Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (Washington)

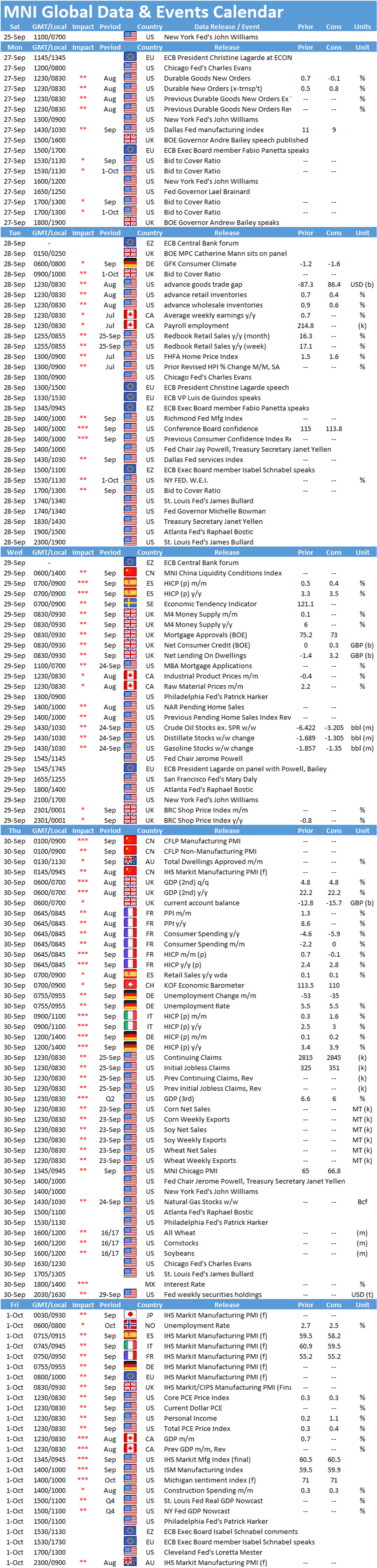

Key Things to Watch:

- Thursday, September 30 – German Inflation

- Inflation will continue to be a dominant theme in Germany in coming days, with annual rates expected to push even higher. Preliminary harmonized readings are expected to see German inflation rise to 3.9% y/y in September, up sharply from the already elevated 3.4% seen in August.

- From a communications perspective, the rise in domestic prices to 4.1% y/y will create problems for the ECB, with a notoriously inflation-resistant German public growing increasingly antsy about higher prices.

- Friday, October 1 – U.S. ISM Manufacturing

- U.S. manufacturing activity slowed in September as ongoing supply chain disruptions and severe storms through the month hampered production.

- The ISM manufacturing index slowed slightly in September, according to Bloomberg, falling to 59.5 from 59.9 in August.

- Friday, October 1 – U.S. Personal Income

- Goods spending increased through September as the spread of the Delta variant put downward pressure on demand for services. Personal spending likely rose 0.6% in September following a 0.3% gain in August, according to Bloomberg.

- The effects of stimulus earlier in the year have waned significantly, but that weakness could be partially offset by higher wages offered amid the ongoing labor shortage, with Bloomberg forecasting a 0.2% increase in personal income in September compared to a 1.1% gain in August.

MNI Washington Bureau | +1 202-371-2121 | brooke.migdon@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok