Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

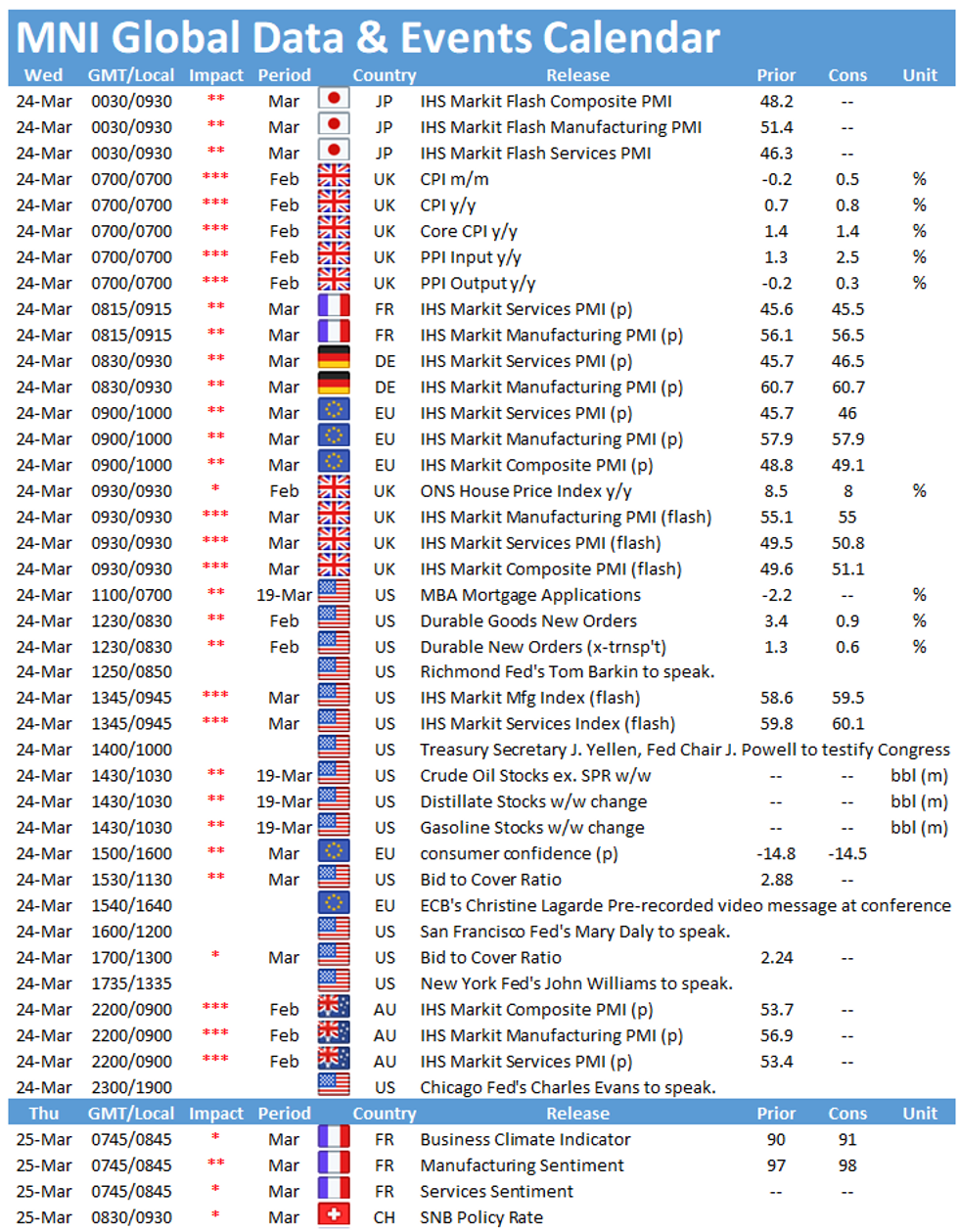

Wednesday kicks of with UK inflation figures at 0700GMT, followed by the flash PMIs for France (0815GMT), Germany (0830GMT), the EZ (0900GMT) and the UK (0930GMT). In the US the publication of durable goods orders will be closely watched at 1230GMT.

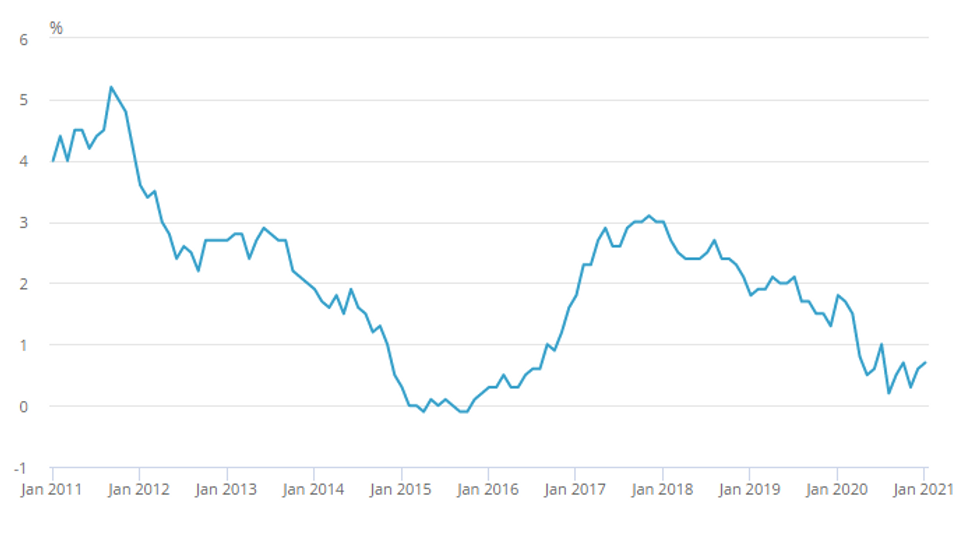

UK inflation seen marginally higher

Inflation is forecast to pick up slightly to 0.8% in February, up from 0.7% seen in January, while core CPI is seen unchanged at 1.4%. This would mark the third successive increase in headline inflation and the highest level since July 2020. January's uptick was driven by rising prices for recreation and culture, furniture and household goods, restaurant, food, hotels and transport, while clothing and footwear prices had a downward effect on price growth.

The BRC shop price index reported falling prices in February as the third lockdown constricts consumer spending and firms continue to discount their products to encourage spending. On the other hand, the services PMI reported a strong increase in input prices as well as output charges, which rose to the highest since February 2020. Overall, prices will largely be driven by higher oil prices compared to a year ago. Hence, the BOE expects inflation to rise steadily through the year, certainly hitting target, although price rises are seen as transitory and likely to fall back in 2022.

UK CPI 12-Month Inflation Rate

Source: Office for National Statistics

PMIs: Divergence between manufacturing and services persist

The flash PMIs are expected to change only marginally in March and the divergence between the manufacturing and the service sector persists as many countries continue to struggle with high infection rates and have to maintain tight restrictions which mainly weigh on consumer-facing businesses in the service sector.

All four manufacturing PMIs remain comfortably above the 50-mark. The French index is forecast to remain at February's level of 56.1 in March, while the German PMI is seen slightly higher at 60.9. The overall EZ manufacturing PMI, which also includes data from Italy and Spain, is expected to remain at February's level of 57.9 in March. Meanwhile, the UK's manufacturing PMI is forecast to ease slightly to 55.0 in March.

France's, Germany's and the EZ's services PMIs are expected to remain in contraction territory with the French index anticipated to drop to 45.5, while the German indicator is forecast to tick up marginally to 46.3. The EZ flash services PMI is projected to gain 0.3pt to 46.0. On the other hand, the UK's services PMI is expected to shift back to expansion territory in March, up to 51.0, despite the continuing lockdown. February's survey noted signs of growth in technology and some business services, while consumer-facing businesses continued to report severe constraints.

US durable goods orders projected to slow

Orders for manufactured durable goods are forecast to decelerate to 0.9% in February after rising by 3.4% in January. This would mark the tenth consecutive monthly gain of new orders. Excluding transportation, new orders rose by 1.3% in January and markets expect the indicator to slow to 0.6% in February. Survey evidence is in line with market forecasts. The ISM manufacturing PMI saw new orders increase further in February, as did the IHS manufacturing PMI where order rose grew at the fastest rate in three years.

The main speakers to look out for on Wednesday include Richmond Fed's Tom Barkin, ECB's Christine Lagarde, San Francisco Fed's Mary Daly, New York Fed's John Williams and Chicago Fed's Charles Evans

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.