RIKSBANK

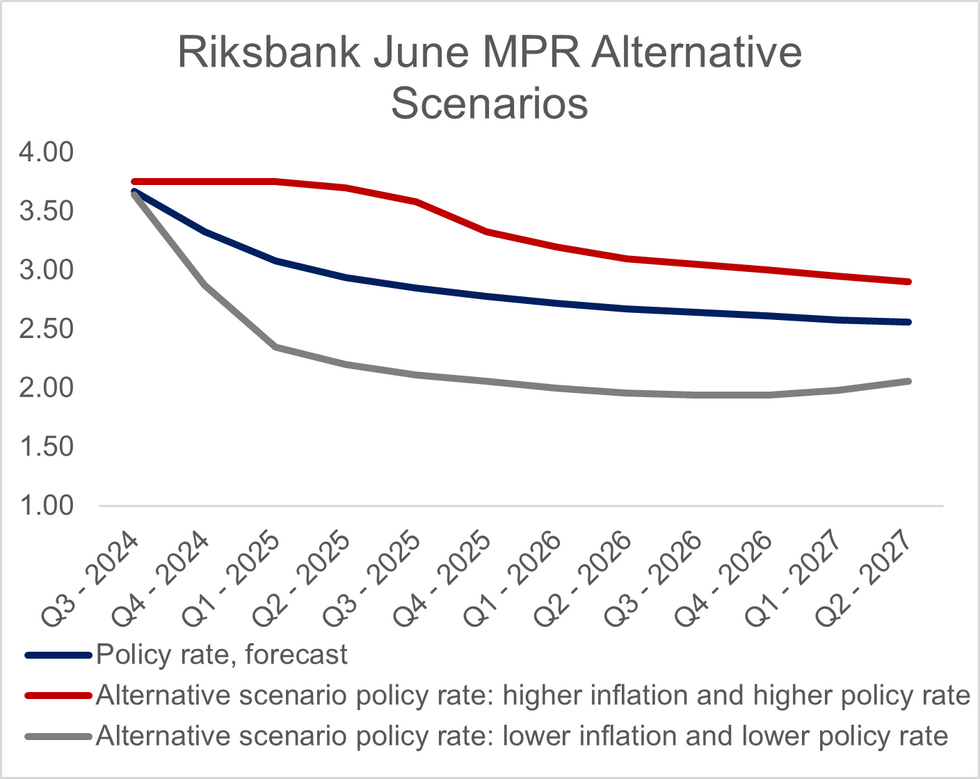

Stronger than expected external demand is cited as an upside risk to the Riksbank’s updated rate path. This scenario would see rates being held at current levels (3.75% into Q1 2025).

- The Riksbank also referenced stronger developments abroad as an upside risk in the March MPR.

- The “low inflation scenario”, which in recent quarters has been a better reflection of actual inflation developments than the main scenarios, considers the case where inflationary pressures are lower than forecasted.

- Unsurprisingly, this scenario sees more cuts in the near-term, with policy rates settling around 2% at the end of the forecast horizon.

- Rounding out the rest of the forecasts, unemployment is expected to be a little higher through the forecast horizon, while CPIF ex-energy has been revised lower.

- GDP growth is expected to be flat in Q2 2024, before rising to around 0.5% Q/Q in the second half of the year. The KIX index forecast is broadly unchanged.

165 words