Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI US MARKETS ANALYSIS - USD Weakens

HIGHLIGHTS

- The US dollar has come under pressure against G10 currencies

- UK job gains exceeded expectations

- Brent crude touched USD70/b

US TSYS SUMMARY: Infrastructure And Housing Provide Tuesday's Themes

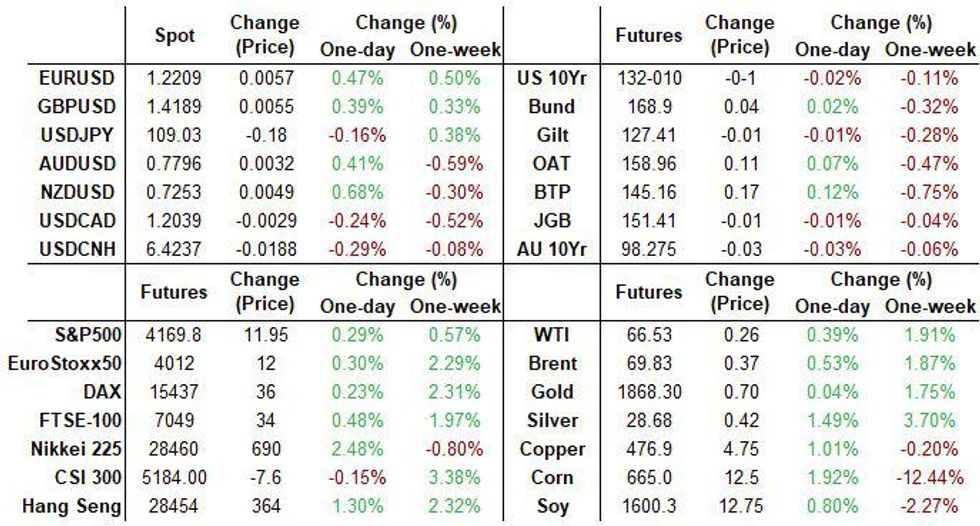

Largely sideways trade for Tsys overnight Tuesday on limited volumes, as the space has largely shrugged off stronger equity futures and a decent drop in the dollar.

- Jun 10-Yr futures (TY) down 1/32 at 132-10 (L: 132-07.5 / H: 132-11.5), just over ~200k traded.

- The 2-Yr yield is unchanged at 0.1531%, 5-Yr is down 0.8bps at 0.8275%, 10-Yr is down 0.3bps at 1.6454%, and 30-Yr is up 0.4bps at 2.367%.

- DXY dollar index off 0.4%; tech leading overnight equity gains, NASDAQ futs up 0.7%.

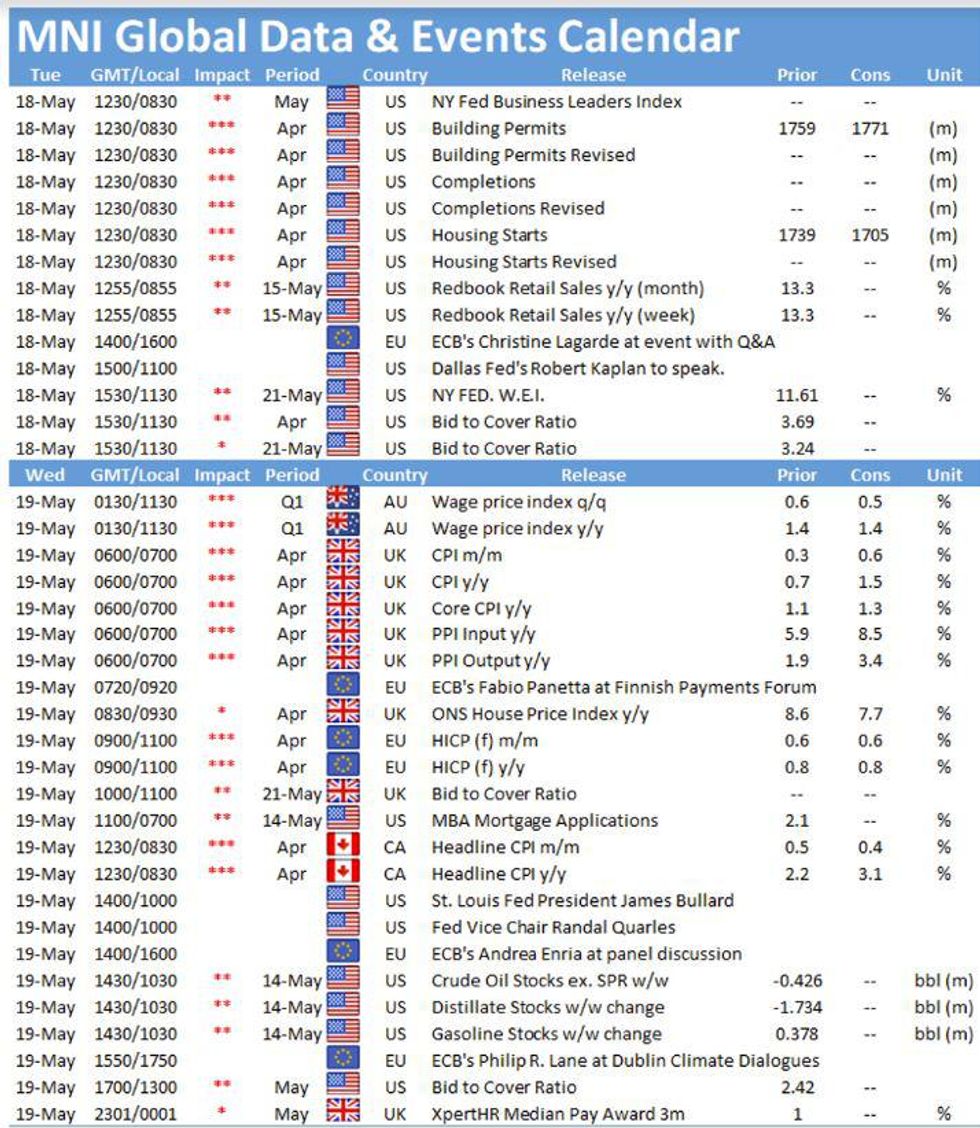

- Today's data is all about housing: building permits and housing starts at 0830ET.

- Treas Sec Yellen speaking at a Chamber of Commerce event at 0915ET, subject "Building a Better Deal for All Americans" - no specifics provided but presumably will include commentary on post-pandemic economic recovery, including White House's infrastructure plan.

- On that note, Senate Republicans expected to present a new proposal on infrastructure to Biden admin officials today, no time provided.

- Dallas Fed's Kaplan in a moderated discussion at 1105ET.

- In supply, $74B total in 42-D / 52-W bill auctions at 1130ET. NY Fed buys ~$1.2B of 7.5-30Y TIPS.

EGB/GILT SUMMARY: A Mixed Start

European sovereign bonds initially traded weaker, with EZ sovereigns firming through the session.

- Gilts continue to trade below yesterday's close with cash yields <1bp higher on the day.

- Bunds recovered early losses and now trade close to flat.

- The OAT curve has flattened a touch on the back of the long-end firming. The 2s30s spread is 1bp narrower.

- BTPs have firmed with yields ~1bp lower.

- UK employment data came in stronger than expected for March (84k 3M/3M vs 50k survey) and the unemployment rate dipped (4.8% vs 4.9% expected. Wage data was mixed (the exc bonus data matched expectations, while the headline figure was significantly lower than expected: 4.0% Y/Y vs 4.5% survey)

- Supply this morning came from the UK (Gilts, GBP5.5bn), Germany (Schatz, EUR4.849bn allotted) and the ESM (Bills, EUR1.5bn).

EUROPE ISSUANCE UPDATE

GERMAN AUCTION RESULTS: New 0% Jun-23 Schatz

Weak, technically uncovered auction.

| 0% Jun-23 Schatz* | Previous | |

| Allotted | E4.849bln | E4.085bln |

| Avg yield | -0.66% | -0.69% |

| Bid-to-cover | 0.91x | 1.09x |

| Buba cover | 1.13x | 1.33x |

| Price | 101.379 | |

| Previous date | 20-Apr-21 | |

| Total sold | E6.0bln | E5.0bln |

*Previous auction is of 0% Mar-23 Schatz

UK AUCTION RESULTS: DMO sells GBP2.25bln of the 1.25% Oct-41 gilt

| 1.25% Oct-41 Gilt | Previous | |

| Amount | GBP2.25bln | GBP2.25bln |

| Avg yield | 1.392% | 1.223% |

| Bid-to-cover | 2.49x | 2.52x |

| Tail | 0.1bp | 0.1bp |

| Avg price | 97.491 | 100.488 |

| Pre-auction mid | 97.372 | |

| Previous date | 09-Mar-21 |

UK AUCTION RESULTS: DMO sells GBP3.25bln of the 0.125% Jan-24 gilt

| 0.125% Jan-24 Gilt | Previous | |

| Amount | GBP3.25bln | GBP3.25bln |

| Avg yield | 0.189% | 0.150% |

| Bid-to-cover | 2.60x | 2.70x |

| Tail | 0.1bp | 0.2bp |

| Avg price | 99.827 | 99.931 |

| Pre-auction mid | 99.812 | |

| Previous date | 20-Apr-21 |

ESM AUCTION RESULTS: E1.5bln of 6-month bills sold

| Type | 6-month bills |

| Maturity | Nov 18, 2021 |

| Amount | E1.5bln |

| Target | E1.5bln |

| Previous | E1.5bln |

| Avg yield | -0.613% |

| Previous | -0.608% |

| Bid-to-cover | 6.96x |

| Previous | 6.28x |

| Previous date | Apr 20, 2021 |

EUROPE OPTIONS FLOW SUMMARY

RXQ1 161p, bought for 2 in 7.4k

3LU1 98.62/98.37/98.25p fly, bought for 1.75 in another 4k (7k total)

FOREX - USD Under Pressure

USD under pressure throughout our European morning session.

- A continuation from the overnight Asian risk on session.

- Commodity bid helps the Kiwi and Aussie at the top of the pile in G10.

- A little perplexed by the risk on bid, which looked to have been driven by a tech bounce, although surprising given supply chain issues.

- The Dollar is struggling across the board with the EURUSD testing initial resistance at 1.2218 at the time of typing.

- Similar story for the British Pound also supported as the UK enter the next step in re-openings.

- Cable is testing trendline resistance circa 1.4216 (printed a 1.4220 high so far)

- The Greenback tested new session low against EUR, GBP, CHF, AUD, SEK, NOK, PHP, INR,, TWD, MYR, and IDR.

- Looking ahead, very little on the data front, but still plenty of speakers are scheduled, including BoE Bailey, Broadbent and Ramsden.

- ECB Lagarde at a prize ceremony, and Fed Kaplan in a panel discussion.

FX OPTION EXPIRY

FX OPTION EXPIRY (updated) Nothing too close.- AUDUSD:; 0.7750 (1bn)

- USDCAD: 1.1945 (887mln)

Price Signal Summary - USD Under Pressure

- In the equity space, the trend outlook remains bullish. S&P E-minis are holding onto recent gains. A key support has been defined at 4029.25, May 13 low. A break of this level would risk a deeper pullback. While it holds, the trend remains up.

- In the FX space, EURUSD has rallied today and cleared former resistance at 1.2182, May 11 high. With price trading above 1.2200, the focus turns to key resistance at 1.2243, Feb 25 high. GBPUSD is bullish following last week's gains. Attention is on 1.4237, Feb 24 high and this year's high. USDJPY support has been defined at 108.34, May 7 low. A bullish theme remains intact while it holds and attention is on 109.79, May 13 high. A break of support would highlight a trendline break drawn off the Jan 6 low and risk a deeper pullback. USDCAD is back below 1.2062, Sep 2017 low. Attention turns to the psychological 1.2000 handle.

- On the commodity front, Gold remains bullish. The focus is on $1875.7, Jan 29 high. Oil is stronger. Brent (N1) focus is on the psychological $70.00 level that has been probed today. A clear break would open and $71.75, Jan 8 2020 high (cont). WTI bulls are eyeing the key resistance at $67.29, Mar 8 high. Key near-term support is at $63.09, May 3 low

- In the FI space, Bunds (M1) remain vulnerable and the risk is for a revisit of the 2020 lows at 167.52. A break of 168.59, May 13 low would trigger a resumption of the downtrend. Near-term risk in Gilts (M1) is still skewed to the downside. The key support and bear trigger is 126.79, Mar 18 low. BTPs (M1) remain in a clear downtrend. The focus is on 144.16, 1.236 projection of the Feb 12 - 26 - Mar 11 price swing.

EQUITIES: Equities led higher by risk-on Asian session

- Japan's NIKKEI up 582.01 pts or +2.09% at 28406.84 and the TOPIX up 28.88 pts or +1.54% at 1907.74

- China's SHANGHAI closed up 11.398 pts or +0.32% at 3529.014 and the HANG SENG ended 399.72 pts higher or +1.42% at 28593.81

- German Dax up 52.38 pts or +0.34% at 15449.41, FTSE 100 up 28.01 pts or +0.4% at 7060.62, CAC 40 up 16.48 pts or +0.26% at 6383.83 and Euro Stoxx 50 up 15.32 pts or +0.38% at 4022.01.

- Dow Jones mini up 86 pts or +0.25% at 34344, S&P 500 mini up 13.25 pts or +0.32% at 4170.75, NASDAQ mini up 94 pts or +0.71% at 13396.75.

COMMODITIES: Levels update: Platinum falls while other commodities rise

- WTI Crude up $0.52 or +0.78% at $66.78

- Natural Gas up $0.01 or +0.32% at $3.12

- Gold spot up $1.98 or +0.11% at $1869.09

- Copper up $4.9 or +1.04% at $475.95

- Silver up $0.31 or +1.09% at $28.4885

- Platinum down $18.42 or -1.48% at $1224.84

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok