Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

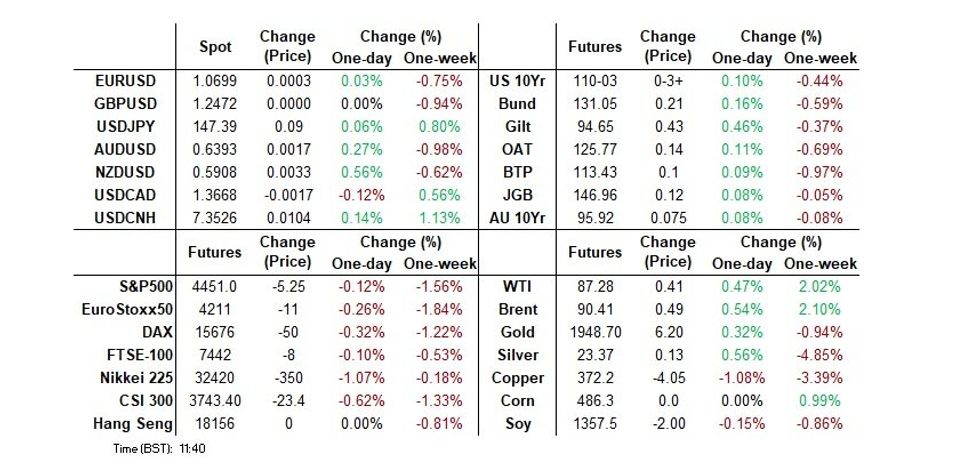

- USD/CNH printed a new cycle high at 7.3623 early Friday, narrowing the gap with key resistance and the bull trigger at 7.3749.

- Little movement in Fed pricing ahead of pre-meeting blackout, degree of cuts priced remains comfortably off recent dovish extremes.

- Canadian labour market data headlines a limited docket ahead of the weekend.

US TSYS: Off Best Levels Into NY Trade

Tsys have pulled back from best levels alongside wider core global FI markets.

- Cash Tsys run little changed to 2bp richer, with 5s outperforming on the curve.

- TYZ3 is around mid-range, last +0-04.

- The initial Asia-Pac bid, coupled with early London reaction to the move and an extension of the recent dovish BoE repricing, then provided a second round bid in the Asia-London handover.

- Asia-Pac highs in TYZ3 remain intact after the contract pushed above pre-ISM Services levels.

- As we noted elsewhere, the Asia-Pac bid was seemingly linked to a combination of Nikkei 225 & USD weakness. The latter came on the latest thinly veiled FX intervention threats out of Japan, although that isn’t a U.S. Tsy positive from a flow perspective.

- Lower tier domestic data and comments on payments innovation from Fed’s Barr are unlikely to do much for markets in NY hours.

STIR: Fed Rate Path Holding Near Pre-ISM Services Beat

- Fed Funds implied rates are unchanged overnight for near-term meetings and slightly higher further out, but don’t change the yesterday’s takeaway of pushing back close to pre-ISM Services levels.

- Cumulative hikes from 5.33% effective: +1.5bp Sep and +11.5bp Nov to a terminal 5.45%, still closely followed by +11bp for Dec.

- Cuts from Nov terminal: 39bp to Jun’24 (from 40bp yesterday) and 109bp to Dec’24 (from 108bp). It’s been a volatile week for 2024 rate cut expectations, closing on Monday at 124bp before recent lows of 101bp after ISM.

- Logan (’23 voter) after the close yesterday: “My base case is that there is work left to do […] I’m not yet convinced that we’ve extinguished excess inflation. But in today’s complex economic environment, returning inflation to 2% will require a carefully calibrated approach — not endless buckets of cold water”.

Source: Bloomberg

Source: Bloomberg

BONDS: Unwinding Some Of Asia/Early London Bid

Core global FI markets reverse some of their Asia/early London gains, with no real headline flow to drive the move off bests.

- Weakness in U.S. & European equity futures may have helped the space base in recent trade.

- The Asia-Pac bid was seemingly linked to a combination of Nikkei 225 & USD weakness. The latter came on latest thinly veiled FX intervention threats out of Japan, although that isn’t a U.S. Tsy positive from a flow perspective.

