EZ ESI expected to see further gains

The EZ ESI is forecast to rise further to 103.0 in April, up from 101.0 seen in March. This would mark the highest level since February 2020. The index improved markedly in March, mainly on the back of a sharp increase of services and retail trade sentiment. With vaccinations gaining momentum, business sentiment is likely to pick up in anticipation of a near-term reopening of consumer-facing businesses. Services confidence is projected to improve further in April to -8.0. According to the flash estimate, consumer confidence rose to -8.1, which is the best result since the start of the pandemic. Meanwhile, industrial sentiment is forecast to gain 2.3pt to and rise to 4.3, which would mark the second successive positive reading and the highest level since November 2018.

Similar survey evidence is in line with market forecasts. The flash EZ composite PMI rose to a 9-month high in April with both the manufacturing and services sector seeing monthly gains.

Source: European Commission

German inflation seen unchanged at 2.0%

Inflation started to pick up at the beginning of the year after several months of negative rates. The headline annual HICP rose to 2.0% in March and markets expect the index to remain at 2.0% in April. Most of the upward pressure on price growth stems from temporary factors such as the end of the German VAT cut and oil price fluctuations in 2020. Inflation is likely to rise further in the coming months, mainly driven by energy base price effects.

Survey evidence suggests an increase in both input and output prices, mainly due to supply chain issues. The flash composite PMI saw charges for goods and services rise at the fastest pace since January 2019.

US GDP forecast to expand

U.S. Q1 GDP is set to grow at an annual rate of 6.5%, according to Bloomberg, up from the annualized 4.3% pace set in the final quarter of 2020. That should mostly reflect consumer spending driven by additional government aid and job growth, though severe winter storms in February could put some downward pressure on growth. Imports were particularly strong through Q1, while exports continued to struggle due to global demand and supply chain constraints.

The main speakers to look out for on Thursday include ECB's Luis de Guindos, Frank Elderson and Fed's Randal Quarles.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.