Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- US stock futures edge off all-time highs

- Dollar holds bulk of Monday losses

- Light data calendar, Fed's Barkin speaks

US TSYS SUMMARY: Belly Underperforming

Tsys are trading mixed, with TYs a little stronger though well off session highs.

- Yields continued to fade some of the post-payrolls rise in Asia-Pac trade, but moved higher in early London trade as desks came back after a 4-day European weekend.

- Belly underperforming: 2-Yr yield is up 0.2bps at 0.1685%, 5-Yr is up 0.5bps at 0.9269%, 10-Yr is up 0.2bps at 1.7022%, and 30-Yr is down 0.3bps at 2.3432%.

- Jun 10-Yr futures (TY) up 3.5/32 at 131-07 (L: 131-03.5 / H: 131-14), volumes still on the light side though, w <300k traded as of 0630ET.

- USD edging higher, stock futures giving back a bit of Monday's gains.

- Not much in terms of headline drivers overnight: mainly focused on EU - US cooperation on global minimum corporate tax, and further Archagos fallout (Credit Suisse announcing $4.7B hit).

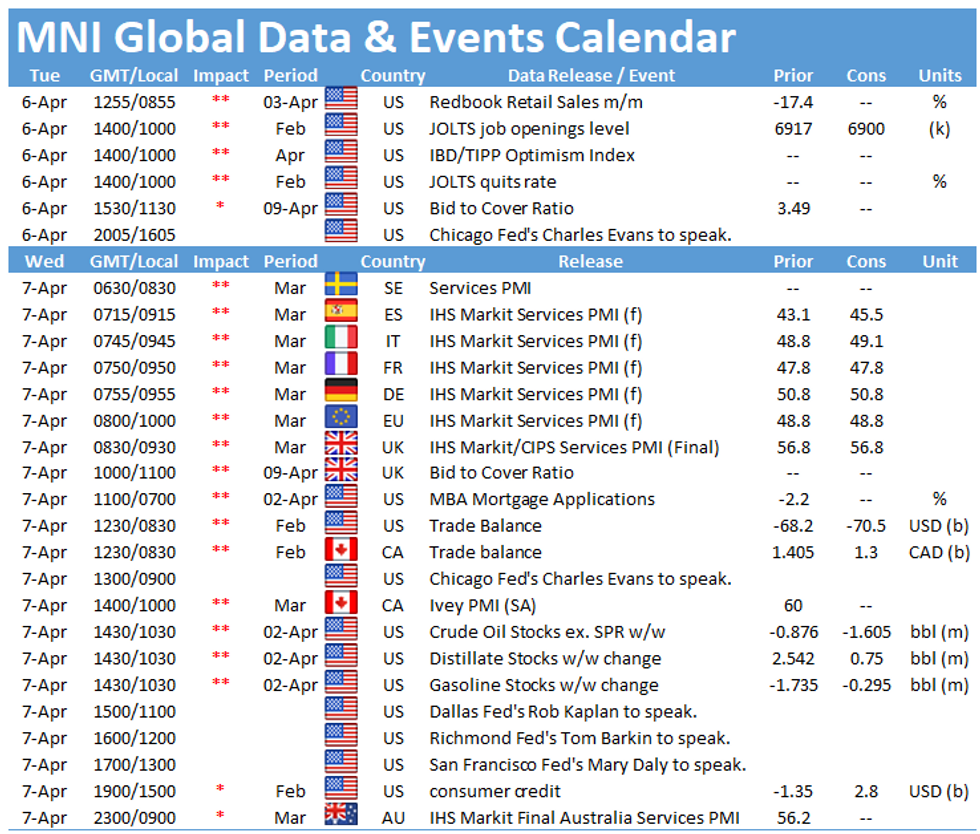

- A quiet calendar lies ahead today: data consists of Feb JOLTS (1000ET), while Richmond Fed's Barkin is the only scheduled speaker (1430ET).

- In supply, we get $40B 42-day bill auction at 1130ET. NY Fed buys ~$1.750B of 20-30Y Tsys.

EGB/GILT SUMMARY: Bear Steepening

EGBs have bear steepened, as the EU comes back from a long weekend break. German 5/30s is at session high, but well within last week's range.

- Bund and EGBs have led US treasuries lower, small move higher in US Yield, as Europe take stock of the NFP beat last Friday.

- Peripheral spreads are generally wider, Italy 2.1bp wider, with the exception of Greece, which trades 1.6bp tighter versus the German 10yr.

- Gilts have traded in tandem with EGBs, and are lower today, despite investors awaiting on any potential decision from MHRA regarding Astra's restrictions.

- Channel 4 reported that MHRA was considering the restrictions amid concerns about rare blood clots, and a decision could be made as early as today.

- Looking ahead, no tier 1 data are left for today, on this side or the other side of the pond.

- On the speaker front, Fed's Barkin takes part in a virtual discussion.

- Jun Bund futures (RX) down 46 ticks at 171.37 (L: 171.32 / H: 171.89)

- Jun BTP futures (IK) down 64 ticks at 149.11 (L: 149.07 / H: 149.88)

- Jun OAT futures (OA) down 46 ticks at 161.95 (L: 161.89 / H: 162.48)

- Italian BTP spread up 2.1bps at 98bps

- Spanish bond spread up 0.8bps at 64.4bps

- Portuguese PGB spread up 0.9bps at 54.5bps

- Greek bond spread down 0.5bps at 114.7bps

EUROPE ISSUANCE: Austrian Bond Auction

Austria sells E1.50bln of RAGB:

- E0.978bln 0% Feb-31 RAGB, Avg yield -0.104% (Prev. -0.138%), Bid-to-cover 2.03x

- E0.518bln 0.75% Mar-51 RAGB Avg yield 0.521% (Prev. 0.159%) Bid-to-cover 2.08x

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXK1 171.50/172.50cs 1x2, bought for 11 in 3.75k

RXK1 170/168ps, sold at 17/16.5 in 3k

RXK1 169/168ps, sold at 5.5 in 2k

RXM1 174/168.5^^, seems done off market and presume sold at 44 in 5k

DUK1 112.20/30cs vs 112.10p, sold the put at 2.5 in 1.25k

DUM1 112.20/30cs vs 112.00/111.90ps, sold at 0.25 in 2.5k

0RZ1 100.62/100.50ps, 1x2, bought the 1 for 0.75 in 5k (ref 100.51, 20del)

3RK1 100.25/100.12ps vs 3RJ1 100.25p x2, bought the ps for half in 2kx4k

FOREX: Dollar Holding Bulk of Monday Losses

- After Monday's weakness, USD is bouncing ahead of Tuesday NY hours, with EUR also gaining. Nonetheless, the greenback is yet to erase Monday's weakness, holding the bulk of the losses. GBP is among the session's poorest performers, although GBP/USD still managed to hit a new April high at $1.3919 before retracing.

- Both AUD & NZD also lag. The RBA rate decision overnight was unchanged - as expected - however the board stressed that they would wait for further signs of economic normalization before making any decisions on forward guidance.

- Stocks hit new alltime highs in early Asia-Pac trade, but are pulling very slightly lower ahead of NY hours. The e-mini S&P is off around 0.2% but remains above the key 4,000 level that was topped late last week.

- There are no major data releases among developed markets Tuesday, with February JOLTs job openings numbers the only notable release. Fed's Barkin is due to take part in an online discussion at 1930BST/1430ET.

FX OPTIONS: Expiries for Apr06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800-05(E1.9bln, E1.5bln of EUR puts), $1.1825(E889mln-EUR puts), $1.1845-50(E400mln), $1.1870-80(E483mln-EUR puts), $1.1975-95(E1.4bln), $1.2000-05(E1.1bln)

- USD/JPY: Y107.65-80($1.8bln), Y108.00-05($761mln), Y108.70($810mln), Y110.00-10($638mln)

- GBP/USD: $1.3750(Gbp461mln)

- EUR/GBP: Gbp0.8700(E620mln)

- AUD/USD: $0.7640-50(A$975mln-AUD puts), $0.7725-35(A$812mln)

Price Signal Summary - E-minis Comfortable Above 4000

- In the equity space, S&P E-minis have cleared the psychological 40000.00 level and appear comfortable above this former key hurdle. The focus is on 4080.99, 1.236 projection of the Feb 1 - Feb 16 - Mar 4 price swing. EUROSTOXX 50 is trading higher too and approaching 4000. A break would open 4047.72, 2.236 projection of the Dec 21 - Jan 8 - Jan 28 price swing

- In the FX space, EURUSD gains are considered corrective. The next resistance is 1.1828, a former bear channel base drawn off the Jan 6 high. A break of this level would suggest scope for a stronger bounce. The GBPUSD outlook remains bearish. Recent gains have stalled at the former bull channel base drawn off the Nov 2 low. Resistance has been defined at 1.3919, today's intraday high. USDJPY remains bullish and pullbacks are considered corrective. The focus is on 111.30 next, Mar 26, 2020 high.

- On the commodity front:

- Gold is holding onto recent gains. Key resistance is at $1755.5, Mar 18 high, where a break is required to suggest scope for a stronger bounce.

- Brent (M1) key directional triggers are:

- Resistance at $65.39, Mar 29 high and key support at $60.33, Mar 23 low and the bear trigger

- WTI (K1) directional triggers are:

- Resistance at $62.27, Mar 30 high and support at $57.25, Mar 23 low and the bear trigger

- In the FI space, Bunds (M1) remain vulnerable. Key support to watch is at 170.52, Mar 18 low. The key support and bear trigger in {GB} Gilts (M1) is at 126.79, Mar 18 low.

EQUITIES: Continental Markets Play Catch-Up, Gap Higher

- Stock markets on the continent are higher, with gains of around 1% for the core European indices. European markets are following the US' lead after the very positive close on Monday, with sentiment persisting overnight as the e-mini S&P holds above 4,000 and touched a new all time high in early Asia-Pac hours at 4,074.50.

- The UK's FTSE-100 outperforms as GBP trades softer in currency markets. Italy's FTSE-MIB and France's CAC-40 lag slightly, but still hold gains of just over 0.5%.

- Across Europe, materials and financials are leading gains, with communication services the only sector in the red.

- Notable outperformers include Volkswagen (higher by over 2% as they rotate to electric vehicles), Banco Santander and Adidas.

COMMODITIES: WTI, Brent Bounce But Still Heavy on the Week

- The Vienna meeting between representatives of the European Union, US and Iran this week remains a focus, with markets watching for any reconciliation that could lead to Iranian oil supply re-entering the global market.

- For WTI and Brent crude futures key directional triggers remain at $65.41, the Apr 1 high in Brent and key support at $60.33, Mar 23 low and the bear trigger. For WTI, directional triggers are $62.27, Mar 30 high and support at $57.25, Mar 23 low and the bear trigger.

- In precious metals markets, gold gave up early gains, with a slightly firmer greenback helping pull prices a little lower throughout the European morning. Silver slightly outperforms, higher by just over 0.25% at pixel time.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.