Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY:

Tsy futures broadly higher after the bell, strong tail-wind for rates all session with equities selling off, ESZ0 breaching 50-day EMA (50% retrace back to Sep low in second half). Limited data, Fed in media black-out through Nov 7.

- No single driver for the risk-off tone, though virus lock-down and/or vaccine efficacy concerns, election anxiety and stimulus talks all remain factors. On stimulus, WH advisor Kudlow said there were a "NUMBER OF AREAS IN PELOSI PLAN THAT TRUMP CAN'T ACCEPT" Bbg.

- Equities did recover off steep losses after midday when "BIDEN AIDES SAY HE'LL PUSH $2T STIMULUS PACKAGE IF ELECTED," FBN.

- Average volumes by the close (TYZ>1M), but pace slowed significantly in the second half, participants close to the sidelines soon after London session close.

- The 2-Yr yield is down 0.8bps at 0.1474%, 5-Yr is down 2.7bps at 0.3493%, 10-Yr is down 4.4bps at 0.7993%, and 30-Yr is down 4.9bps at 1.5923%.

TECHNICALS: US 10YR FUTURE TECHS:

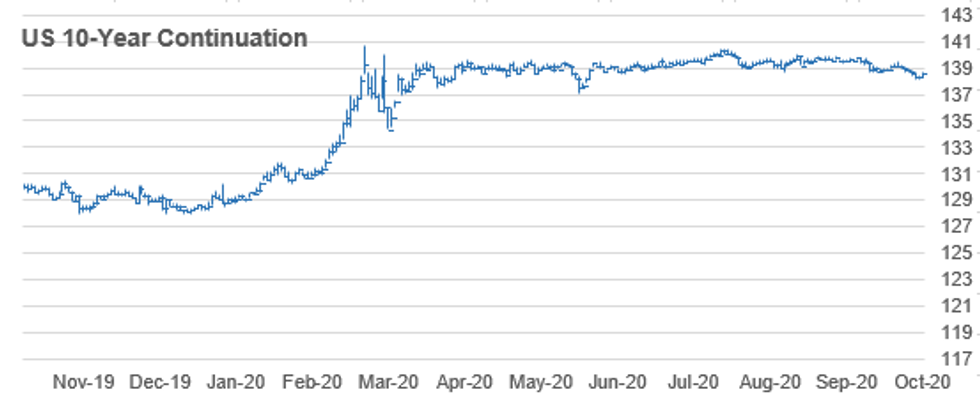

US 10YR FUTURE TECHS: (Z0) Bouncing, but Still Weak

- RES 4: 139-14 High Oct 15

- RES 3: 139-04+ 50-day EMA

- RES 2: 138-30+ 20-day EMA

- RES 1: 138-23 High Oct 26

- PRICE: 138-20 @16:25 GMT Oct 26

- SUP 1: 138-05 Low Oct 23

- SUP 2: 138-04+ 1.00 Proj of Aug 4 - 28 decline from Sep 3 high

- SUP 3: 138-01 Bear channel base drawn off the Aug 4 high

- SUP 4: 137-29 76.4% retracement of the Jun - Aug rally (cont)

Despite the bounce Monday, Treasuries remain in a downtrend following the recent sell-off. A bearish theme was reinforced on Oct 21 following the break of 138-20+, Oct 7 low. The move lower confirmed a resumption of the broader reversal that occurred on Aug 4 and clears the way for an extension lower. This has opened 138-04+ next, a Fibonacci projection ahead of 138-01, a bear channel base drawn off the Aug 4 high. Initial resistance is seen at 138-20+.

AUSSIE 3-YR TECHS:

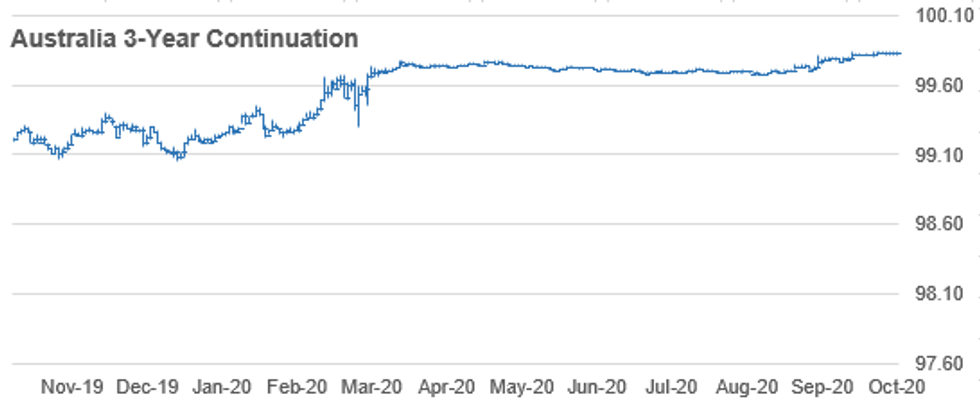

AUSSIE 3-YR TECHS: (Z0) Looking To Clear Resistance

AUSSIE 3-YR TECHS: (Z0) Looking To Clear Resistance- RES 3: 100.00 - Psychological round number

- RES 2: 99.886 - 3.0% Upper Bollinger Band

- RES 1: 99.845 - All time High Oct 20, 15 and the bull trigger

- PRICE: 99.835 @ 16:32 BST Oct 26

- SUP 1: 99.760 - Low Oct 1 and 2

- SUP 2: 99.705 - Low Sep 18, 21 and 22

- SUP 3: 99.675 - Low Sep 7 and key support

Aussie 3yr futures are largely unchanged and remain bullish. The price surge at the tail-end of September and early October confirmed bullish trend conditions. Recent activity is viewed as a pause in the uptrend and in pattern terms has taken on the appearance of a bull flag. This is a continuation pattern and reinforces current trend conditions. A break of 99.845, Oct 20 high and last week's high would open 99.889. Support is at 99.760.

AUSSIE 10-YR TECHS:

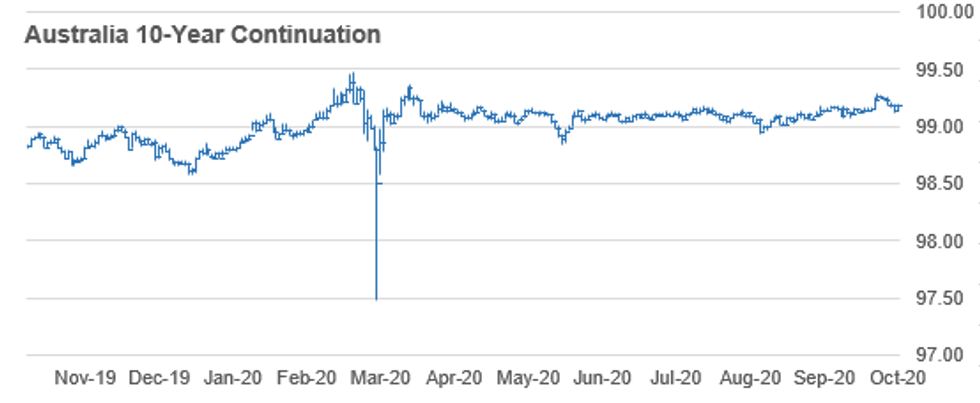

AUSSIE 10-YR TECHS: (Z0) Uptrend Remains Intact

- RES 3: 99.480 - High Mar 10 and the all-time high

- RES 2: 99.360 - High Apr 2 (cont)

- RES 1: 99.290 - High Oct 16

- PRICE: 99.190 @ 16:33 BST Oct 26

- SUP 1: 99.112 - 50-dma

- SUP 2: 99.055 - Low Sep 18 and 21

- SUP 3: 98.970 - Low Sep 8

Aussie 10y futures remain bullish despite last week's pullback. The break above 99.180, an area of congestion reflecting highs in Sep and early October confirmed a resumption of the uptrend that started on Aug 28. Attention turns to 99.300 and 99.360. The latter is the Apr 2 high (cont). The near-term bull trigger is 99.290, Oct 16 high. On the downside, firm trend support is at 99.075, Oct 5 low.

JGB TECHS:

JGB TECHS: (Z0) Either Side of 152

- RES 3: 152.55 - High Aug 5 (cont)

- RES 2: 152.36- 3.0% Upper Bollinger Band

- RES 1: 152.29 - High Sep 24 and the bull trigger

- PRICE: 151.97 @ 16:37 BST Oct 26

- SUP 1: 151.75 - Low Oct 08 and trend support

- SUP 2: 151.54 - Low Sep 7

- SUP 3: 151.43 - Low Sep 1

JGBs continue to trade either side of the 152 handle, countering the recent positive outlook. Attention remains on 152.29, Sep 4 high, a key resistance and the bull trigger. A break of this level would confirm a resumption of the uptrend and open 152.36, a Bollinger band objective and 152.55, Aug 5 high (cont). On the downside, key trend support has been defined at 151.75, Oct 8 low.

TSY FUTURES CLOSE:

Broadly higher after the bell, strong tail-wind for rates all session with equities selling off, ESZ0 breaching 50-day EMA (50% retrace back to Sep low in second half). Yld curves bull flatten, update:

- 3M10Y -3.598, 71.315 (L: 69.544 / H: 73.315)

- 2Y10Y -3.551, 64.996 (L: 64.159 / H: 67.608)

- 2Y30Y -4.126, 144.223 (L: 142.931 / H: 147.446)

- 5Y30Y -2.049, 124.235 (L: 123.332 / H: 126.1)

- Current futures levels:

- Dec 2Y +0.25/32 at 110-13.3 (L: 110-13 / H: 110-13.75)

- Dec 5Y +3.25/32 at 125-21.75 (L: 125-18 / H: 125-23)

- Dec 10Y up 9/32 at 138-20.5 (L: 138-11 / H: 138-23)

- Dec 30Y up 1-1/32 at 173-20 (L: 172-22 / H: 173-30)

- Dec Ultra 30Y up 2-10/32 at 216-17 (L: 214-13 / H: 217-05)

US EURODLR FUTURES CLOSE:

Moderately higher across the strip, near session highs with Golds outperforming all session; lead quarterly EDZ0 holding steady since 3M LIBOR set' +0.00575 to 0.22225% (-0.00188 last wk).

- Dec 20 steady at 99.755

- Mar 21 +0.005 at 99.790

- Jun 21 steady at 99.795

- Sep 21 steady at 99.800

- Red Pack (Dec 21-Sep 22) +0.005 to +0.010

- Green Pack (Dec 22-Sep 23) +0.015 to +0.030

- Blue Pack (Dec 23-Sep 24) +0.035 to +0.045

- Gold Pack (Dec 24-Sep 25) +0.045 to +0.055

US DOLLAR LIBOR: Latest settles

- O/N -0.00075 at 0.08063% (+0.00025 last wk)

- 1 Month -0.00475 to 0.15150% (+0.00487 last wk)

- 3 Month +0.00575 to 0.22225% (-0.00188 last wk)

- 6 Month -0.00313 to 0.24625% (-0.00812 last wk)

- 1 Year -0.00463 to 0.33200% (+0.00163 last wk)

US TSYS: Short Term Rates

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.09% volume: $61B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $183B

- Secured Overnight Financing Rate (SOFR): 0.08%, $915B

- Broad General Collateral Rate (BGCR): 0.06%, $334B

- Tri-Party General Collateral Rate (TGCR): 0.06%, $313B

- (rate, volume levels reflect prior session)

- Tsy 7Y-20Y, $3.601B accepted vs. $11.784B submission

- Next scheduled purchase:

- Tue 10/27 1010-1030ET: Tsy 20Y-307Y, appr $1.750B

- Wed 10/28 Next forward schedule release at 1500ET

OUTLOOK: Look Ahead To Tuesday

- US Data/Speaker Calendar (prior, estimate)

- 27-Oct 0830 Sep durable goods new orders (0.5%, 0.5%)

- 27-Oct 0830 Sep durable new orders ex transport (0.6%, 0.4%)

- 27-Oct 0855 24-Oct Redbook retail sales m/m (1.0%, --)

- 27-Oct 0900 Aug FHFA Home Price Index (1.0%, 0.7%)

- 27-Oct 0900 Aug Case-Shiller Home Price Index (0.55%, 0.40%)

- 27-Oct 1000 Q3 housing vacancies rate

- 27-Oct 1000 Oct Conference Board confidence (101.8, 101.9)

- 27-Oct 1000 Oct Richmond Fed Mfg Index (21, 18)

- 27-Oct 1030 Oct Dallas Fed services index

- 27-Oct 1130 $30B US Tsy 42D Bill CMB auction (9127963J6)

- 27-Oct 1130 $30B US Tsy 119D Bill CMB auction (912796XE4)

- 27-Oct 1300 $54B US Tsy 2Y-Note auction (91282CAR2)

PIPELINE: Back To The Sidelines

Expect more issuance from financial names as they exit earnings

- Date $MM Issuer (Priced *, Launch #)

- 10/?? $Benchmark Kommuninvest short 2Y TBA

- -

- $2.5B Priced late Friday; $33.35B/wk

- 10/23 $2.5B *Citigroup 4NC3 fix/FRN +48

EURODOLLAR/TREASURY OPTIONS

Eurodollar Options:

- +9,600 Dec 100 calls, cab

- +5,000 Red Dec 100 calls, 3.0

- +1,500 Blue Dec 91/97 1px3c risk reversals, 2.0 net vs. 99.52/0.30%

- +2,000 Gold Dec 88/91 put spds, 4.25

- +1,500 Green Dec 95/96 put spds, 2.0

- Overnight trade

- Block, 5,000 90/91/93 put trees, 4.5 at 0743:25ET

- -5,000 FVZ 125.75 calls, 13.5

- +5,000 TYZ 136.5 puts, 6/64

- +2,000 TYZ 141 calls, 3/64

- >4,200 TYZ 138.5 straddles, 117-116

- +1,000 USF 169/174 3x2 put spds, 132

- BLOCK, -15,669 TYF 136.5/139.5 strangles, 40/64 at 1047:56ET, adds to heavy sales late last week

- -4,000 TYZ 138 puts 6/64 over TYF 136.5 puts

- +2,000 wk5 TY 137.75 puts, 2

- 1,000 TYF 137.5 puts, 37/64

- Overnight trade

- Block, +5,000 USZ 172/177 put over risk reversals, 52/64

- 7,200 TYZ 139.5 calls, 15/64

- 3,700 TYF 139.5 calls, 21/64

- +3,000 wk5 TY 137.7/138 put spds, 2/64

- 2,500 FVZ 126 calls, 6.5/64

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.