Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

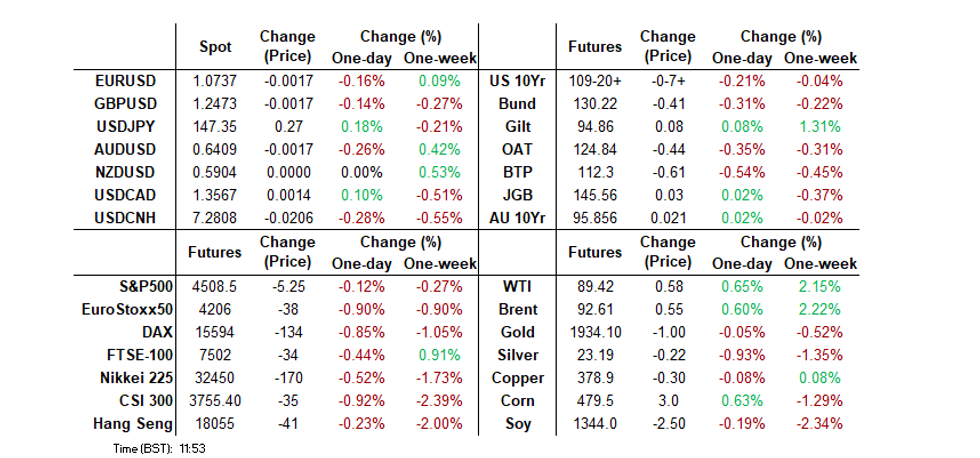

- EGBs cheapen on hawkish ECB sources piece from RTRS.

- Gilts outperform on UK GDP, GBP pares initial losses.

- U.S. CPI headlines in NY hours.

MNI US CPI Preview: Airfares And Seasonal Factors Seen Leading Modest Core Bounce

EXECUTIVE SUMMARY

- Released on Wednesday at 0830ET, consensus puts core CPI inflation at 0.2% M/M in August in what’s likely only a minor uptick from unrounded 0.16% M/M readings in both June and July.

- The main increase is seen coming from airfares after two particularly heavy declines, muddying implications for core PCE seeing as it leans on PPI airfares (to be released Thursday).

- The Fed’s closely watched core services ex housing measures should firm further, which despite the above could still catch headlines.

- The market sees very low odds of a hike next week and roughly 50/50 probability of a hike by year-end, from a combination of data and cautiously optimistic Fedspeak. Cut expectations meanwhile are near recent lows, approaching 100bps from the terminal to end-2024 and more closely aligned with the June dot plot.

- Both PPI and retail sales land the day after on Thursday, before the Sept 19-20 FOMC meeting.

- PLEASE FIND THE FULL REPORT HERE: USCPIPrevSep2023.pdf

US TSYS: A Little Cheaper & Steeper Into CPI

TYZ3 tests initial support (109-19) with spill over from EGBS evident, as the latter trades on the defensive in the wake of last night’s hawkish ECB sources piece from RTRS.

- The contract operates at the base of a narrow 0-06 range, while cash Tsys sit 1-3bp cheaper, steepening.

- Another ’23 high in crude oil futures will have aided the cheapening.

- See the previous bullet for more details on Fed-related STIR pricing, with the picture little changed ahead of the impending CPI release (our full preview of that key risk event here).

- 30-Year Tsy supply and the real AWE data that accompanies the CPI release pad out the NY docket.

- Headline flow thus far has centred on the aforementioned ECB sources report, Sino-U.S. and Sino-EU trade relations & continued speculation surrounding Chinese policy support measures.

STIR: Fed Path Sees Less Than 100bp of Cuts In 2024 Ahead Of US CPI

- Fed Funds implied rates are little changed after limited spillover from a hawkish ECB sources piece from Reuters late yesterday. It consolidates yesterday’s main change being a further trimming of 2024 cuts ahead of today’s US CPI print.

- Cumulative hikes from 5.33% effective: +1.5bp Sep, +11bp Nov, +12bp Dec to terminal 5.45%.

- Cuts from terminal: 32bp to Jun’24 and 96bp to Dec’24. The SFRU3/Z4 spread shows a similar reading, for its least inverted since mid-March in the initial regional banking fallout otherwise at levels last seen in Nov 2022.

STIR: OI Points To Mixed Positioning Swings In SOFR on Tuesday

The combination of yesterday’s price action and preliminary OI data point to the following net positioning swings on the SOFR strip:

- Short cover was seemingly seen in SFRM3-Z3, while SFRH4 seemingly saw fresh shorts added. The former dominated the latter when it came to net impact.

- The reds seemed to see a mix of fresh shorts added and long cover, with the former dominating.

- Net OI in the greens was essentially unchanged, with any short setting being offset by long cover.

- The blues saw a mix of positioning swings, with the unchanged nature of SFRU6 in price terms muddying any inference re: net positioning swings in that pack.

| 12-Sep-23 | 11-Sep-23 | Daily OI Change | Daily OI Change In Packs | ||

| SFRM3 | 1,113,816 | 1,120,406 | -6,590 | Whites | -9,407 |

| SFRU3 | 1,142,697 | 1,142,835 | -138 | Reds | +24,528 |

| SFRZ3 | 1,273,497 | 1,285,628 | -12,131 | Greens | -67 |

| SFRH4 | 976,807 | 967,355 | +9,452 | Blues | +2,677 |

| SFRM4 | 901,706 | 898,197 | +3,509 | ||

| SFRU4 | 820,283 | 808,284 | +11,999 | ||

| SFRZ4 | 882,271 | 871,963 | +10,308 | ||

| SFRH5 | 524,957 | 526,245 | -1,288 | ||

| SFRM5 | 577,344 | 578,361 | -1,017 | ||

| SFRU5 | 486,029 | 485,977 | +52 | ||

| SFRZ5 | 426,462 | 426,893 | -431 | ||

| SFRH6 | 290,806 | 289,477 | +1,329 | ||

| SFRM6 | 246,904 | 245,882 | +1,022 | ||

| SFRU6 | 167,116 | 163,900 | +3,216 | ||

| SFRZ6 | 171,408 | 173,003 | -1,595 | ||

| SFRH7 | 126,323 | 126,289 | +34 |

ECB: MNI ECB Preview - September 2023: A Hawkish Hold

- Conflicting data, limited insight from policymakers since the last meeting, and the very marginal nature of hiking by 25bp or holding following 425bp in policy hikes this cycle, make the September ECB rate decision a tough call.

- We assume that the ECB will leave policy rates unchanged at this meeting, while maintaining a tightening bias and stressing that rates could head higher at future meeting. However, this is a relatively low conviction call.

- For the full publication please see:ECB Preview September 2023 .pdf

EGBS: Under Pressure, ECB Sources Dominate

A fresh wave of selling knocks Bunds through previous session lows, before a recovery from worst levels. Bears continue to breach intermediate support levels, a continuation would expose 129.72, the Aug 15 low and a key support.

- Benchmark German cash benchmarks run 2-5bp cheaper, with a light flattening bias.

- Yesterday’s hawkish ECB sources piece from RTRS continues to reverberate, with related OIS pricing titled higher, albeit off hawkish extremes (around 17bp of tightening is now showing for tomorrow).

- Initial glances at the Eurozone IP data suggest that Irish data may have skewed the release once again.

- Core/semi-core spreads little changed to a touch wider vs. Bunds.

- Most peripherals widen by 1-3bp vs. Bunds given the ECB repricing/presence of supply.

- Greece provides the exception, narrowing at the margin after yesterday’s widening (some sell-side names remain constructive on GGBs ahead of Moody’s scheduled sovereign rating review of Greece on Friday).

- A quick reminder that our policy team has flagged its understanding that “the ECB is only likely to begin in-depth discussions over its balance sheet reduction after the conclusion of its operational framework review due by the end of the year.”

- Also note that the ECB has suggested that the Italian banking tax may create problems re: legal uncertainty, as well as pose headwinds re: bank funding.

EUROPEAN ISSUANCE UPDATE

German auction results

- The 30-year Bund auction was decent with the lowest accepted price further above the pre-auction mid-price than at the previous auction for both the 0% Aug-52 Bund and the 1.80% Aug-53 Bund.

- The bid-to-offers were also respectable without being exceptional.

- E1bln (E810mln allotted) of the 0% Aug-52 Bund. Avg yield 2.73% (bid-to-cover 1.77x).

- E1.5bln (E1.209bln allotted) of the 1.80% Aug-53 Bund. Avg yield 2.79% (bid-to-cover 1.88x).

Italy auction results

- A decent Italian 3/7/17/30-year BTP auction with bid-to-covers exceeding the previous auctions for the three reopenings and the new 7-year BTP seeing the same bid-to-cover of around 1.4x at its launch today (despite the last auction being for a smaller size).

- The average auction price also exceeded the pre-auction mid-price for all issues.

- E3.25bln of the 3.85% Sep-26 BTP. Avg yield 3.86% (bid-to-cover 1.51x).

- E4bln of the 4.00% Nov-30 BTP. Avg yield 4.21% (bid-to-cover 1.41x).

- E1bln of the 5.00% Sep-40 BTP. Avg yield 4.74% (bid-to-cover 1.68x).

- E1.5bln of the 4.50% Oct-53 BTP. Avg yield 4.89% (bid-to-cover 1.63x).

Portugal auction results

- IGCP issues marginally above the top of the target range with E1.007bln sold (E0.75-1.00bln target).

- Decent bid-to-covers for both issues sold today, in excess of 2.5x.

- The allotment price was also high: for the 0.90% Oct-35 OT the allotment price of 73.67 was in excess of today's intraday high on the secondary market of 73.44. For the the 1.65% Jul-32 OT, the allotment price was higher than anything traded in the secondary market up to 45 minutes before the auction close.

- E485mln of the 1.65% Jul-32 OT. Avg yield 3.383% (bid-to-cover 2.51x).

- E522mln of the 0.90% Oct-35 OT. Avg yield 3.632% (bid-to-cover 2.96x).

Gilt auction result

- A generally disappointing 10-year gilt auction for the on-the-run 3.25% Jan-33 Gilt with a tail of 1.2bp the widest at a 10-year auction since 1 December 2021.

- The LAP of 91.133 was lower than at any time through the bidding window (around 8:30BST was the last time we saw a price that low).

- On publication of the results the price of the 3.25% Jan-33 Gilt fell from 91.219 almost immediately to 91.137 and has hit a post-auction low of 91.077.

- Gilt futures fell from 95.00 to 94.84 and have hit a post-auction low of 94.77 before recovering back to 94.84 shortly after.

- GBP3.75bln of the 3.25% Jan-33 Gilt. Avg yield 4.402% (bid-to-cover 2.38x, tail 1.2bp).

FOREX: Cable recovers from the lows, US CPI in focus

- It is a positive European morning session for the Dollar, in the Green against all G10s, after Equities fell and US Yield rose, mostly led by Europe, following report that the ECB said that they expect the EU inflation to remain elevated next year.

- The early mover on the open, was the Pound, after UK GDP miss consensus, and Cable fell towards the highlighted level at 1.2446, the September low and lowest level since the start of June.

- Despite printing a 1.2442 low, that area has held and Cable is now circa 20 pips of the low, at the time of typing.

- Looking across G10, the Pound is still mixed, leading gains against the SEK, up 0.23%, and now just down 0.14% vs the Dollar.

- EURUSD stays in that 6 sessions range of 1.0686/1.0769, as market participants await the ECB Tomorrow.

- Given the lack of risk events and data, large options expiry may have played a role in keeping the pair within ranges.

- Initial resistance will be at that top range.

- There's 3.39bn at 1.0730/1.0775 for today's option expiry in EURUSD.

- Looking ahead, main focus is on US CPI and Earnings.

FX OPTIONS: Expiries for Sep13 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0730 (758mln), 1.0755 (1.37bn), 1.0765 (789mln), 1.0775 (469mln). 1.0825 (600mln)

- USDJPY: 147.00 (800mln), 147.50 (1.2bn), 148.00 (695mln)

- USDCAD: 1.3540 (250mln), 1.3550 (254mln)

- AUDUSD: 0.6400 (620mln).

EQUITIES: Bear Threat in EUROSTOXX 50 Futures Remains Present

- For now, gains in the E-mini S&P contract are considered corrective and a bear cycle remains in play. Key resistance is at 4597.50, the Sep 1 high where a break is required to reinstate the recent bullish theme. A stronger sell-off would open key support and bear trigger at 4397.75, the Aug 18 low. Clearance of this support would strengthen a bearish case.

- A bear cycle in EUROSTOXX 50 futures remains in play and the recent recovery is considered corrective. Price has recently pierced 4187.00, the Aug 18 low and a bear trigger. A clear break of this level would strengthen bearish conditions and open 4177.40, 61.8% of the Mar 20 - Jul 31 bull leg. Initial firm resistance is seen at 4278.60, the 20-day EMA.

COMMODITIES: Oil Bulls Remains In The Driver’s Seat

- Gold traded lower yesterday. Key support to watch lies at $1903.9, the Aug 25 low. A break of this level would be viewed as a bearish development and highlight the fact that the recovery between Aug 21 - Sep 1 has been a correction. This would expose $1884.9, the Aug 21 low. On the upside, initial firm resistance is seen at $1929.5, the 50-day EMA. Key resistance is at $1953.0, the Sep 4 high.

- In the oil space, the uptrend in WTI futures remains intact and yesterday's gains reinforce this condition. The break higher confirms a resumption of the uptrend and maintains the bullish price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a rising trend. The focus is on the psychological $90.00 handle. On the downside, initial firm support to watch lies at $83.91, the 20-day EMA.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/09/2023 | 1430/1030 | ** |  | US | DOE Weekly Crude Oil Stocks |

| 13/09/2023 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 13/09/2023 | 1800/1400 | ** | | US | Treasury Budget |

| 14/09/2023 | 0130/1130 | *** |  | AU | Labor Force Survey |

| 14/09/2023 | 0600/0800 | *** |  | SE | Inflation Report |

| 14/09/2023 | 1215/1415 | *** |  | EU | ECB Deposit Rate |

| 14/09/2023 | 1215/1415 | *** | | EU | ECB Main Refi Rate |

| 14/09/2023 | 1215/1415 | *** | | EU | ECB Marginal Lending Rate |

| 14/09/2023 | 1230/0830 | ** | | US | Jobless Claims |

| 14/09/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 14/09/2023 | 1230/0830 | ** |  | CA | Wholesale Trade |

| 14/09/2023 | 1230/0830 | *** | | US | Retail Sales |

| 14/09/2023 | 1230/0830 | *** | | US | PPI |

| 14/09/2023 | 1400/1000 | * | | US | Business Inventories |

| 14/09/2023 | 1415/1615 | | EU | ECB's Lagarde speaks at Podcast | |

| 14/09/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 14/09/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 14/09/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok