Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (Washington)

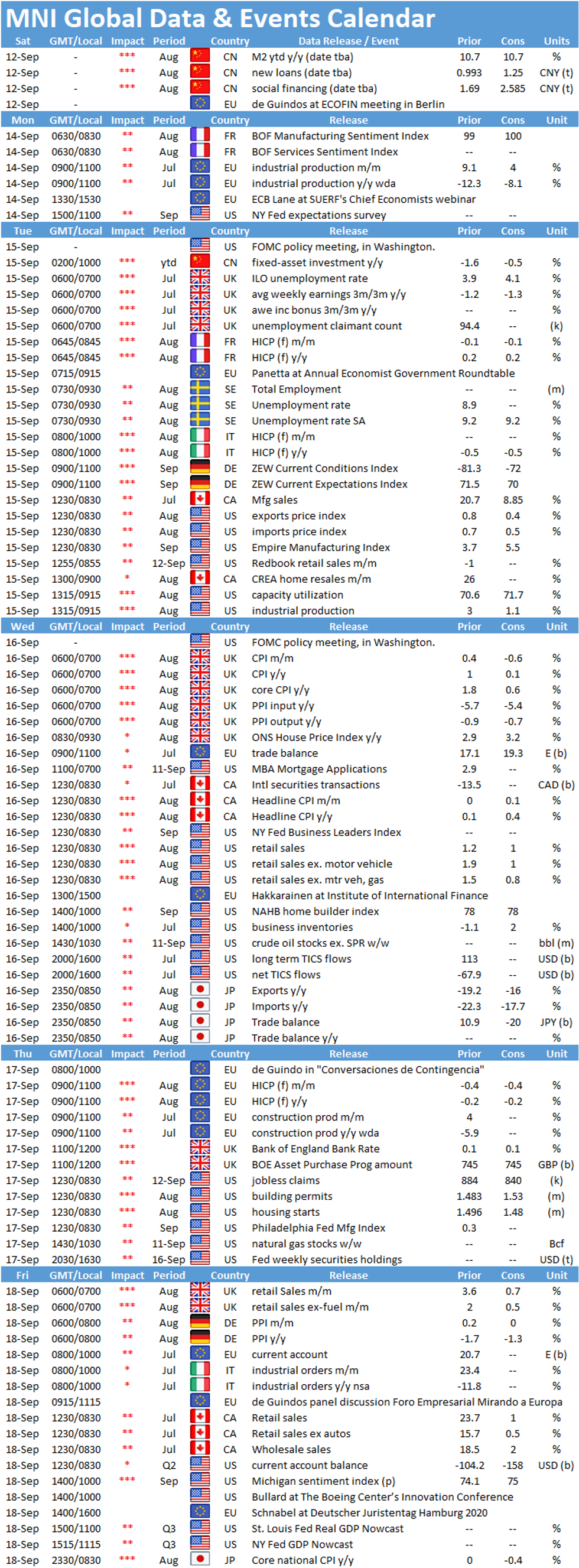

Key Things to Watch For:

- Wednesday, September 16 – U.S. Retail Sales

- U.S. retail sales likely rose 1.2% in August, the same as July, losing momentum from earlier in the summer.

- Vehicle sales should increase in August, evidenced in part by surging used car and truck prices in Friday's CPI report. Gas prices also rose in August, which should give a boost to gas station sales

- Excluding motor vehicle sales, retail sales should increase 1.1%. Excluding both vehicle and gas station sales, retail sales should also rise 1.1%.

- Wednesday, September 16 – FOMC Policy Meeting

- Fed set to issue new forecasts extending out to 2023, making these and estimates for the path of interest rates central to this meeting.

- This month's policy meeting comes with an unusual level of doubt about what else the Fed might deliver--some in markets have argued forward guidance is imminent, but MNI has exclusively reported that policymakers are likely not ready to deliver it.

- Fed watchers will be paying close attention to any changes to the Fed's July statement that economy and employment "picked up somewhat in recent months but remained well below their levels at the beginning of the year."

- Powell will likely face questions on future Fed action, the lack of a new fiscal stimulus and dollar weakness, among other themes, during his press conference.

- Thursday, September 17 – Bank of England Policy Decision

- The Bank of England's Monetary Policy Committee policy decision is due Thursday and expectations are for rates to remain on hold at 0.1%, with the stock of QE maintained at a combined GBP745 billion.

- All focus will be on the minutes and any comments offered by the governor Andrew Bailey following the meeting, although as of now, there is no confirmation of a press briefing post-meet. The messages have been mixed from policymakers in recent weeks, with Chief Economist Andy Haldane leading a fairly upbeat charge on the data that has come through so far after the trough of April and May.

- However, others, including external member Michael Saunders, have appeared less upbeat and certainly see the threat of the growing downside risks building particularly on the employment front.

- So on balance no policy action expected, although any commentary could appear to be on the dovish side, with a possible hint towards further policy action later in the year.

MNI Washington Bureau | +1 202-371-2121 | brooke.migdon@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok