Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (Washington)

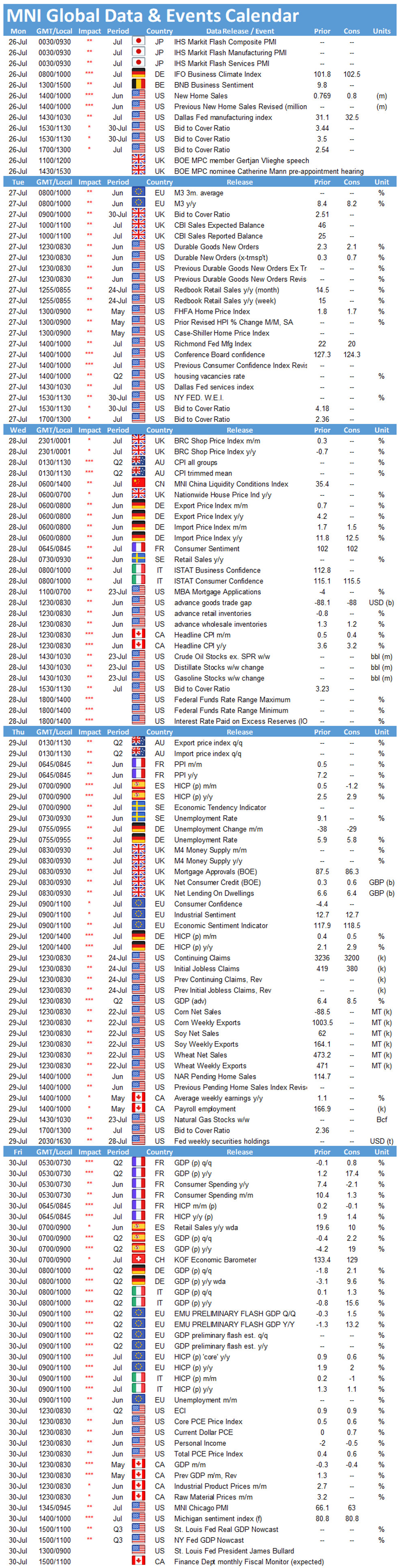

Key Things to Watch:

- Wednesday, July 28 – FOMC Policy Decision

- No policy change is expected and no fresh economic projections are due to be released at the July meeting. Rates at set to stay at the 0%-0.25% target range, with USD120 billion of monthly asset purchases to continue until "substantial further progress" is seen toward full employment and stable prices.

- The committee will continue discussions over the timing and roadmap for tapering QE but no decision is expected at this meeting. Chair Jay Powell said earlier this month that the FOMC will be watching closely to see how inflation and labor supply evolve over the next six months. Should inflation persistently surprise to the upside, it would be prepared to adjust policy as needed.

- Friday, July 30 – Flash Eurozone Q2 GDP and Inflation Data

- Friday sees flash Eurozone inflation and Q2 GDP data published, both likely to give the ECB a key guide to the state of the economy.

- After a modest deceleration in June, July y/y inflation is expected to pick up pace again and push back to the 2% level - now of course the ECB's main price target. However, core inflation, once again a key focus for Frankfurt policymakers, is expected to slow to 0.7% y/y from 0.9% in June.

- Second quarter flash GDP will show a marked uptick from the lockdown driven 0.3% decline in Q1, with analysts forecasting a 1.6% q/q rise. the forecast 13.3% y/y recovery in Q2 will likely be the largest on record, boosted by comparisons to the economy's pandemic low in 2020.

- Friday, July 30 – U.S. Q2 Employment Cost Index

- The employment cost index likely increased 0.9% in Q2, according to Bloomberg, following another 0.9% gain in Q1.

- This quarter's release should be of particular interest to those following movements in U.S. wages, as things like hiring bonuses, which aren't included in monthly employment data from the BLS, will appear here, potentially pushing up compensation costs.

MNI Washington Bureau | +1 202-371-2121 | brooke.migdon@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok