US TSYS: Paring Modest Gains As US Filters In, Core PCE Inflation Watched

Treasuries have moved off highs with the US filtering in, but for the most part keep to a modest rally after a lack of hawkish rhetoric from BoJ Governor Ueda.

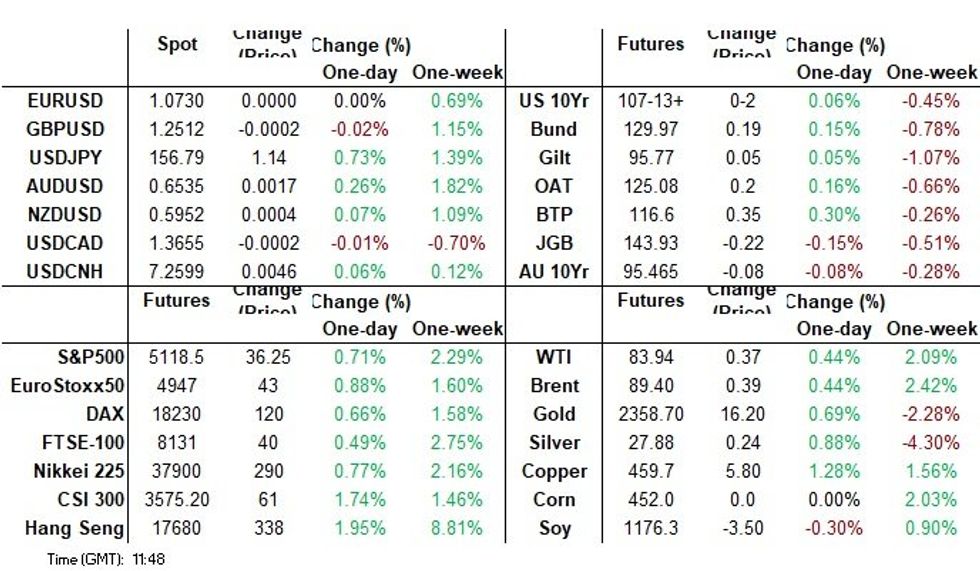

- Cash yields range from 0.2bp lower (2s) to 1.5bp higher (20s & 30s), flattening with 2s10s at -30.6bps and still firmly within the week’s range.

- TYM4 sits at 107-13 (+ 01+) off an earlier high of 107-18, on solid but not particularly high cumulative volumes approaching 340k.

- The trend direction remains down, with yesterday seeing a fresh cycle low of 107-04 (Apr 25 low) and with moving average studies also in a bear-mode set-up. Further support is seen at a Fibo projection of 106-27.

- Focus is firmly on data today and especially core PCE, whilst the earnings calendar winds down for the week in terms of notable names (Exxon is largest for the day, already out with a miss for Q1 adj EPS of $2.06 vs 2.19 expected).

- Data: Personal income/spending & PCE inflation Mar (0830ET), U.Mich Apr final (1000ET), Kansas City Fed services Apr (1100ET)

- No issuance

US TSY FUTURES: OI Points To Another Round Of Relatively Large Net Short Setting On Thursday

Yesterday’s PCE-driven sell off and preliminary OI data points to net short setting as the dominant positioning factor on the Tsy futures curve on Thursday.

- Net shorts seemed to be added across most contracts, with some apparent light long cover in UXY futures providing the only meaningful exception.

- That left a net DV01 equivalent of ~$7.5mn short exposure added across the curve. While a little shallower than the apparent net short setting seen on Wednesday, it still represents a fairly notable positioning move.

- A reminder that the latest CFTC CoT continued to point to net short positioning across the futures curve, although some of those positions had been trimmed.

- The CFTC CoT positioning report will be skewed by basis trades.

| 25-Apr-24 | 24-Apr-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,112,974 | 4,089,609 | +23,365 | +843,494 |

| FV | 6,056,811 | 6,002,163 | +54,648 | +2,234,782 |

| TY | 4,535,038 | 4,501,766 | +33,272 | +2,092,401 |

| UXY | 2,052,930 | 2,060,257 | -7,327 | -619,208 |

| US | 1,575,330 | 1,566,316 | +9,014 | +1,117,049 |

| WN | 1,635,395 | 1,626,036 | +9,359 | +1,770,397 |

| Total | +122,331 | +7,438,914 |

STIR: Minimal Impact From BoJ, Focus On Monthly Core PCE

Fed Funds implied rates are only marginally lower overnight after the BoJ left policy unchanged and with Ueda not offering any hawkish rhetoric.

- They keep the majority of the impact from yesterday’s core PCE strength and another lower-than-expected set of jobless claims data.

- Today’s data focus turns to the monthly PCE data, including the distribution of that surprisingly strong core PCE, and finalized U.Mich inflation expectations.

- Cumulative cuts from 5.33% effective: 1bp May, 3bp Jun, 9bp Jul, 19bp Sep, 25bp Nov and 35bp Dec.

STIR: OI Points To Mix Of Short Setting & Long Cover In SOFR Futures On Thursday

The combination of yesterday’s move lower in SOFR futures and preliminary OI data points to a mix of net short setting and long cover as Q1 PCE data triggered another hawkish round of Fed repricing.

- Net short setting seemed to dominate in the reds and greens, while net long cover was seemingly the dominant positioning factor in the whites.

- Net pack OI was closer to unchanged in the blues.

| 25-Apr-24 | 24-Apr-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRH4 | 932,138 | 940,793 | -8,655 | Whites | -17,297 |

| SFRM4 | 1,133,353 | 1,117,032 | +16,321 | Reds | +10,795 |

| SFRU4 | 999,277 | 993,029 | +6,248 | Greens | +15,341 |

| SFRZ4 | 1,187,636 | 1,218,847 | -31,211 | Blues | -1,324 |

| SFRH5 | 732,918 | 730,599 | +2,319 | ||

| SFRM5 | 816,398 | 802,529 | +13,869 | ||

| SFRU5 | 713,804 | 715,987 | -2,183 | ||

| SFRZ5 | 790,257 | 793,467 | -3,210 | ||

| SFRH6 | 483,356 | 479,420 | +3,936 | ||

| SFRM6 | 503,294 | 498,084 | +5,210 | ||

| SFRU6 | 381,222 | 376,921 | +4,301 | ||

| SFRZ6 | 353,467 | 351,573 | +1,894 | ||

| SFRH7 | 230,369 | 230,405 | -36 | ||

| SFRM7 | 184,271 | 183,673 | +598 | ||

| SFRU7 | 168,180 | 168,351 | -171 | ||

| SFRZ7 | 142,732 | 144,447 | -1,715 |

EGBS/GILTS: A Little Firmer As BoJ Holds The Line

Core global FI markets hold onto the bulk of their early Friday rally, although JPY FX activity has generated far greater interest.

- A lack of hawkish offerings from BoJ Governor Ueda helped bonds to rally around the European cash open.

- Steady to slightly lower inflation expectations in the ECB’s latest consumer expectations survey wouldn’t have harmed the bid.

- Bund futures are a little off session highs, last +20 or so at 130.00. The German cash curve has bull flattened, with yields 0.5-2.5bp lower.

- OATs are little changed to a touch tighter vs. German peers, as participants await potential French sovereign rating updates from Fitch & Moody’s. The recent French fiscal deterioration has fed into OATs, with the impending rating updates having the potential to move the market on Monday (we will provide more colour later).

- Peripheral paper is generally tighter to Bunds, with a light rally in EUR STIR markets, some tightening in benchmark credit spreads and the recovery in equities since yesterday’s European close feeding in.

- Gilt futures are +15 or so at 95.85. Bulls failed to force a break above 96.00, with the bearish technical backdrop intact.

- Cash gilt yields are 1-3bp lower across the curve, with some flattening seen.

- Light dovish moves are seen in GBP STIRs.

- The European & UK calendars are light from here, which will leave focus on cross-market spill over and macro headline flow.

FOREX: JPY Volatility in Focus Post-BOJ, USD Index at Fresh Two-Week Low

- Global focus has been on the Japanese Yen on Friday, as the dust settles from an unchanged Bank of Japan decision overnight. Governor Ueda stated the yen's recent weakness has not affected underling inflation, which the Bank continue to watch closely.

- Overall, this has paved the way for further JPY weakness on the session, with USDJPY printing a fresh multi-decade high of 156.82. There was a momentary sharp pullback to 154.99, with markets potentially getting spooked re MOF intervention but this move was quickly faded, with the pair tracking back above 156.50 as we approach the NY crossover.

- Firmer equities in Europe are moderately bolstering risk sentiment, with the likes of AUD and NZD outperforming and the USD index printing a fresh two-week low below 105.50.

- As such, AUDJPY is up 1% and EURJPY stand 0.70% in the green, with the latter piercing initial resistance at 168.25, the 1.50 projection of the Jan 1 - 19 - Feb 1 price swing.

- EURUSD has edged to fresh highs, briefly printing above 1.0750. The market will monitor a clear break of the 20-day EMA (1.0726), which would signal scope for a stronger technical recovery.

- US PCE Core Deflator crosses this afternoon, alongside personal income and spending figures. UMich consumer sentiment and inflation expectations round off the week’s data calendar. Potential for comments from ECB's Centeno, participating in a panel in Frankfurt.

FOREX OPTIONS: Expiries for Apr26 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0680 (890mln), 1.0685 (411mln), 1.0700 (858mln), 1.0725 (882mln), 1.0730 (464mln), 1.0740 (256mln), 1.0750 (1.17bn), 1.0784 (714mln).

- GBPUSD: 1.2500 (677mln).

- USDJPY: 155.00 (1.21bn), 156.00 (377mln), 156.25 (220mln), 156.50 (531mln).

- AUDUSD: 0.6500 (463mln), 0.6550 (300mln).

- NZDUSD; 0.5925 (230mln), 0.5940 (386mln).

- USDCNY: 7.2370 (550mln), 7.24 (277mln), 7.2500 (728mln).

EQUITIES: Short-Term Resistance In S&P E-Minis Remains Intact

In the equity space, the short-term trend condition in S&P E-Minis remains bearish and the latest recovery appears - for now - to be a correction. The contract has recently cleared the 50-day EMA, signalling scope for a continuation lower. Sights are on 4907.57 next, 50.0% of the Oct 27 ‘23 - Apr 1 bull leg. Firm resistance is 5138.90, the 20-day EMA. A clear break of the average would signal a possible reversal.

- EUROSTOXX 50 futures are holding on to the bulk of the recovery from 4762.00, the Apr 19 low. The contract has breached the 20-day EMA and resistance at 4990.00, Apr 15 high. This highlights a potentially stronger reversal. A continuation higher would expose the bull trigger at 5079.00, Apr 2 high. Initial support to watch is 4869.70, the 50-day EMA.

COMMODITIES: WTI Continues To Trade Above Key Short-Term Support

On the commodity front, Gold has this week pierced the 20-day EMA and this highlights the start of a possible corrective cycle. A resumption of weakness would signal scope for an extension towards $2229.4, the 50-day EMA. Note that a short-term bear cycle would allow a significant overbought condition to unwind. Key resistance and the bull trigger is at $2431.5, the recent Apr 12 high.

- In the oil space, WTI futures have recovered from their recent lows and price continues to trade above key support at $81.03, the 50-day EMA. The recent move lower highlights a corrective phase and a clear break of the 50-day average would signal scope for a deeper retracement towards $76.07, the Mar 11 low. On the upside, key resistance and the bull trigger has been defined at $86.97, the Apr 12 high.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/04/2024 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 26/04/2024 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 26/04/2024 | 1500/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 26/04/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |