Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (Washington)

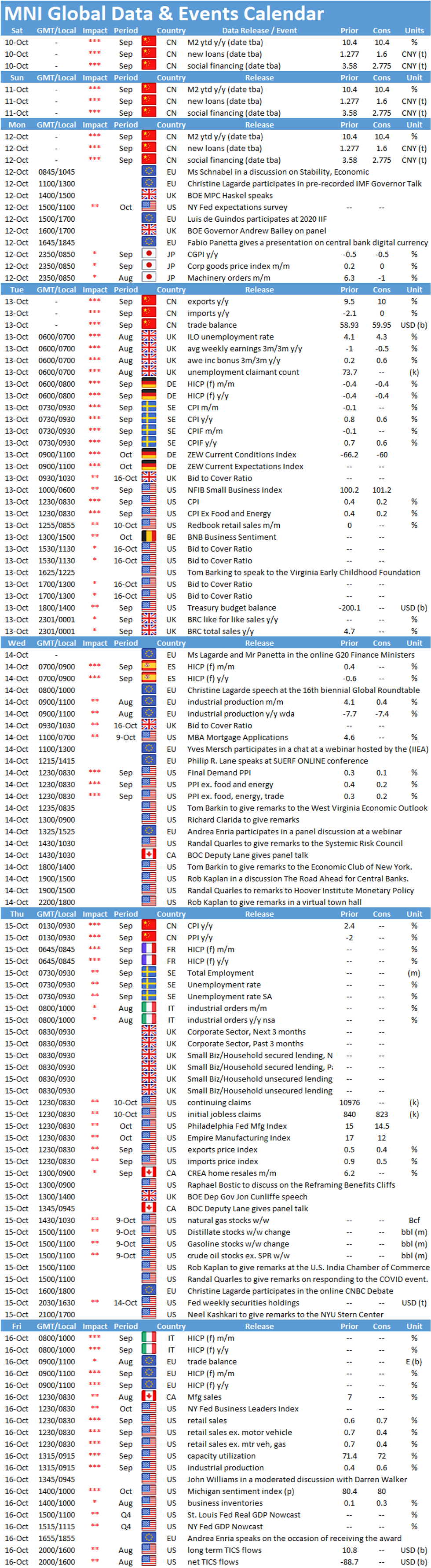

Key Things to Watch For:

- Tuesday, October 13 – U.S. CPI

- U.S. CPI likely rose 0.2% in September following a 0.4% increase in August. That will mainly reflect relatively unchanged gasoline prices last month.

- Excluding food and energy, core CPI should also rise 0.2% in September, likely due to decelerating used car and truck prices which accounted for more than 40% of the increase in core CPI in August.

- Tuesday, October 13 – German ZEW Index

- The ZEW October, expectations reading is seen easing to 70.0, down from September's reading of 77.4 on the back of improved current conditions. This would mark the lowest level since July.

- Sentiment recovered quickly after it plunged in March, however, the renewed increase in Covid-19 cases and subsequent stricter restrictions pose a downside risk to the recovery. The economic situation improved significantly in September, rising by 15.1pt to -66.2 and markets look for a fall to 61.5.

- The recently released Sentix index is in line with market forecasts. The headline index edged slightly higher with current conditions improving to the highest level since March, while expectations cooled for the second consecutive month. The Gfk consumer climate indicator saw confidence broadly unchanged heading into October and the report noted that economic and income expectations rose, while the propensity to buy fell.

- Friday, October 16 – U.S. Retail Sales

- U.S. retail sales likely increased 0.7% in September after rising 0.6% in August. Headline sales should be propped up by still-strong foodservice sales, though still decelerating from gains earlier in the summer.

- Excluding motor vehicle sales, September retail sales likely rose 0.4%. Excluding motor vehicle and gas station sales, retail sales should be up 0.4%.

- Analysts say pent up demand is finally drying up and the waning impact of government aid to consumers and businesses has reduced spending power.

MNI Washington Bureau | +1 202-371-2121 | brooke.migdon@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok