Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Inflation still top of mind, with PPI data eyed as well as more Fedspeak

- Equity decline persists, a number of Asian markets enter correction

- Commodities roll off cycle highs, Chinese Iron Ore off as much as 12% overnight

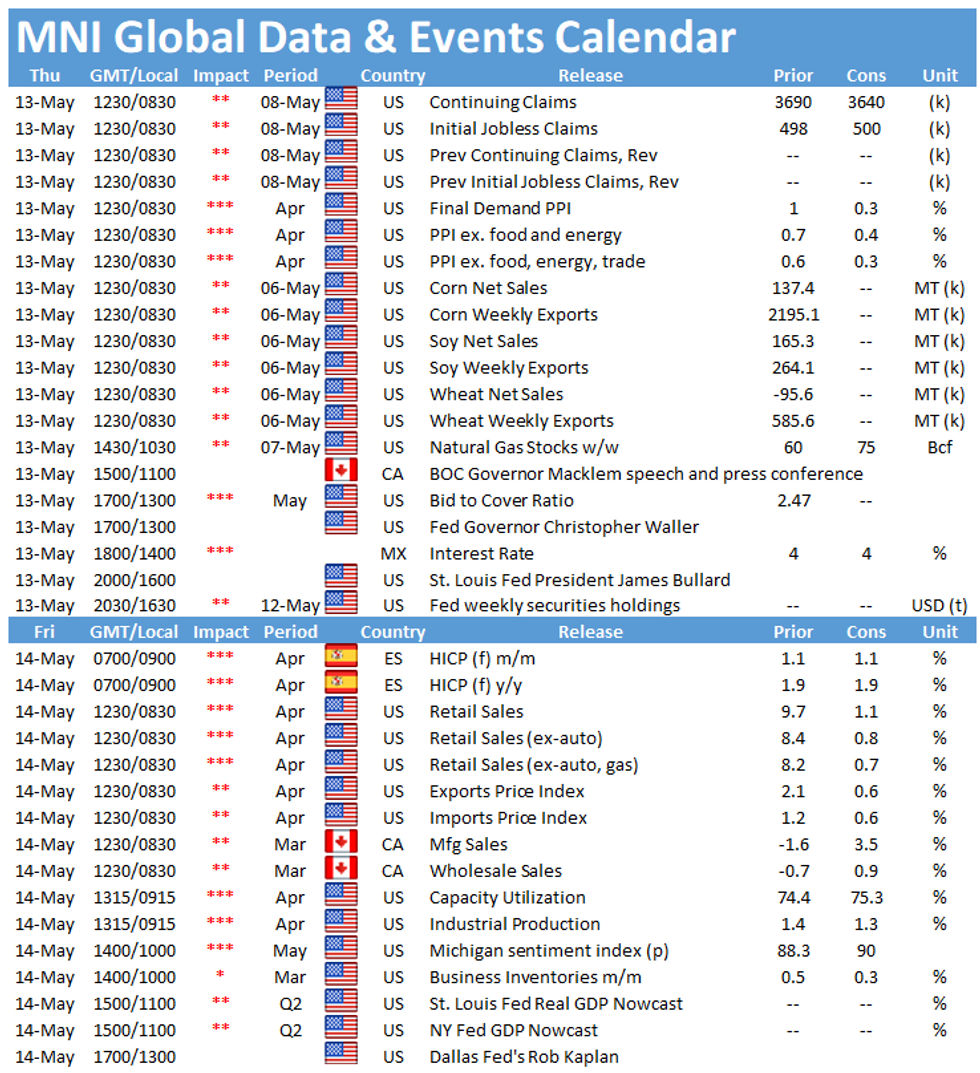

US TSYS SUMMARY: PPI Eyed As Follow-Up From CPI Shock

Tsy losses have slowed in overnight post-CPI trade Thursday, but respite looks to have been fleeting. Jun TYs have stabilized but briefly pierced through Wednesday's low (131-28) in European trade: last down 1.5/32 at 131-28 (L: 131-27 / H: 132-03). Elevated volumes (~385k).

- Attention is on PPI/jobless claims data and 30-Yr supply later.

- A bit of curve flattening in Asia-Pac trade has since reversed: the 2-Yr yield is unchanged at 0.1629%, 5-Yr is up 0.3bps at 0.866%, 10-Yr is up 1bps at 1.7018%, and 30-Yr is up 0.4bps at 2.4153%.

- Attention firmly on data (PPI and jobless claims) at 0830ET. It doesn't appear there was any revision in PPI estimates for Apr (+0.3% M/M headline; +0.4% ex-food and energy) in the wake of Wednesday's upside CPI surprise.

- Another decent Fed speaker slate today, where opinions on inflation will be in demand: Richmond Fed's Barkin at 1000ET; Gov Waller at 1300ET; St Louis' Bullard at 1600ET.

- In supply, we get $80B in 4-/8-week bill auctions at 1130ET, and $27B 30-Yr Tsy bond at 1300ET. Of potential note is the NY Fed's forward purchase schedule update at 1500ET, where we could see a potential tweak of buying allocations.

EGB/GILT SUMMARY: Inflation Concerns Continue To Bite

Equities and sovereign bonds are under pressure again from lingering inflation concerns, further fueled by yesterday's stronger than expected US CPI print.

- Gilt yields are 1-3bp and the curve is 2bp steeper.

- The bund curve has similarly bear steepened with the 2s30s spread 2bp wider on the day.

- OAT yields have pushed up 1-3bp.

- BTPs have underperformed core EGBs with yields 3-6bp higher and the curve 2bp steeper.

- Supply this morning came from Italy (BTPs, EUR9.25bn) and Ireland (IGBs, EUR1.5bn).

EUROPE ISSUANCE UPDATE: Ireland, Italy Auctions

Ireland sells 10/12/30y IGBs:

- E0.800bln 0% Oct-31 IGB, Avg yield 0.30% (Prev. 0.01%), Bid-to-cover 1.48x, (Prev 1.83x)

- E0.400bln 1.30% May-33 IGB, Avg yield 0.40%, (Prev. 0.50%), Bid-to-cover 1.50x

- E0.300bln 1.50% May-50 IGB, Avg yield 1.03% (Prev 0.67%), Bid-to-cover 1.68x (Prev 1.58x)

Italy sells 3/7/30y BTPs

- E3.000bln 0% Apr-24 BTP, Avg yield -0.06% (Prev. -0.17%), Bid-to-cover 1.41x (Prev. 1.38x)

- E4.500bln 0.50% Jul-28 BTP, Avg yield 0.69% (Prev. 0.36%), Bid-to-cover 1.35x

- E1.750bln 1.70% Sep-51 BTP, Avg yield 2.06% (Prev. 1.47%), Bid-to-cover 1.30x (Prev 1.37x)

EUROPE OPTION FLOW SUMMARY: Sizeable Activity in Bund Options

Significant activity in Bund options Thursday, with profit-taking and new positions added targeting 0% in the 10yr German yield.

Eurozone:

RXM1 170.5/169.5/168.5p fly 1x1x0.75, sold at 63 and 63.5 in 4k (profit taking)

RXM1 169/168.5ps, sold at 18 in 5k (profit taking)

RXM1 169/168ps, sold at 31 in 5k (profit taking)

RXM1 168/167ps 1x1.5, bought for 10.5/11 in 7.5k

RXM1 170.5/169.5ps, sold at 82.5 in 30k vs 6.6k bund at 168.92 (unwind)

RXN1 170/168.5ps 1x1.5, bought for 28 in 3k (underlying Sep Bund is 170.48), Playing ECB and target ~0% in yield

RXN1 169/168/167/166p condor, bought for 17.5 in 16.75k

3RU1 100.12/99.87ps, bought for 7.25 in 5k (ref 99.09)

UK:

2LM1 99.62/99.50/99.37p fly sold at 4.5 in 10k

FOREX: AUD/JPY Approaching Long-Held Support

- Risk-off is pervading through currency markets given the persistent weakness in global stocks since yesterday's US CPI print. AUD is among the weakest in G10, extending the sell-off from the Monday high of $0.7891 to briefly show below the $0.77 mark today. This opens declines toward the May 4 low of $0.7675, which would trigger further bearish signals.

- The main beneficiaries Thursday have been the JPY and USD, which sit firmer against most others in DMFX. AUD/JPY is on track to have declined in every session so far this week, and is narrowing the gap with key support at the 84.09 50-dma, a level that's largely held for months.

- Recent weakness in EUR/USD has put the pair at new weekly lows, opening 1.1986 as next key downside level.

- Focus turns to US PPI data due later today, with markets cognizant of the risk of a sizeable upside surprise after the eventful CPI reading out yesterday. Consensus looks for a modest slowdown in PPI later today, to +0.3% for the headline M/M and to +0.4% for ex-food and energy figures.

- Weekly US jobless claims data also cross, as well as speeches from BoE's Cunliffe & Bailey, Fed's Barkin, Waller & Bullard, BoC's Macklem and the Banxico rate decision.

FX OPTIONS: Expiries for May13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1900-05(E1.4bln), $1.1950-55(E2.2bln-EUR puts), $1.1964-75(E2.0bln-EUR puts), $1.1995-00(E535mln), $1.2040-50(E538mln), $1.2100(E1.3bln-EUR puts), $1.2115-30(E850mln), $1.2150(E821mln), $1.2170-80(E2.5bln-EUR puts)

- USD/JPY: Y108.30-40($678mln), Y108.90-109.00($1.6bln-USD puts), Y109.15-20($505mln), Y110.40-50($648mln)

- USD/CHF: Chf0.9085-95($1.3bln-USD puts)

- AUD/USD: $0.7690-00(A$656mln), $0.7760-65(A$1.0bln), $0.7780-95(A$1.7bln)

- USD/CAD: C$1.2090-10($503mln)

EQUITIES: Stock Sell-Off Exposing Key Supports, But No Correction Yet

- Globally, equities remain weak, with losses led by Asian indices. The Nikkei 225 finished lower by over 2.5%, with Taiwan also a particular weak spot (the Taiex sits over 10% off its 2021 high). Europe is following suit, with most indices off 1.5% or so. UK markets underperform thanks to a sizeable pullback in the materials sector, with the likes of Anglo American and Rio Tinto off sharply after China's pledge to rein in surging commodities prices.

- The pullback in the e-mini S&P is extending early Thursday, taking out nearby support and edging below the 50-dma at 4052.82. A close below would be the first since early March.

- Today's weakness has extended the pullback from the alltime high to near 5%, so the index is far from entering correction territory just yet, but markets remain wary of the risk.

- The longevity of the recent sell-off will depend on the ability for the index to hold above key support at 3994.14. A break below here opens a decline toward 3843.25, which would be well on the way to a technical correction.

COMMODITIES: WTI, Brent Offered as Colonial Pipeline Back Online

- Prices were supported throughout the first half of the week on a supply scramble in the southern US states after a weekend cyber attack knocked the Colonial Pipeline offline. While reserves are unlikely to hit the gas pumps immediately, the issues are expected to be resolved in short order, taking some of the pressure off prices this morning.

- WTI futures are back below the $65/bbl mark, and Brent has eased well below $68/bbl.

- In metals space, precious benchmarks are lower, with gold and silver off 0.3% and 0.8% respectively. This cements the importance of the 200-dma in gold as key resistance, with the level crossing at $1847.9.

- Industrial commodities are also suffering, with China-listed Iron Ore futures falling sharply after the Chinese authorities pledged to rein in flyaway commodities prices.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.