Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- European national inflation data provides the focus ahead of U.S. data.

- Bonds and USD off highs.

- Fed highlights broader docket, with various U.S. data releases and German CPI also eyed.

MNI Fed Preview - Jan 2024: Dropping The Tightening Pretense

The Federal Reserve will hold rates steady for the 5th time in 6 meetings in January, further cementing expectations that the hiking cycle is over and that the next move will be a cut.

- Given participants’ pushback against 2024 market rate cut pricing since the December meeting, the main question will be the degree to which the Statement and Chair Powell leave the door open to a rate cut as soon as March.

- There is a good chance that the forward guidance will be amended to remove the tightening bias in favor of a more neutral stance, in light of recent disinflationary progress.

- But the FOMC will be wary of signaling a March cut, and will re-emphasize a patient data dependent approach.

- The FOMC is also expected to discuss plans to slow the pace of quantitative tightening in the coming months, though it is very unlikely that any decisions will be reached or announced at this stage.

- For the full preview see:FedPrevJan2024.pdf

MNI BOE Preview - February 2024: The end of the tightening bias?

The February MPC meeting will almost certainly see Bank Rate left on hold at 5.25% but there are three significant aspects of the decision that will be closely watched by markets – the vote split, the guidance and the forecasts.

- The Bank continues to reiterate that it is data dependent, and the story in the data has changed since both the November MPR forecasts were made and also since the December MPC meeting.

- On the vote: We still look for 1-2 hawkish dissenters and assign a 40% probability to Dhingra voting for a cut at this meeting.

- We expect the tightening bias to be removed from the Monetary Policy Statement, while “finely balanced” is likely to be erased from the Minutes. But the rest of the guidance is likely to stay intact.

- We have read through and summarised over 20 analyst previews. There is a huge split of opinion on what could happen to both the vote, guidance and the forecasts at this meeting.

- For the full preview see:MNI BoE Preview - Feb24.pdf

MNI Sees Small Upside Risks To German National CPI Following State Data

We have now received state data that equates to 86.7% weighting of the national January flash German CPI print (due at 13:00 BST / 14:00 CET). MNI estimates that national CPI (non-HICP print) rose by +0.1-0.2% m/m and 2.9% y/y.

- This is based on the published index values for available state data. The data implies readings slightly below consensus on an annual basis (with the Bloomberg consensus coming into the session at +3.0% Y/Y). However, the M/M reading appears to have upside risks to the Bloomberg consensus of +0.1% M/M.

- How can we look for a softer Y/Y print but a firmer M/M print? Looking more into the Bloomberg survey data there are 16 analysts who forecast both M/M and Y/Y and a further 7 analysts who forecast only Y/Y. If we take only the analysts who forecast both, the median of their forecasts is 2.85%Y/Y (mean 2.89%) with median 0.1%M/M (0.14%M/M mean). So our 2.90%Y/Y and +0.18%M/M calculations see small upside risks to both the M/M and Y/Y prints from this sub-section of the survey.

- Today's state data points to core CPI (ex-energy and food) of roughly 3.3-3.4% Y/Y, vs 3.5% in January. Core CPI data is only available for 6 states accounting for 50% of the national index so this is a rough estimate, but the direction vs December's reading seems downward.

- Note: These estimates are in relation to the national CPI print, not the HICP print which feeds into the Eurozone HICP print that the ECB targets. The magnitude of surprises to consensus can sometimes be different due to the different methodologies and weights used in national CPI vs HICP - but the direction of the surprise is normally the same.

| Y/Y | January (Reported) | December (Reported) | Difference |

| North Rhine Westphalia | 3.0 | 3.5 | -0.5 |

| Hesse | 2.2 | 3.5 | -1.3 |

| Bavaria | 2.9 | 3.4 | -0.5 |

| Brandenburg | 3.7 | 4.5 | -0.8 |

| Baden Wuert. | 3.2 | 3.8 | -0.6 |

| Berlin | 2.3 | 3.9 | -1.6 |

| Bremen | N/A | 2.1 | N/A |

| Saxony | 3.5 | 4.3 | -0.8 |

| Rhineland-Palatinate | 2.7 | 3.5 | -0.8 |

| Lower Saxony | 2.3 | 3.7 | -1.4 |

| Mecklenburg Western Pomerania | N/A | 4.2 | N/A |

| Saxony-Anhalt | N/A | 3.5 | N/A |

| Saarland | 2.9 | 4.1 | -1.2 |

| Thuringia | N/A | 4.4 | N/A |

| Weighted average: | 2.90% | for | 86.7% |

| M/M | January (Reported) | December (Reported) | Difference |

| North Rhine Westphalia | 0.3 | -0.1 | 0.4 |

| Hesse | 0.0 | 0.0 | 0.0 |

| Bavaria | 0.2 | 0.1 | 0.1 |

| Brandenburg | 0.1 | 0.0 | 0.1 |

| Baden Wuert. | 0.2 | 0.1 | 0.1 |

| Berlin | -0.2 | 0.2 | -0.4 |

| Bremen | N/A | 0.1 | N/A |

| Saxony | 0.4 | 0.2 | 0.2 |

| Rhineland-Palatinate | 0.3 | 0.1 | 0.2 |

| Lower Saxony | 0.0 | 0.1 | -0.1 |

| Mecklenburg Western Pomerania | N/A | 0.2 | N/A |

| Saxony-Anhalt | N/A | -0.1 | N/A |

| Saarland | 0.5 | 0.1 | 0.4 |

| Thuringia | N/A | 0.2 | N/A |

| Weighted average: | 0.18% | for | 86.7% |

Details Of German State Level Prints Suggest Services Inflation Stickiness

Looking at individual drivers of German January CPI inflation based on the state-level data already published, we note the following observations in addition to our headline/core forecast already released (a reminder that we estimate national CPI (non-HICP print) at +0.1-0.2% m/m and 2.9% y/y):

- On an annual basis, services CPI appears to be sticky, again tracking at over 3% Y/Y (vs 3.2% in December) for the six states that reported services inflation in the flash release (around 50% of the national CPI basket). This is in part due to the aformentioned rise in restuaurant VAT from January - we see the restaurants and hotels component rising around +2.0% M/M (NSA).

- The energy component is seen reversing its Y/Y rise in December (which was driven by base effects relating to energy subsidies in December '22), with current tracking (again based on 50% of the basket) around -3.3% Y/Y. We note that energy sub-components appear to have increased on an NSA monthly basis, due to various policy changes noted in our preview.

- Goods inflation (incl. energy) appears to have decelerated on an annual basis, to around 2.3% Y/Y (based on 67% of the national CPI basket) from 4.1% in December.

- Food, alcohol and tobacco inflation is indicated to continue its gradual moderation on an annual basis.

US TSYS: Refunding And ECI Provide Early Focal Point Before FOMC Headlines

Cash Tsys have seen a sizeable pulling back from overnight highs, with the move lower aided by European data with German regional inflation pointing to small upside surprise for the national print later on and surprisingly strong Italian labor data.

- Currently trading 0-1bp richer, they consolidate a large paring of yesterday’s JOLTS-inspired losses, with the reversal boosted by equity futures sliding after weak earnings for big-tech names after the close.

- TYH4 at 111-26 is off an earlier high of 112-02 on solid volumes of 375k. The contract continues what’s deemed a corrective cycle as part of a bearish trend, although the extent of the lift suggests scope for an extension in the near-term. The day's high aside, next resistance is now seen at 112-26+ (Jan 12 high).

- Ahead, ADP offers some volatility prospects before early focus on the Treasury’s QRA landing alongside the employment cost index for Q4. That's followed by an interlude for the MNI Chicago PMI after mixed alternate manufacturing indicators, before the day’s main event in the FOMC announcement and press conference.

- Fed: FOMC decision (1400ET), Chair Powell’s presser (1430ET)

- Treasury Quarterly Refunding Announcement (0830ET)

- Data: MBA mortgage data Jan 26 (0700ET), ADP employment Jan (0815ET), ECI Q4 (0830ET), MNI Chicago PMI Jan (0945ET)

- Bill issuance: US Tsy to sell $60B 17-week bills (1130ET)

US TSY FUTURES: OI Points To Mix Of Modest Positioning Swings On Tuesday

The combination of yesterday's twist flattening of the Tsy futures curve (come settlement time) and preliminary OI data points to the following net positioning swings across the curve on Tuesday.

- Net long cover: TU & FV futures

- Net long setting: TY & UXY futures

- Net short cover: US & WN futures

- DV01 equivalent OI swings in each contract were contained, with a bias towards a mix of short and long cover in net curve terms.

| 30-Jan-24 | 29-Jan-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 3,921,624 | 3,943,178 | -21,554 | -805,598 |

| FV | 5,932,109 | 5,943,189 | -11,080 | -474,145 |

| TY | 4,721,861 | 4,720,623 | +1,238 | +79,502 |

| UXY | 2,105,794 | 2,097,400 | +8,394 | +770,604 |

| US | 1,422,864 | 1,429,081 | -6,217 | -847,500 |

| WN | 1,646,623 | 1,652,422 | -5,799 | -1,243,128 |

| Total | -35,018 | -2,520,264 |

STIR: Further Labor Data To Add To The Mix Before FOMC Decision

Fed Funds implied rates for the March FOMC are nearly back at pre-JOLTS/Conf Board levels whilst they’ve unwound about half of the increase for late 2024 meetings.

- It leaves a cumulative 11.5bp of cuts for March, just about three cuts for July with 76bp and 133bp for 2024.

- A large part of the move came in the second half of yesterday’s session, naturally paring the sell-off (perhaps on some weaker details within JOLTS including further quits rate moderation) before an added hand from big-tech earnings weakness after the close.

- Today of course sees the FOMC decision (MNI preview) but first lands ADP and then more importantly the ECI - of added note considering the reaction to JOLTS yesterday - along with Treasury refunding amounts.

STIR: OI Points To Mix Of SOFR Positioning Swings On Tuesday

The combination of Tuesday’s twist flattening on the SOFR strip and preliminary OI data point to the following net positioning swings:

- Whites: Net short setting was seemingly seen across all contracts.

- Reds: Net short setting was seemingly seen across all contracts.

- Greens: Net short setting was seemingly seen in SFRZ5 & H6, while long cover was seemingly seen in SFRM6,. It is hard to be certain when it comes to SFRU6 given its unchanged price status on the day. We also note that the net OI swing was fairly modest in SFRU6.

- Blues: Net long setting was seemingly seen through most of the contracts, with some modest net short cover in in SFRU7 providing the only exception.

| 30-Jan-24 | 29-Jan-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRZ3 | 1,204,438 | 1,200,462 | +3,976 | Whites | +27,006 |

| SFRH4 | 1,256,423 | 1,236,674 | +19,749 | Reds | +80,884 |

| SFRM4 | 1,140,438 | 1,138,553 | +1,885 | Greens | +16,880 |

| SFRU4 | 984,205 | 982,809 | +1,396 | Blues | +16,399 |

| SFRZ4 | 1,074,255 | 1,038,242 | +36,013 | ||

| SFRH5 | 543,910 | 541,886 | +2,024 | ||

| SFRM5 | 671,932 | 646,614 | +25,318 | ||

| SFRU5 | 591,630 | 574,101 | +17,529 | ||

| SFRZ5 | 640,409 | 624,882 | +15,527 | ||

| SFRH6 | 419,019 | 415,472 | +3,547 | ||

| SFRM6 | 417,185 | 418,710 | -1,525 | ||

| SFRU6 | 299,163 | 299,832 | -669 | ||

| SFRZ6 | 268,608 | 266,538 | +2,070 | ||

| SFRH7 | 138,139 | 133,280 | +4,859 | ||

| SFRM7 | 158,543 | 148,692 | +9,851 | ||

| SFRU7 | 148,396 | 148,777 | -381 |

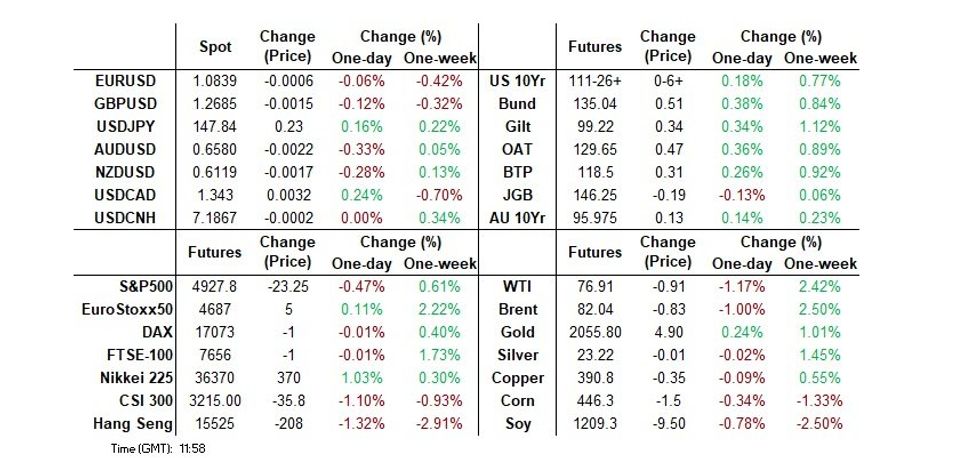

FOREX: Weak USD Selling Signal Going Into Month End

- Despite seeing a small push lower following a French inflation miss, coming below consensus, the EURUSD has not quite managed to break the 1.0800 handle, only printing a 1.0806 low, and short of the support still eyed at 1.0793.

- The Dollar was and is still on the front foot during the European early session, and that is despite the US 10yr Yield falling and testing the 4% mark.

- Some pullback off the high in Equities, may have been somewhat supportive, but looking at the last 5 days, the Dollar is mixed, with CAD up 0.74% and EUR down 0.55% for that period.

- AUD was the overnight and early worst performer, after the Australian inflation came below consensus, but has been taken over by the NOK, as Oil (WTI) slips lower this morning.

- Note that most desks only sees weak USD sell signal going into Month End.

- Looking ahead, main focus will be on the Fed decision (expected unchanged rate), but we'll be getting US ADP, MNI Chicago PMI, and US Treasury Quarterly refunding before that event.

FX OPTIONS: Expiries for Jan31 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0800 (783mln), 1.0845 (298mln), 1.0850 (336mln), 1.0860 (830mln), 1.0875 (281mln), 1.0880 (280mln), 1.0900 (784mln).

- USDJPY: 147.25 (1.09bn), 147.50 (325mln), 148.00 (568mln).

- GBPUSD: 1.2630 (800mln), 1.2700 (471mln).

- USDCAD: 1.3400 (1.09bn), 1.3455 (339mln), 1.3500 (418mln).

- AUDUSD: 0.6590 (626mln), 0.6600 (978mln), 0.6605 (289mln).

- USDCNY: 7.1400 (455mln).

EUROPEAN ISSUANCE UPDATE

2.20% Feb-34 Bund Auction

- E4.5bln (E3.606bln allotted) of the 2.20% Feb-34 Bund.

- Avg yield 2.23% (bid-to-cover 1.41x).

15-year BTP Syndication: Launched

- E10bln of the new Oct-39 15-year BTP (ISIN: IT0005582421).

- Books closed in excess of E77bln (inc E2.275bln JLM interest).

- Spread set at 3.25% Mar-38 BTP + 11 bps (guidance was + 13 bps area)

EFSF Mandate

- "Today, EFSF, the European Financial Stability Facility has sent a Request for Proposal to a selection of banks from the EFSF/ESM Market Group with regards to an upcoming transaction, subject to market conditions."

- Note MNI had pencilled in an ESM syndication for next week - and this transaction will take place instead.

- We don't have a strong view on the maturity on offer.

BONDS: Off Best Levels As Early Impulse Fades, Plenty Of Risk Events Ahead

Initial European trade saw core global FI markets benefit from a combination of the late NY Tsy rally, downticks in U.S. & Chinese equity indices (the former post-big tech earnings and the latter on well-defined areas of economy worry/lack of fresh policy support), source reports flagging less room for UK fiscal easing and softer-than-expected French & Australian CPI prints.

- Initial regional German CPI data helped bias the space away from best levels (with a particularly focus on the relatively firm print from the lowly-weighted Saxony), before the totality of the data/run rate for the national release (~2.9% Y/Y) limited the pullback.

- Still, there hasn’t been a meaningful bid in the time since, with continued supply burden (the EFSF became the latest to frontload their syndication schedule, along with the presence of Italian & German supply) and firmer than-expected Italian wage data (which was driven by a one-off government subsidy) resulting in some light pressure in recent trade.

- The failure of bond bulls to hold/develop a shallow breach of 4.00% in U.S. 10s also aided the pullback.

- Bund futures trade ~45 ticks shy of highs but are still ~55 ticks better off. Cash trade sees German benchmark yields printing 0.5-5.0bp lower on the day, with a bull flattening impulse.

- Peripherals are little changed to 2bp wider vs. 10-Year Bunds, with the presence of the Italian 15-Year BTP syndication (today’s business) providing the focal point on that front.

- Gilt futures are 0 ticks higher on the day, a little over 35 ticks off best levels. Cash gilt yields are 1.0-2.5bp lower, with a light flattening bias seen.

- Looking ahead, most of the focus will fall on U.S. matters, with the FOMC, QRA, ADP labour market data, MNI Chicago PMI and employment cost index all due. The aforementioned national German CPI print and supply headlines the European docket.

EQUITES: Price Signal Summary - Uptrend In S&P E-Minis Remains Intact

The uptrend in S&P E-Minis remains intact and this week’s fresh cycle highs, reinforce current conditions. Resistance at 4841.50, the Dec 28 high, has recently been cleared, confirming an extension of the price sequence of higher highs and higher lows. Sights are on 4982.62 next, the 1.50 projection of Nov 10 - Dec 1 - 7 price swing. Initial support is at 4854.34, the 20- day EMA.

- EUROSTOXX 50 futures remain firm and the contract is holding on to its recent gains. Key resistance at 4634.00, the Dec 14 high, has recently been cleared. The break confirms a resumption of the medium-term uptrend and sights are on the 4700.00 handle next. Initial firm support lies at 4549.60, the 20-day EMA.

COMMODITIES: Bull Cycle In Oil Futures Remains In Play

Gold continues to trade above the Jan 17 low of $2001.9. The recent print below the 50-day EMA and the break of support at $2013.4, the Jan 11 low, has strengthened a bearish threat and a resumption of weakness would open a key level at $1973.2, the Dec 13 low. For bulls, clearance of 2062.3, the Jan 12 high, is required to signal a reversal.

- In the oil space, WTI futures continue to trade closer to their recent highs. The contract has breached $76.31, the Dec 26 high. The clear break of this hurdle undermines the recent bearish theme and highlights a stronger short-term bullish condition. A continuation higher would signal scope for a climb towards $79.56, the Nov 30 high. On the downside, initial key support lies at $74.76, the 50-day EMA. Monday’s move lower appears - for now - to be a correction.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 31/01/2024 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 31/01/2024 | 1300/1400 | *** |  | DE | HICP (p) |

| 31/01/2024 | 1315/0815 | *** | | US | ADP Employment Report |

| 31/01/2024 | 1330/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 31/01/2024 | 1330/0830 | ** | | US | Employment Cost Index |

| 31/01/2024 | 1330/0830 | ** | | US | Treasury Quarterly Refunding |

| 31/01/2024 | 1445/0945 | *** | | US | MNI Chicago PMI |

| 31/01/2024 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 31/01/2024 | 1900/1400 | *** | | US | FOMC Statement |

| 01/02/2024 | 2200/0900 | ** |  | AU | IHS Markit Manufacturing PMI (f) |

| 01/02/2024 | 0030/1130 | * | | AU | Building Approvals |

| 01/02/2024 | 0030/1130 | ** | | AU | Trade price indexes |

| 01/02/2024 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Manufacturing PMI |

| 01/02/2024 | 0145/0945 | ** |  | CN | IHS Markit Final China Manufacturing PMI |

| 01/02/2024 | 0815/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 01/02/2024 | 0830/0930 | *** |  | SE | Riksbank Interest Rate Decison |

| 01/02/2024 | 0845/0945 | ** |  | IT | S&P Global Manufacturing PMI (f) |

| 01/02/2024 | 0850/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 01/02/2024 | 0855/0955 | ** | | DE | IHS Markit Manufacturing PMI (f) |

| 01/02/2024 | 0900/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 01/02/2024 | 0930/0930 | ** |  | UK | S&P Global Manufacturing PMI (Final) |

| 01/02/2024 | 1000/1100 | *** | | EU | HICP (p) |

| 01/02/2024 | 1000/1100 | ** | | EU | Unemployment |

| 01/02/2024 | 1000/1100 | *** | | IT | HICP (p) |

| 01/02/2024 | 1130/1230 | | EU | ECB's Lane remarks at EIEF | |

| 01/02/2024 | 1200/1200 | *** | | UK | Bank Of England Interest Rate |

| 01/02/2024 | 1200/1200 | *** | | UK | Bank Of England Interest Rate |

| 01/02/2024 | 1230/1230 | | UK | BoE Press Conference | |

| 01/02/2024 | - | *** | | US | Domestic-Made Vehicle Sales |

| 01/02/2024 | 1330/0830 | *** | | US | Jobless Claims |

| 01/02/2024 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 01/02/2024 | 1330/0830 | ** | | US | Preliminary Non-Farm Productivity |

| 01/02/2024 | 1400/1400 | | UK | DMP Data | |

| 01/02/2024 | 1445/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/02/2024 | 1500/1000 | *** | | US | ISM Manufacturing Index |

| 01/02/2024 | 1500/1000 | * | | US | Construction Spending |

| 01/02/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 01/02/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 01/02/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 01/02/2024 | 1630/1130 | | CA | BOC Governor Macklem testifies at House finance committee. |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.