- Bund futures last +25, with German cash benchmarks 1-2bp richer.

- Gilt futures haven’t closed the opening gap higher, last +45, while UK cash benchmarks are 2bp richer to 0.5bp cheaper as the curve twist steepens.

- Early support for Gilts came from another downtick in BoE-dated OIS, as the recent dovish repricing extended. That move is now off extremes. Underperformance was noted in the long end from the off, with news the DMO is considering holding a tender for a 40+-Year gilt on 27 September a potential driver (that wasn’t a complete surprise given DMO guidance alongside the latest quarterly issuance calendar release).

STIR: BBG Survey Loosely In Line With '23 ECB Market Pricing

With the pre-meeting ECB quiet period in play we look at the BBG survey ahead of next week’s decision.

- The survey shows a near-even split when it comes to the hike/hold debate, with a slim majority (17/32) looking for no change next week.

- Beyond next week’s meeting a similarly slim majority expect the deposit rate to peak at 4.00% in the current cycle (equating to 1 further 25bp hike from prevailing levels).

- This outlook isn’t too dissimilar to market pricing, with a little under 10bp of tightening showing for next week, while terminal deposit rate pricing hovers between 3.90-3.95%.

- The debate at next week’s meeting will centre on the trade off between soft economic activity data and still elevated (but slowing) inflation.

- A slim majority in the BBG survey see the deposit rate at 3.75% by March, with 3x cuts in ’24 providing median expectation at present.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Sep-23 | 3.747 | +9.5 |

| Oct-23 | 3.808 | +15.6 |

| Dec-23 | 3.836 | +18.4 |

| Jan-24 | 3.821 | +16.9 |

| Mar-24 | 3.770 | +11.8 |

| Apr-24 | 3.695 | +4.3 |

| Jun-24 | 3.589 | -6.3 |

| Jul-24 | 3.481 | -17.1 |

FOREX: USD/CNH Touches New Cycle High as Fix Comes in Notably Higher

- USD/CNH printed a new cycle high at 7.3623 early Friday, narrowing the gap with key resistance and the bull trigger at 7.3749. Clearance here would put the pair at the highest levels since 2007, however a sell-on-rallies theme has emerged, with the pair off the best levels headed into the NY crossover. Chinese inflation data will cross over the weekend, with CPI expected to exit a deflationary state and the degree of PPI deflation expected to ease again.

- The greenback sits modestly softer, however the USD Index remains comfortably inside the broader up-trend posted off the mid-July lows. The JPY underperforms, shaking off any strength built earlier in the week via verbal intervention from cabinet ministers Matsuno and Kanda.

- USD/JPY slipped to overnight lows of 146.60 alongside the notably higher USD/CNY fix, but has recovered all losses headed through to NY hours, keeping the underlying uptrend intact to finish the week.

- NZD, AUD are among the session's best performers, however the overnight high for AUD/USD at 0.6415 remain well inside the week's early ranges.

- Focus for the session ahead turns to the Canadian jobs release for August, and final US wholesale inventories and trade sales data for July. Fed's Barr is the sole central bank speaker,

FX OPTIONS: Expiries for Sep08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0625-30(E530mln), $1.0700(E2.2bln), $1.0746-50(E1.3bln), $1.0795-15(E1.8bln), $1.0825-30(E1.5bln)

- USD/JPY: Y146.10-25($850mln), Y146.90-00($951mln)

- GBP/USD: $1.2500(Gbp1.2bln), $1.2569-80(Gbp621mln)

- AUD/USD: $0.6450(A$619mln), $0.6550(A$934mln), $0.6600(A$1.4bln)

- USD/CAD: C$1.3485-00($1.8bln), C$1.3600($700mln)

- USD/CNY: Cny7.3100($924mln)

CHINA STOCKS: A Modest Downtick To End The Week, Data, Property Sales & G20 Eyed

MNI (London) - Benchmark Chinese stock indices edged lower Friday, with continued worry re: the Chinese economic outlook noted as the impulse from the recent raft of policy measures faded further.

- The CSI 300 lost ~0.5%, edging closer to recent lows.

- The Hong Kong Exchange was closed owing to adverse weather conditions, meaning that the HK-China Stock Connect scheme and Chinese H shares were closed.

- Chinese inflation data will cross over the weekend, with CPI expected to exit a deflationary state and the degree of PPI deflation expected to ease again.

- Elsewhere, monthly credit and economic activity data will hit over the next week.

- It is also worth noting that weekend Chinese property sales will likely come under increased focus, recent stimulus provided a meaningful uptick last weekend.

- On that front, policy advisors and market analysts told our Beijing team that “local governments are weighing whether to scrap rules limiting the purchase of multiple houses by homeowners should the latest mortgage rule relaxations fail to stimulate sales during the Sept-Oct peak season.”

- Finally, Chinese Premier Li will be at the G20 summit over the weekend, with China reportedly looking to raise the issue of improved access to advanced semiconductors (per BBG sources).

EQUITIES: EUROSTOXX 50 Pierces Key Support

- The E-mini S&P contract traded lower yesterday and a bear cycle remains in play. Key resistance has been defined at 4547.75, Sep 1 high. A break is required to reinstate the recent bullish theme. Note that recent gains stalled at the area of resistance around the former bull channel base - drawn from the Mar 13 low. The line intersects at 4547.83. This is a bearish development and a continuation lower would expose key support at 4350.00, Aug 18 low.

- A bear cycle in EUROSTOXX 50 futures remains in play and the contract is trading lower today. Price has pierced key support at 4187.00, the Aug 18 low and bear trigger. Clearance of this level would strengthen bearish conditions and open 4177.40 next, 61.8% of the Mar 20 - Jul 31 bull leg. Key resistance has been defined at 4358.00, the Aug 30 high. Initial firm resistance is seen at 4289.30, the 20-day EMA.

COMMODITIES: Bull Cycle In WTI Remains In Play

- On the commodity front, Gold is trading closer to this week’s lows. Key support to watch lies at $1903.9, the Aug 25 low. A break of this level would be viewed as a bearish development and highlight the fact that the recovery between Aug 21 - Sep 1 has been a correction. This would expose $1884.9, the Aug 21 low. On the upside, initial firm resistance is seen at $1930.9, the 50-day EMA. Key resistance is at $1953.0, the Sep 4 high.

- In the oil space, the uptrend in WTI futures remains intact. The recent break of resistance at $84.16, the Aug 10 high, confirmed a resumption of the uptrend and this maintains the bullish price sequence of higher highs and higher lows. Note that moving average studies are in a bull mode position, highlighting current positive sentiment. Sights are on the psychological $90.00 handle. On the downside, initial firm support to watch lies at $82.50, the 20-day EMA.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/09/2023 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 08/09/2023 | 1230/0830 | ** |  | US | WASDE Weekly Import/Export |

| 08/09/2023 | 1300/0900 | | US | Fed Vice Chair Michael Barr | |

| 08/09/2023 | 1400/1000 | ** | | US | Wholesale Trade |

| 08/09/2023 | 1500/1100 | | US | San Francisco Fed's Mary Daly | |

| 08/09/2023 | 1900/1500 | * | | US | Consumer Credit |

| 09/09/2023 | 0130/0930 | *** |  | CN | CPI |

| 09/09/2023 | 0130/0930 | *** | | CN | Producer Price Index |

| 11/09/2023 | 0600/0800 | * |  | NO | CPI Norway |

| 11/09/2023 | 0800/1000 | * |  | IT | Industrial Production |

| 11/09/2023 | - | *** | | CN | Money Supply |

| 11/09/2023 | - | *** | | CN | New Loans |

| 11/09/2023 | - | *** | | CN | Social Financing |

| 11/09/2023 | 1500/1100 | ** | | US | NY Fed Survey of Consumer Expectations |

| 11/09/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 11/09/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 11/09/2023 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

| 12/09/2023 | 2300/0000 |  | UK | BOE's Mann to Speak in Canada |

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok