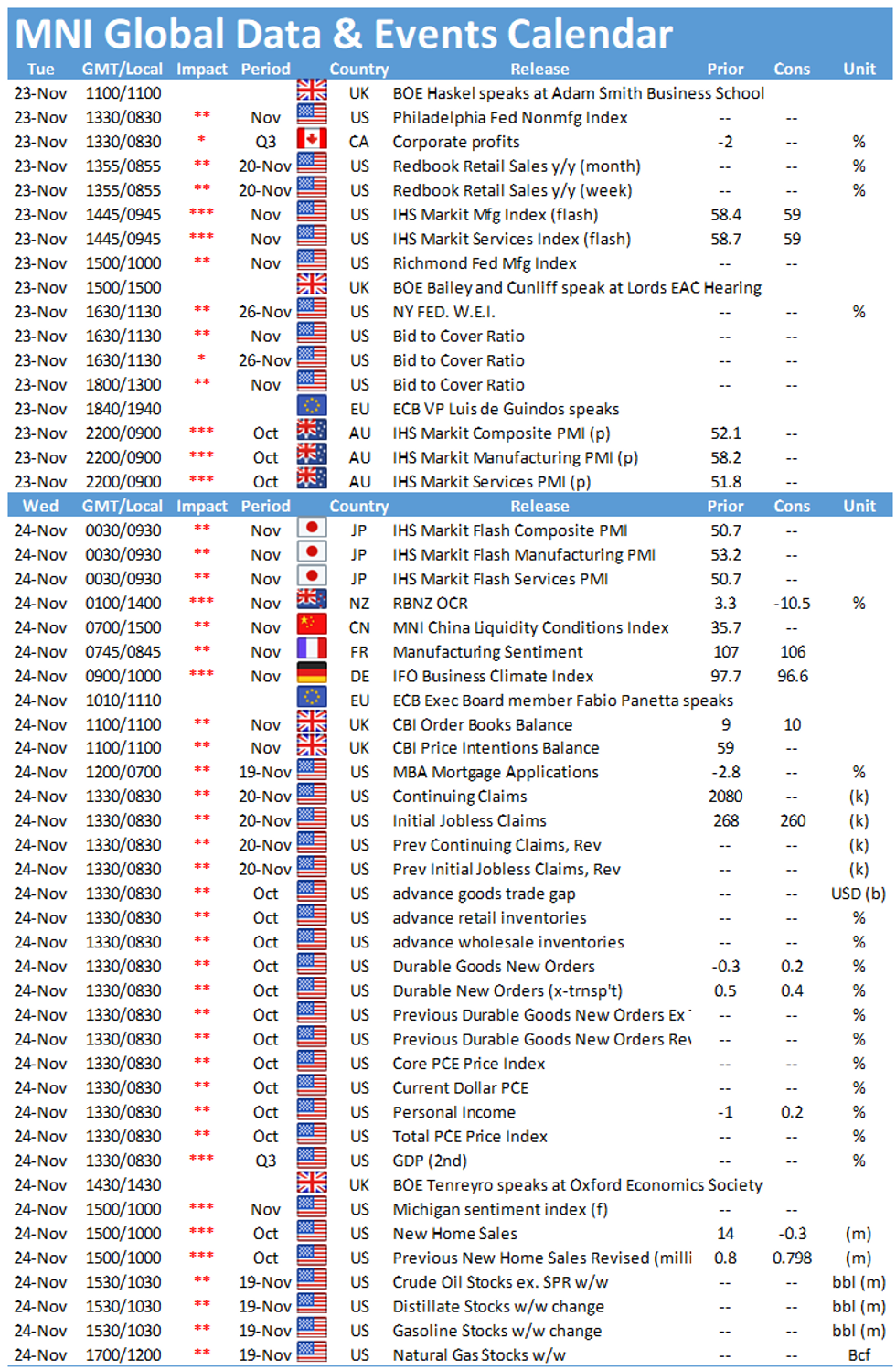

Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Bunds erase Friday rally on better-than-expected European PMI data

- EUR recovers off YTD lows printed at 1.1226

- Markets on watch for coordinated oil response ahead of Biden's inflation speech

US TSYS SUMMARY: Small Bear Steepening After Yday's Sell-Off

- Cash Treasuries have seen a limited sell-off at the longer end as they catch up on yesterday's price action following Biden's Fed picks.

- 2Y yield unchg at 0.630%, 10Y +1.7bps at 1.641% and 30Y +2.5bps at 1.987%, which sees the 2s/10s spread at 101bps and very close to flattest its been since January.

- TYZ1 down -0-06+ on the day at 129-25+ and at both session and ytd lows.

- The data focus today is on preliminary PMI for Nov (0945ET) before tomorrow's core PCE/incomes and durable goods for Oct.

- Other events of note: Biden speaking on economy/inflation at 1400ET/1900GMT and Fed minutes on Wed.

- Busy supply schedule today with $40B 35D bill (1130ET), $24B 2Y FRN (1130ET) and $59B 7Y (1300ET) auctions.

- Next scheduled NY Fed purchases: TIPS 7.5Y-30Y, appr $1.075B (1030ET)

EGB/GILT SUMMARY: Bunds Erase Friday Rally on Strong Euro PMIs

- Bund futures trade notably weaker, with the Dec-21 contract printing a new intraday low just ahead of the NY crossover. Bunds have now fully retraced the whole of Friday's rally to narrow the gap with first support at 170.88. A a clear break through the level opens yield resistance at -0.210%, which would equate to 170.41 in prices.

- Solid European PMI data has been the primary catalyst, with French and German manufacturing and services sectors growing faster than forecast.

- The Gilt curve trades bear flatter, reinforced by upbeat commentary from BoE's Haskel, who re-stated that the path of rates is upwards.

- Focus turns to US PMI data as well as Biden's speech on inflation and the economy at 1400ET/1900GMT.

EUROPE OPTION FLOW SUMMARY:

Eurozone:

DUG2 112.20/112.00/111.80p fly, bought for 4.25 in 5k

IKZ1 149/148.5/148/147.5p condor, bought for 4 in 3,030

US:

TY week3 128.50/127.5ps, bought for 17 in 12.5k

FVF2 119.75p, bought for 14.5 in 10k

EUROPE ISSUANCE UPDATE

Netherlands sells E2.1bln 0% Jan-29 DSL, Avg yield -0.280% (Prev. -0.251%), Price 102.03 (Prev. 101.85)

UK DMO Syndicates:

- Final terms on 2073 linker

- Deal Size : GBP1.1bln (as MNI expected)

- Spread set at UKTI 0.125% 22-March-2068 -3.5bps (guidance had been -3.5bps to-3.0bps)

FOREX: EUR Off the Mat as PMIs Improve

- The single currency is among the session's best performers so far Tuesday, with the EUR improving on the back of a set of better-than-expected PMI numbers across the continent. Prelim data showed growth was higher than expected across both manufacturing and services sector in France and Germany.

- This puts EUR/USD back above 1.1250 ahead of the NY crossover and thereby off the new YTD lows printed in early Asia-Pac hours at 1.1226. There's little evidence of a sustained bounce at present levels, with markets needing to top 1.1307 before indicating any further recovery.

- Elsewhere, markets are more mixed, with CAD, NZD and NOK among the session's worst performers as commodity markets trade more subdued. WTI and Brent crude futures are off over 1.5% on the day, possibly in anticipation of a coordinated release of oil reserves from some of the world's largest consumers at some point today.

- US prelim PMI takes focus going forward, with both the manufacturing and services sector seen improving from the October read. Both sectors are seen growing at a decent clip, with the data seen holding just below 60.0. The speaker slate picks up, with BoE's Bailey, Cunliffe and Haskel all due as well as BoC's Beaudry and ECB's de Guindos.

- Lastly, President Biden speaks directly on the US economy and inflation at 1400ET / 1900GMT.

OPTIONS: Expiries for Nov23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1220(E767mln), $1.1340-55(E914mln), $1.1595-00(E1.7bln)

- USD/JPY: Y114.20($840mln)

- AUD/USD: $0.7310-25(A$622mln), $0.7350-60(A$651mln)

Price Signal Summary - Treasuries Resumes Their Downtrend

- In the equity space, short-term sentiment has soured. S&P E-minis failed to hold onto yesterday's high and have traded lower since. In pattern terms, yesterday's candle is a shooting star and does highlight a potential short-term top. If correct, this leaves support at 4625.25 exposed, the Nov 10 low. Key resistance is yesterday's high of 4740.50. The recent sell-off has been steeper in EUROSTOXX 50 futures. The contract has traded through the 20-day EMA and this exposes the 50-day EMA at 4231.60. This average is a key support parameter.

- In FX, trend conditions are unchanged in the USD and the uptrend remains firmly intact. EURUSD remains in a downtrend. The pair is trading below the base of its bear channel drawn from the Jun 1 high. The focus is on 1.1222 next, 1.618 projection of the Jan 6 - Mar 31 - May 25 price swing. Resistance is at 1.1374, the Nov 18 high. The recent break in GBPUSD below 1.3412, Sep 29 low, opens 1.3334 next, 1.00 projection of the Sep 14 - 29 - Oct 20 price swing. Resistance is at 1.3520, the 20-day EMA. USDJPY has traded above last week's high and through the 115.00 handle. This confirms a resumption of the underlying uptrend with attention on 115.51 next, the Mar 10, 2017 high. Support has been defined at 113.59.

- On the commodity front, Gold sold off sharply yesterday. The metal has cleared 20- and 50-day EMAs and this opens $1785.1, Nov 5 low and possibly the base of a bull channel at $1754.6. The channel is drawn off the Aug 9 low. A bearish risk remains present in WTI following the recent breach of support at $77.23, Nov 4 low. The break has opened $74.25 next, the Oct 7 low.

- In the FI space, Bund futures have pulled back from recent highs. A deeper pullback would expose the key support at 170.06, Nov 5 low. Gilts maintain a bullish tone. Watch key support at 125.40, Nov 17 low. A break would alter the picture. Treasuries have traded below 129-31, Oct 21 low. This confirms a resumption of the downtrend and opens 129-03, 50.0% of the Oct '18 - Mar '20 bull cycle.

EQUITIES: Europe Slips, But US Markets More Resilient

- European equity markets are uniformly lower, with the EuroStoxx50 off around 1%, with German and Italian stocks posting similar losses. The UK's FTSE-100 is faring slightly better, but still trades underwater by 0.1%.

- In US futures space, indices are a little more resilient, with the e-mini S&P lower, but comfortably off the overnight lows of 4654.50. Nonetheless, the index remains within striking distance of yesterday's alltime highs at 4740.50.

- VIX futures are inching higher to complement the recent weakness off highs, putting the Dec-21 VIX future at the highest levels since mid-October.

COMMODITIES: Markets on Watch For Coordinated Oil Reserves Release

- Markets remain on watch for a possible coordinated statement from global oil consumers today, with number of countries expected to release stocks from their oil reserves in a bid to relieve high fuel prices.

- Reports over the past few days suggest India, South Korea, China and Japan will join the USA in releasing reserves, but there remain questions over both the size and timing of such a release.- India are seen selling 5mln bbls, USA releasing 35mln bbls "over time". This represents ~6% of the SPR stockpile, which stood at ~605mln bbls last week.

- China have been dripfeeding markets from reserves already as part of a broader strategy, but the details are more vague. Size of interventions tend to be at around 7mln bbls from reserves, but the frequency and size could increase as part of coordinated action.

- OPEC+'s next meeting is scheduled for next week, 2nd December. The group are seen easing production curbs by 400,000bpd - but broad intervention could work against this expectation.

- Biden speaks directly on inflation and the economy later today at 1400ET/1900GMT, with Powell's re-appointment and action on oil prices seen as key tenets of his policy against runaway prices.

- The Brent crude futures curve has flattened since the Xi-Biden summit, showing a market that's pricing in some supply relief in the coming months. An ineffective reserves release, or a pushback from OPEC+ at next week's meeting could see the front-end of the futures curve swiftly reverse recent losses.

The Brent futures curve has dropped since the Xi-Biden Summit

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok