Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

While the fall in CPI rates appear to have bottomed, inflation remains deep in negative territory, with prices continuing to decline at an annual rate of 0.7%. This is unlikely to phase the SNB, however, with the Bank likely satisfied with their current expansionary policy. Downside pressure on EUR/CHF has alleviated and EUR rates markets are signalling little chance of a further cut to the ECB's deposit rate, lessening the pressure on the SNB to take any near-term policy action to maintain the rate differential.

Throughout 2020, the Bank have made clear that they still have room to manoeuvre on interest rates. But, it's clear that – for the time being - this suite of tools has succeeded in containing financial market fragmentation. As such, the Bank will likely reaffirm their vigilance this quarter, stressing that the CHF is "even more highly valued", but decline to cut rates or expand their current toolkit amid a calmer market outlook.

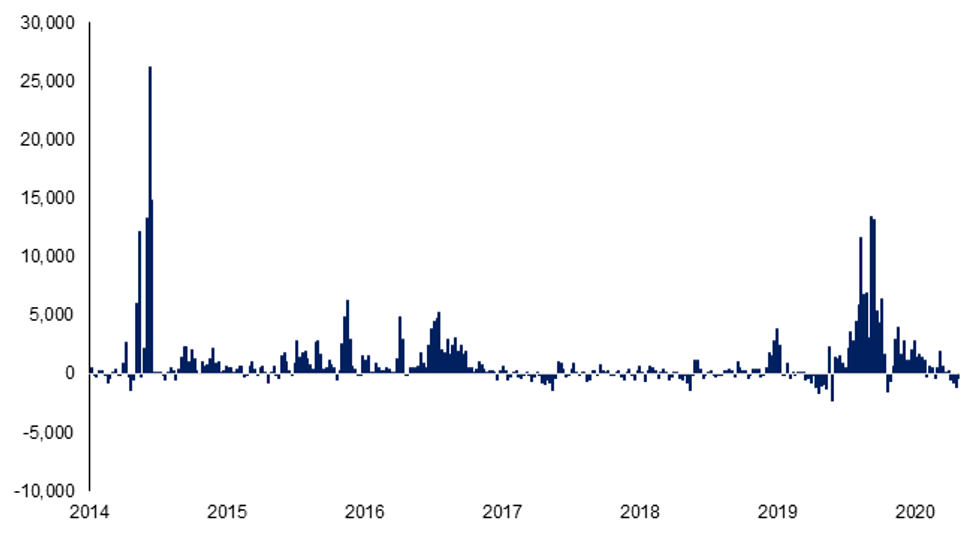

Figure 1: SNB haven't felt the need to intervene materially in currency markets for months

This makes it likely that the SNB will stress that policy tools outside of interest rates will be favoured in any further downturn, with the bank's COVID-19 refinancing facility, FX intervention and tiering multiplier likely more favoured options over a broader rate cut, which would face fierce political opposition domestically.

Full preview here:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.