Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- US curve leaning flatter, but inside overnight range

- USD favoured in currency markets, outperforming most others

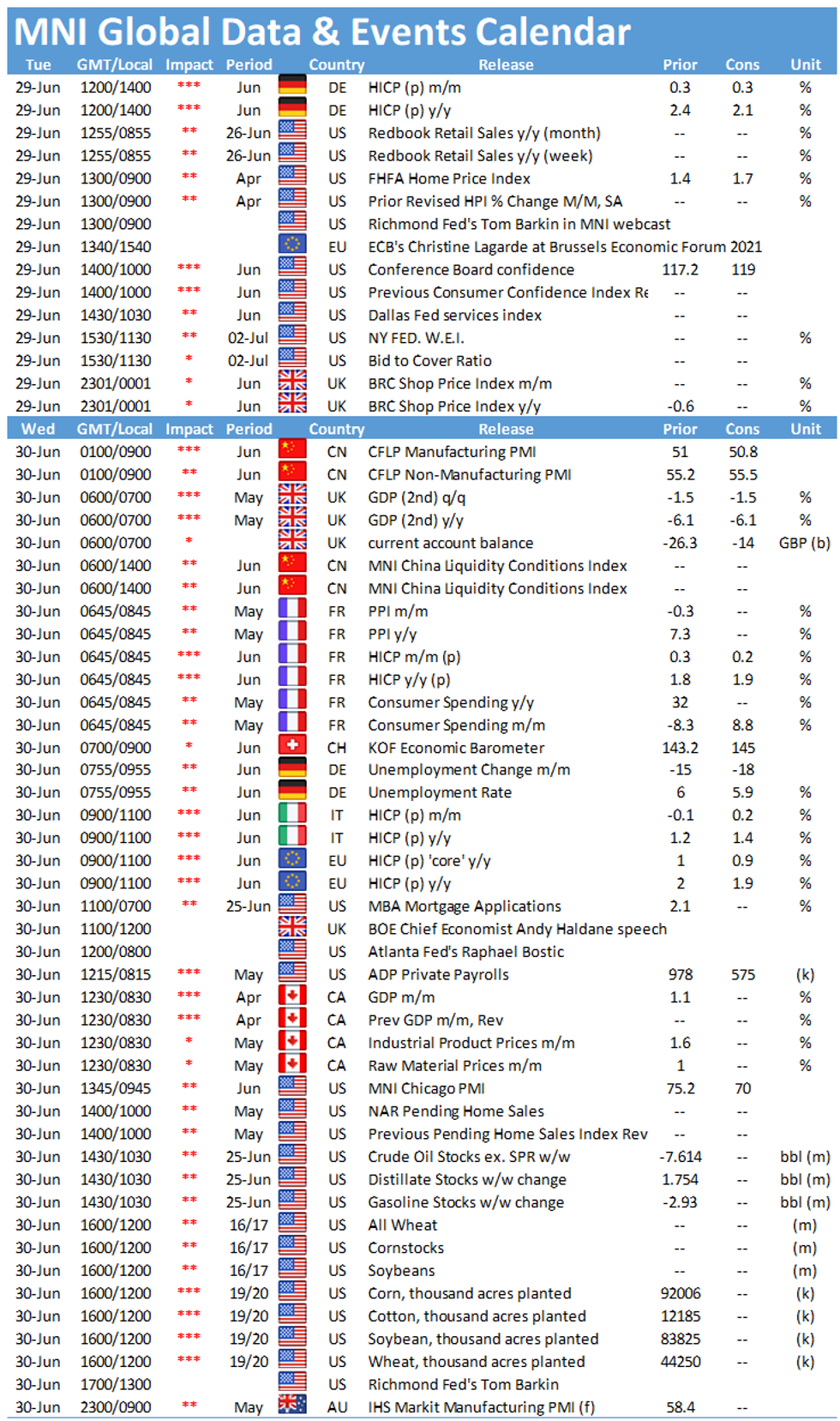

- Fed's Barkin takes part in MNI event, Lagarde & Weidmann also due

US TSYS SUMMARY: Curve leans flatter, in line with EGBs

US Treasuries have traded within their overnight ranges during the European morning session.

- Curve trades flat in line for Europe Govies, albeit leaning flatter on the margin, but well within ranges traded post FOMC.

- We have seen little or heard little in terms of Month End flow, but it is worth noting that for some clearer at least, this Month, extensions are on the low side.

- Looking ahead, more speakers are scheduled, which today includes, Fed Barkin (At MNI Event).

- ECB Lagarde, Villeroy, Weidmann, and BoE Hauser.

- 2y yields up 0.2bp today at 0.257%

- 5y yields up 0.4bp today at 0.901%

- 10y yields up 0.3bp today at 1.481%

- 30y yields down -0.3bp today at 2.094%

- 2s10s unch today at 122.3bp

- 10s30s down -0.6bp today at 61.3bp

EGB/GILT SUMMARY: Mixed Session Amid Background Covid Concerns

Core European govies have traded weaker this morning while the EGB periphery has largely firmed. The dollar has been on the front foot against global FX, while European equities have posted gains. Rising infections involving the Delta variant of the coronavirus and tightening restrictions in some developed and emerging economies have stoked economic uncertainty.

- Gilt yields are broadly 1bp higher on the day with the long end of the curve close to flat.

- Bunds are slightly offered albeit with yields trading near yesterday's close.

- It is a similar story for OATs with the curve also flattening.

- BTPs have inched higher with cash yields 1bp lower on the day.

- Data published by Nationwide show UK house prices soaring 13.4% Y/Y in June, up from 10.9% the previous month. Elsewhere, regional German CPI data for June broadly edged lower, while Euro area economic confidence for the same month improved.

- There will be a combined EUR15bn 5y/30y dual tranche NGEU bonds issued today.

EUROPE ISSUANCE UPDATE

Eurozone NGEU Syndication: Final terms set

5Y size set at E9bln (MNI exp E8-9bln), spread set at MS-11bps (original guidance at MS-8bps area)

Books above E70bln.

30Y Fixed size set at E6bln (MNI exp E6-7bln), spread set at MS+22bps (original guidance MS+25bps area)

Books above E60bln

EUROPE OPTION FLOW SUMMARY

Eurozone:

0RN1 100.50/100.62cs, bought for 0.25 in 2.5k

0RU1 100.12p, bought for 0.25 in 2k

UK:

3LU1 98.37/98.25ps, bought for 0.25 in 2k

FOREX: USD is favoured

The story so far during the morning European session, has been the better bid in the USD.

- The currency extended higher across the board and is up across G10s and EM, and that's despite risk still tilted to the upside, with Mini S&P hovering near all time high.

- Worst performers against the Greenbacks are the Kiwi, the Aussie and the NOK, all down above half a percent at the time of typing.

- AUD is weighted by further lockdown, with Perth joining Sydney and Darwin.

- USDNOK is up 0.52% and now eye the 22/06 high at 8.6151.

- In terms of Month End flow, this has so far been limited, with very little reported from desks.

- Citi's prelim month-end model for June indicates slight USD sales.

- And Barcap, preliminary run of month-end rebalancing model points to moderate USD selling against all majors.

- Looking ahead, more speakers are scheduled but unlikely to hear anything new, since we have heard from them previously.

- Today includes, Fed Barkin (At MNI Event), and ECB Lagarde, Villeroy, Weidmann, BoE Hauser.

- Attention though, is already turning to the US NFP Friday.

FX OPTIONS: Expiries for Jun29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1900-10(E623mln)

- USD/JPY: Y109.30-45($1.4bln), Y110.00-15($1.1bln-USD puts), Y110.85-90($515mln), Y111.00-10($526mln),

- Y112.00($1.25bln-USD calls)

- NZD/USD: $0.7260(N$705mln)

- USD/CAD: C$1.2300-10($570mln)

- USD/CNY: Cny6.4000($510mln)

- USD/MXN: Mxn19.88($890mln)

Price Signal Summary - S&P Bulls Still In Charge

- In the equity space, S&P E-minis maintain a bullish theme and sights are set on the 4300.00 handle. EUROSTOXX 50 futures found support Jun 21 at 4015.00. Attention is on the Jun 18 sell-off that in pattern terms is a bearish engulfing candle, signaling a potential S/T top. The key directional triggers are; 4015.00, Jun 21 low and 4153.00, Jun 17 and the bull trigger

- In FX, the USD remains on a bullish path despite the recent corrective pullback. The EURUSD focus is on 1.1837 next, 76.4% of the Mar 31 - May 25 rally. GBPUSD remains vulnerable. Attention is on 1.3717 next, Apr 16 low. The bear trigger is 1.3787, Jun 21 low. USDJPY needle still points north. Attention is on 111.30/64, Mar 26, 2020 high and 1.0% 10-dma envelope.

- On the commodity front, Gold continues to consolidate. The outlook remains weak and the current consolidation appears to be a bear flag. This reinforces a bear theme and the focus is on $1756.2, low Apr 29. The Oil market trend condition remains bullish and pullbacks are considered corrective. Brent (Q1) focus is $76.97, 1.23 projection of Mar 23 - May 18 - May 21 price swing. Support lies at $73.22, the 20-day EMA. WTI (Q1) sights are set on $75.01, 1.382 projection of Mar 23 - May 18 - May 21 price swing. Watch support at $70.93, the 20-day EMA.

- Within FI, Bund futures is consolidating. The contract last week probed support at 171.80, Jun 17 low. A stronger sell-off would expose 171.37, Jun 3 low and 170.99, Mar 31 low and a key short-term support. Key support to watch in Gilt futures is unchanged at 126.70, Jun 3 low and remains an important pivot level. The key resistance is at 128.39, Jun 11 high.

EQUITIES: European and US stocks a bit higher

- Japan's NIKKEI down 235.41 pts or -0.81% at 28812.61 and the TOPIX down 16.19 pts or -0.82% at 1949.48

- China's SHANGHAI closed down 33.194 pts or -0.92% at 3573.178 and the HANG SENG ended 274.2 pts lower or -0.94% at 28994.1

- German Dax up 79.75 pts or +0.51% at 15637.48, FTSE 100 up 6.78 pts or +0.1% at 7082.55, CAC 40 up 13.46 pts or +0.21% at 6573.96 and Euro Stoxx 50 up 10.32 pts or +0.25% at 4101.43.

- Dow Jones mini up 11 pts or +0.03% at 34173, S&P 500 mini down 4 pts or -0.09% at 4277.25, NASDAQ mini down 30.75 pts or -0.21% at 14480.5.

COMMODITIES: Generally lower

- WTI Crude down $0.36 or -0.49% at $72.54

- Natural Gas up $0 or +0.11% at $3.598

- Gold spot down $8.28 or -0.47% at $1770.2

- Copper down $5.6 or -1.31% at $422.25

- Silver down $0.16 or -0.63% at $25.9476

- Platinum down $15.96 or -1.46% at $1079.66

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.