Highlights:

- Odds of French right-wing forming majority continue to dwindle

- Greenback remains favoured as US Yields consolidate Monday move

- Powell set to appear at ECB conference alongside Lagarde

- Treasuries outperform EGBs, with the latter seeing some pressure after higher-than-expected Eurozone June core inflation (even if moves were limited with the bear exaggerated by rounding) plus some Italian fiscal factors also likely weighing.

- Today’s session is unusually concentrated around 0930/1000ET with Powell and then JOLTS with the only data offering of the day.

- Cash yields sit between 0-1bp lower on the day, with the belly leading declines.

- TYU4 trades at 109-10 (+04+) as it lifts a little further off yesterday’s low of 109-02+, with solid cumulative volumes for the time of day at 340k.

- Yesterday’s low stopped just short of a key support at 109-00+ (Jun 10 low) with the contract remaining vulnerable. Hawkish developments today meanwhile could see some attention on resistance at 110-00 (20-day EMA).

- Fedspeak: Chair Powell in panel discussion in Sintra (0930ET, just Q&A) - see the STIR bullet for more context.

- Data: JOLTS May (1000ET)

- Bill issuance: US Tsy $65B 41D bill CMB auction (1130ET)

STIR: Fed Rates Mostly In Range Awaiting Powell

- Fed Funds implied rates probe marginally higher for the very near-term but otherwise continue to sit within recent ranges, awaiting Powell’s appearance in Sintra on a panel including ECB’s Lagarde (no prepared text).

- Cumulative cuts from 5.33% effective: 2.5bp Jul, 18bp Sep, 27bp Nov, 45bp Dec and 58bp

- Powell last spoke at the FOMC press conference on Jun 12. From the MNI Fed Review (full report here): “Powell gave little away on rate cut timing as expected, noting that while May’s CPI (+0.16% M/M core versus +0.28% consensus) in addition to April’s figure (+0.29% M/M) represented “progress” that was “building confidence”, “we don't see ourselves as having the confidence that … would warrant beginning to loosen policy at this time." In other words, the theme portrayed by the meeting communications is that rate cuts are being delayed, but they are still expected by year-end, and the ultimate destination hasn’t changed.”

- Since then, other data points have come in softer than expected including consumption metrics and core PCE at just 0.08% M/M in May (but only the first month for 2024 at a sub-2% pace).

- Earlier today, Chicago Fed’s Goolsbee (’25 voter) said policymakers should cut interest rates if US inflation continues to fall back to the 2% target in a BBG TV interview in Sintra. Bloomberg writes he feels “we are on a path to 2%” inflation and “if you just hold the rates where they are while inflation comes down, you are tightening — so you should do that by decision, not by default.”

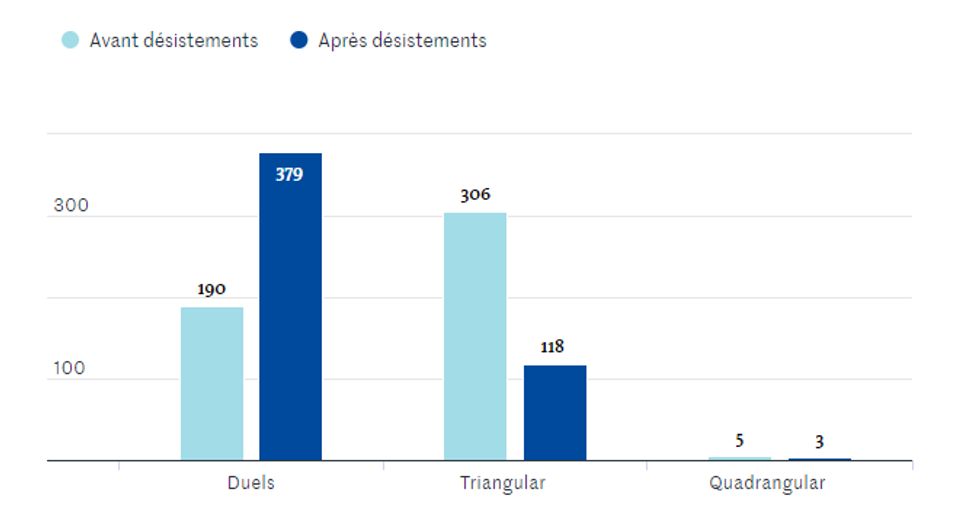

FRANCE: RN Maj. Prospects Declining As Centrist & Leftist Candidates Withdraw

Eligible candidates face a deadline of 1800CET (1200ET, 1700BST) to formally declare whether they intend to run in the 7 July second round legislative elections. This comes as the so-called 'republican front' of centrist and left-wing parties seek to minimise gains for the right-wing nationalist Rassemblement National (National Rally, RN) by reducing the number of tripartite run-offs that could split the vote and allow the RN to win a majority.

- According to Le Monde, as of 0850BST, a total of 191 third/fourth-placed candidates have announced their withdrawal. Of these, 123 are from the left-wing New Popular Front (NFP) alliance, while 66 are from the centrist presidential camp (Ensemble).

- This leaves 118 seats where three parties will still contest the vote, and three where four parties will seek election.

Chart 1. Second Round Contests by Number of Candidates

Source: Le Monde. N.b. 'Avant desistements' - before withdrawals, 'Apres desistements'-after withdrawals. Duels = two-party contests, triangular = three-party contests, quadrangular = four-party contests.

Source: Le Monde. N.b. 'Avant desistements' - before withdrawals, 'Apres desistements'-after withdrawals. Duels = two-party contests, triangular = three-party contests, quadrangular = four-party contests.

- While the NFP and Ensemble are political rivals, the 'republican front' appears to be working at least in part in attempting to concentrate the anti-RN vote. Betting markets see this coming through as well. Data from Polymarket gives the RN a 21% implied probability of winning an overall majority. This is down from a peak of 66%, and indeed stands at a lower chance than had been afforded to the party in the week leading up to the first round.

Chart 2. Implied Probability of RN Winning an Overall Majority, %

Source: Polymarket

Source: Polymarket

- RN parliamentary leader Marine Le Pen appeared to reiterate the stance of party president Jordan Bardella that the RN would only form a majority gov't, saying “It is evident that we cannot accept to go to government if we cannot act,...We wish to govern,”. Le Pen also claimed she would remain president of the RN caucus in the National Assembly no matter the outcome.

STIR: OI Points To Mix Of Short Setting & Long Cover In SOFR Futures On Monday

The combination of preliminary OI data and yesterday’s weakness in SOFR futures reveals a couple of positioning swings that are worth highlighting:

- SFRM4 saw meaningful net long cover of ~30K contracts.

- SFRU4 through SFRZ5 seemed to see net short setting in all contracts.

- Fallout from the first round of the French elections and the potential for a second Presidential term for Donald Trump drove weakness in the long and U.S STIRs, quickly overpowering any bids that came on the back of the ISM manufacturing survey.

- There was little movement in near-term FOMC-dated OIS.

| 01-Jul-24 | 28-Jun-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRM4 | 1,195,684 | 1,226,474 | -30,790 | Whites | -11,989 |

| SFRU4 | 1,147,511 | 1,145,229 | +2,282 | Reds | +19,405 |

| SFRZ4 | 1,002,312 | 998,934 | +3,378 | Greens | -3,167 |

| SFRH5 | 820,929 | 807,788 | +13,141 | Blues | -3,487 |

| SFRM5 | 714,324 | 707,546 | +6,778 | ||

| SFRU5 | 647,804 | 632,010 | +15,794 | ||

| SFRZ5 | 812,460 | 808,019 | +4,441 | ||

| SFRH6 | 553,813 | 561,421 | -7,608 | ||

| SFRM6 | 471,439 | 481,511 | -10,072 | ||

| SFRU6 | 419,612 | 415,971 | +3,641 | ||

| SFRZ6 | 357,794 | 354,092 | +3,702 | ||

| SFRH7 | 250,067 | 250,505 | -438 | ||

| SFRM7 | 236,762 | 237,612 | -850 | ||

| SFRU7 | 181,727 | 183,873 | -2,146 | ||

| SFRZ7 | 169,185 | 172,159 | -2,974 | ||

| SFRH8 | 113,836 | 111,353 | +2,483 |

MNI NBP Preview - July 2024: Status Quo

Executive Summary:

- The NBP is expected to stand pat on rates again.

- The new inflation projection will steal the limelight.

- Governor Glapiński may reaffirm the NBP's hawkish stance.

Full preview including a summary of sell-side views here:

MNI NBP Preview - July 2024.pdf

The details of the updated macroeconomic projection will be the highlight of this week’s monetary policy meeting, which is otherwise widely expected to result in another on-hold decision. The National Bank of Poland (NBP) keeps signalling its intention to freeze rates at their current levels through the remainder of this year. Core inflation remains elevated amid robust wage growth, while the partial withdrawal of energy price caps is expected to boost headline in 2H2024. Against this backdrop, Governor Adam Glapiński may use Thursday’s press conference to reaffirm the NBP’s hawkish monetary policy stance.

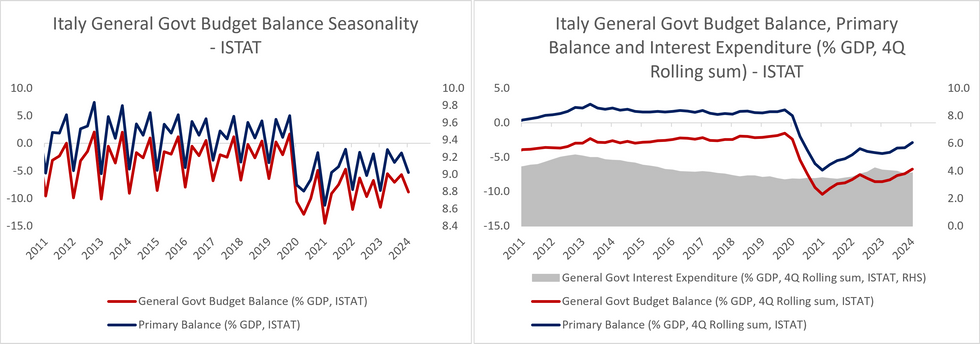

FISCAL: Q1 Seasonality Skews Italian Fiscal Deficit Higher

The Italian Q1 fiscal data looks worse than it probably is, though broader concerns around debt sustainability have not been alleviated.

- Although the general government cumulative deficit/GDP ratio rose to 8.8% (vs 7.4% prior), deficits are usually highest in Q1 before falling through the remainder of the year.

- Since 2000, Government revenues have fallen by an average 35% Q/Q in Q1, driven by a 50% fall in income taxes (which are then recouped in Q2 and Q4 as individuals file tax returns).

- Measured as a 4Q rolling sum, the deficit/GDP ratio actually fell to 6.7%, after Q1 2023’s 11.6% deficit dropped out of the calculation.

- An improvement in the budget deficit is expected in 2024 (e.g. Italian Treasury forecasts 4.3%, the EC 4.4%, and the current Bloomberg median 4.7%).

- The fall in the 4Q rolling measure suggests progress is being made here, but there is still some way to go.

- The primary balance showed similar dynamics to the wider deficit. The cumulative deficit to GDP was 5.3% in Q1 (vs 3.6% prior), but 2.9% on a 4Q rolling sum basis.

- Recent trends in the interest rate-growth differential "(r-g)" remain somewhat concerning. The sharp fall in Q1 nominal GDP growth (-6.6% Q/Q) meant that the 4Q rolling sum of (r-g) rose to -2.1pp, its highest since June 2021.

- If (r-g) is positive and a country runs fiscal deficits, it puts the government debt/GDP ratio on a potentially unstable and explosive path higher.

- The Italian debt/GDP ratio rose a touch to 137.7% in Q1 (vs 137.3% prior), and the EC expects this ratio to rise to 141.7% by 2025.

- The EC notes that this increase "mainly reflects a less favourable interest growth-rate differential and a debt-increasing stock-flow adjustment related to the delayed cash impact of government-supported housing renovation". The latter point refers to the controversial "Superbonus" scheme.

EUROPE ISSUANCE UPDATE:

UK auction results

- Strong 3-year gilt auction with a 0.4bp tail and the lowest accepted price of 98.255 matching the highs on the secondary market through the last 40 minutes of the auction.

- There was a little move higher in price on the release of the results with a post-auction high of 98.259 still well below the intraday high. Gilt futures saw very little reaction to the auction.

- GBP4bln of the 3.75% Mar-27 Gilt. Avg yield 4.441% (bid-to-cover 3.26x, tail 0.4bp).

German auction results

- E500mln (E493mln allotted) of the 0% Aug-30 Green Bund. Avg yield 2.47% (bid-to-offer 2.91x; bid-to-cover 2.96x).

- E500mln (E494mln allotted) of the 0% Aug-50 Green Bund. Avg yield 2.74% (bid-to-offer 3.28x; bid-to-cover 3.32x).

FOREX: Greenback Remains Favoured as US Yields Hold Monday Rally

- With the US yield curve consolidating and holding the majority of yesterday's rally, the greenback is firmer again headed into NY hours. The USD Index has topped the Monday high and remains within range of 106.130 - strength through which puts the greenback at the best level since early May.

- The single currency trades poorly, with both EUR/USD and EUR/GBP in the red. Moves come as focus remains on the French political process. Pollsters and betting odds continue to the fade the implied probability of the right-wing RN winning an outright majority after the election second round on Sunday. Preliminary Eurozone CPI came in alongside expectations at 2.5% - as indicated by the outturns from the composite regions including Germany yesterday and late last week.

- While GBP's Tuesday trade has been middling in G10, the pair remains within range of key support at the 1.2613 mark. Further selling pressure headed into the election on Thursday (results due through the night on Friday) would result in six-week lows for the pair and exposure of 1.2580, the 50% retracement for the upleg posted off the April low.

- JOLTS job openings data is the highlight of the US calendar Tuesday, with the ECB's central banking conference in Sintra also set to continue. The highlight today will likely be a panel appearance from Fed's Powell, ECB's Lagarde and BCB's Campos Neto at 1430BST/0930ET.

Expiries for Jul02 NY cut 1000ET (Source DTCC)

- USD/JPY: Y161.00($1.5bln)

EQUITIES: E-Mini S&P Eases Further Away From Last Week's Highs

- The trend condition in Eurostoxx 50 futures remains bullish and the recovery from the Jun 14 low appears to be an early reversal of the May 16 - Jun 14 correction. Attention is on 5039.84, a Fibonacci retracement. Clearance of this level would be a positive development. On the downside, a reversal lower would instead signal a resumption of the bearish corrective cycle that started May 16 and open 4846.00, the Apr 19 low and a key support.

- The trend condition in S&P E-Minis is unchanged and signals remain bullish. Resistance at 5430.75, the May 23 high and bull trigger, has recently been cleared. This break confirmed a resumption of the primary uptrend. Note that the recent pause in the trend appears to be flag formation - a bullish continuation signal. Sights are on 5594.66, a Fibonacci projection. Support to watch is 5488.93, the 20-day EMA.

COMMODITIES: WTI Futures Trading at Highest Level Since April

- A bull cycle in WTI futures remains in play and the contract traded higher Monday, starting the week on a bullish note. The recent breach of $80.11, the May 29 high and a key resistance, strengthened a bullish theme. Note too that $82.24, 76.4% of the Apr 12 - Jun 4 bear leg, has been cleared. This opens $85.27, the Apr 12 high and a bull trigger. Initial firm support to watch is $79.04, the 50-day EMA.

- A bear threat in Gold remains present and the yellow metal continues to trade closer to its recent lows. The sell-off on Jun 7 reinforced a short-term bearish theme. Price has pierced the 50-day EMA, at 2318.9. A clear break of this EMA would confirm a resumption of the reversal from May 20 and open $2277.4, the May 3 low. Clearance of this price point would also strengthen a bearish theme. Initial firm resistance is $2387.8, the Jun 7 high.

| Date | GMT/Local | Impact | Country | Event |

| 02/07/2024 | - | *** | Domestic-Made Vehicle Sales | |

| 02/07/2024 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 02/07/2024 | 1330/1530 | ECB's Lagarde in policy panel at ECB forum | ||

| 02/07/2024 | 1330/0930 | Fed Chair Jerome Powell | ||

| 02/07/2024 | 1400/1000 | *** | JOLTS jobs opening level | |

| 02/07/2024 | 1400/1000 | *** | JOLTS quits Rate | |

| 02/07/2024 | 1530/1130 | * | US Treasury Auction Result for Cash Management Bill | |

| 03/07/2024 | 0130/1130 | ** | Retail Trade | |

| 03/07/2024 | 0700/0300 | * | Turkey CPI | |

| 03/07/2024 | 0800/1000 | ECB's De Guindos chairing MonPol Cycles session | ||

| 03/07/2024 | 0900/1100 | ** | PPI | |

| 03/07/2024 | 0900/1100 | ECB's Cipollone chairing Productivty session | ||

| 03/07/2024 | 1030/1230 | ECB's Lane chairing panel on equilibirum interest rates | ||

| 03/07/2024 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 03/07/2024 | 1100/0700 | New York Fed's John Williams | ||

| 03/07/2024 | 1230/0830 | ** | Trade Balance | |

| 03/07/2024 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 03/07/2024 | 1230/0830 | *** | Jobless Claims | |

| 03/07/2024 | 1330/1530 | ECB's Lagarde closing remarks at ECB Forum | ||

| 03/07/2024 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/07/2024 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/07/2024 | 1600/1200 | ** | Natural Gas Stocks | |

| 03/07/2024 | 1800/1400 | *** | FOMC Minutes |