Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

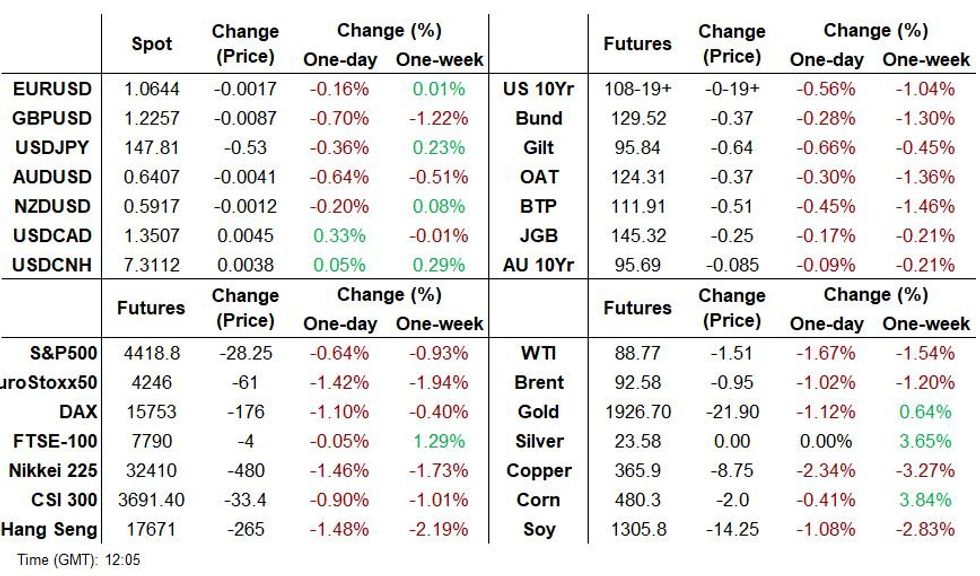

- GBP extended losses after the BoE voted 5-4 to maintain rates at 5.25% vs market pricing leaning to a hike.

- This followed an unexpected hold by the SNB, and priced-in hikes by the Riksbank and Norges Bank, helping extend the post-FOMC dollar rally.

- Up next are the BoE press conference, initial jobless claims, Philly Fed, and existing home sales data.

BOE MPC VOTES 5-4 TO LEAVES BANK RATE UNCHANGED AT 5.25%

- FOUR BOE MPC MEMBERS VOTED FOR 25BPS HIKE

- BOE MPC CUNLIFFE, GREENE, HASKEL, MANN BACKED 25BPS HIKE

- BOE KEEPS GUIDANCE, MORE TIGHTENING IF INFLATION PERSISTS

STIR: Unchanged BoE Rate Steepens BoE Pricing, 20bp Of Further Rightening Now Seen

BoE-dated OIS comes in as the Bank leaves policy rate unchanged, with a steepening impulse as the market removes pre-decision pricing of a hike for today (which was the slightly favoured outcome pre-decision).

- Liquid contracts now show -11bp to +4bp on the day. Twist steepening.

- Terminal policy rate pricing indicates ~20bp of cumulative hikes from here vs. just over 25bp pre-decision, still pricing a roughly 4 in 5 chance of another hike despite today’s hold.

- Ahead of the decision we suggested that no hike with unchanged guidance would result in a more meagre 10bp of tightening being reflected in terminal rate pricing.

- The narrow 5-4 vote split will have prevented this adjustment from taking place, along with some the comments from the Bank. The combination of the two points to a ‘hawkish hold.’

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Sep-23 | 5.204 | +1.9 |

| Nov-23 | 5.301 | +11.6 |

| Dec-23 | 5.355 | +17.0 |

| Feb-24 | 5.383 | +19.8 |

| Mar-24 | 5.382 | +19.7 |

| May-24 | 5.362 | +17.7 |

| Jun-24 | 5.317 | +13.2 |

| Aug-24 | 5.234 | +4.9 |

US TSYS: Latest Losses Pared, Initial Claims and 10Y TIPS To Come

- Treasuries have continued to pull back from fresh cycle (and multi-year) highs for yields seen in Asia-Pac hours or more recently for the very long end.

- The curve twist steepens with benchmarks 2.5bp richer to 2.5bp cheaper, pivoting around 5s.

- It sees TYZ3 trades at 108-21+ off a low of 108-16 that cleared a Fibo projection level in the process, with strong volumes of 400k.

- It has been a heavy morning for central banks, with the BoE surprisingly holding at 5.25% and the SNB at 1.75% (cons 2.00%), whilst the Norges Bank and Riksbank both hiked 25bps as expected to 4.25% and 4%, indicating peaks of 4.5% and 4.1% respectively.

- NY hours will see weekly jobless claims for a payrolls reference week, the Philly Fed survey and existing home sales data. The $15B 10Y TIPS re-open highlights supply, with the 10Y real yield having touched fresh highs since 2009.

STIR: Fed Implied Rates Only Modestly Trim An Extended Post-FOMC Push Higher

- Fed Funds implied rates for 2024 meetings have pulled back slightly on the day but it comes from particularly elevated levels as a hawkish reaction continued to build after Chair Powell’s conference finished.

- Shown in the table comparing levels before both the announcement and press conference, the main takeaway has been a further large trimming of cut expectations on net.

- Cumulative hikes from 5.33% effective: +7.5bp for Nov, +13bp for Dec and +14bp to 5.47% for Jan.

- Cuts from terminal: 21bp to Jun’24 (27bp pre-decision) and 74bp to Dec’24 (86bp pre-decision) with the latter to an effective 4.73% vs 5.1% end-2024 dot. The first cut is seen landing in September.

- Earlier today, the SNB and BoE (the latter somewhat) surprisingly held rates, whilst the Norges Bank and Riksbank both hiked 25bps as expected to 4.25% and 4%, whilst indicating peaks of 4.5% and 4.1% respectively.

EUROPE AUCTIONS UPDATE

Spain auction results

- *It was a decent auction with the stop price exceeding the pre-auction mid-price for all Oblis on offer today.

- * The bid-to-cover on the 3-year Bono was a bit weaker than in July (but it was stronger for the 5-year Obli compared to May).

Spain issued E6.304bln (from a E5.5-6.5bln target range).

- * There was a bit of weakness post-auction, but all in line with moves in other EGBs.

- * E2.588bln of the 2.80% May-26 Bono. Avg yield 3.527% (bid-to-cover 1.65x).

- * E1.983bln of the 0% Jan-28 Obli. Avg yield 3.426% (bid-to-cover 2.2x).

- * E1.733bln of the 0.50% Oct-31 Obli. Avg yield 3.591% (bid-to-cover 1.71x).

France MT OAT auction results

France sells the top of the E10-11bln target in another decent auction with the stop price in excess of the pre-auction mid-price for all three MT OATs on offer.

- * E4.703bln of the 2.50% Sep-26 OAT. Avg yield 3.27% (bid-to-cover 2.33x).

- * E2.785bln of the 0.75% May-28 OAT. Avg yield 3.12% (bid-to-cover 1.99x).

- * E3.51bln of the 2.75% Feb-29 OAT. Avg yield 3.14% (bid-to-cover 2.26x).

France linker auction results:

- * E651mln of the 0.10% Mar-29 OATei. Avg yield 0.57% (bid-to-cover 3.06x).

- * E609mln of the 0.10% Mar-32 OATi. Avg yield 0.58% (bid-to-cover 2.8x).

- * E488mln of the 0.10% Jul-38 Green OATei. Avg yield 0.82% (bid-to-cover 3.44x).

FOREX: USD Underpinned Post-FOMC

USD remains underpinned in the wake of the FOMC decision (dot plot tweaks for ’24 & ’25 at hawkish end of expectations, Powell noting potential that r* is higher and a firmer tone re: economic growth), weakness in equities has helped, although the BBDXY failed to breach early September highs.

- JPY has benefited from the broader equity market weakness, after the initial yield differential impulse saw USD/JPY to fresh ’23 highs. USD/JPY now sits at Y148.20, with JPY atop the G10 FX table.

- NOK has benefitted from hawkish adjustments to the Norges Bank’s rate track, which came alongside the signalled 25bp hike. The Bank also alluded to the likelihood of another rate hike, most likely in December.

- Elsewhere, the SEK failed to hold on to knee-jerk gains surrounding the bank’s FX hedging policy, which came ahead of time vs. most expectations. Still, the hedging amount outlined was in line with rough calculations and the upward shift in the Riksbank’s rate path forecast was perhaps a little shallower than could have been expected, even with the Governor pointing to the likelihood of one further rate hike. EUR/SEK trades comfortably off session lows.

- CHF finds itself at the bottom of the G10 pack after the SNB left policy rates unchanged (BBG consensus looked for a hike). While Chairman Jordan pointed to the potential for further hikes and noted that the inflation battle is not yet over, some of the language deployed and the SNB playing down the idea of a hawkish pause has also weighed on the CHF.

- GBP extended struggles after the not-fully priced BoE hold. Cable shows below $1.23 for the first time since April.

FX OPTIONS: Close Option Expiries At NY Cut

There are a number of close option expiries at NY cut today, based on the latest DTCC data.

- At a $0.65 strike there are ~$1bn of AUD Call options. At $0.6450 there are $410mn of AUD Puts and at $0.6448 we have $297mn of AUD Calls.

- AUD/USD Overnight Implied Volatility is slightly elevated, albeit well within recent ranges, at 13.10% as option markets price in a $0.6389-$0.6497 range today.

EQUITIES - S&P E-Minis Support Remains Exposed

- A bear cycle in the E-mini S&P contract remains in play and this week’s break lower reinforces current conditions. Support at 4483.25, the Sep 7 low, has been breached. A continuation lower would expose 4397.75, the Aug 18 low and the next key support. Initial key resistance has been defined at 4566.00, the Sep 15 high. A break of this level would be seen as a bullish development. First resistance is at 4511.54, the 20-day EMA.

- A strong sell-off in EUROSTOXX 50 futures Monday highlighted a bearish start to this week’s session. A continuation lower would refocus attention on key near-term support at 4210.00, the Sep 8 low. Clearance of this level would confirm a resumption of the downtrend that started late July. Key short-term resistance has been defined at 4359.00, the Sep 15 high.

COMMODITIES - Corrective Cycle In Oil Remains In Play

- On the commodity front, Gold traded higher yesterday but quickly pulled back from the session high. The recent breach of the 50-day EMA does highlight a possible developing bullish threat. Key resistance is at $1953.0, the Sep 1 high where a break is required to confirm a bullish theme. On the downside, $1901.1, the Sep 14 low, marks a key near-term support. A breach of this level would strengthen a bearish theme and expose $1884.9, the Aug 21 low.

- In the oil space, the uptrend in WTI futures remains intact, however, the contract has entered a short-term bearish corrective cycle.The trend condition is overbought and a move lower would allow this to unwind. The first key support to watch lies at $86.25, the 20-day EMA and is a potential short-term objective. On the upside, clearance of Tuesday’s $92.43 high would confirm a resumption of the uptrend and open $94.66, a Fibonacci projection, the 2.236 projection of the Jun 28 - Jul 13 - Jul 17 price swing.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/09/2023 | 1230/0830 | *** |  | US | Jobless Claims |

| 21/09/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 21/09/2023 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 21/09/2023 | 1230/0830 | * | | US | Current Account Balance |

| 21/09/2023 | 1400/1000 | *** | | US | NAR existing home sales |

| 21/09/2023 | 1400/1600 | ** |  | EU | Consumer Confidence Indicator (p) |

| 21/09/2023 | 1400/1600 | | EU | ECB's Lagarde Lectures in Marseille | |

| 21/09/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 21/09/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 21/09/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 21/09/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 22/09/2023 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

| 22/09/2023 | 2301/0001 | ** |  | UK | Gfk Monthly Consumer Confidence |

| 22/09/2023 | 0030/0930 | ** |  | JP | Jibun Bank Flash Japan PMI |

| 22/09/2023 | 0200/1100 | *** | | JP | BOJ policy announcement |

| 22/09/2023 | 0600/0700 | *** | | UK | Retail Sales |

| 22/09/2023 | 0700/0900 | *** |  | ES | GDP (f) |

| 22/09/2023 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 22/09/2023 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 22/09/2023 | 0730/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 22/09/2023 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 22/09/2023 | 0800/1000 | ** | | EU | S&P Global Services PMI (p) |

| 22/09/2023 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 22/09/2023 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 22/09/2023 | 0830/0930 | *** | | UK | S&P Global Manufacturing PMI flash |

| 22/09/2023 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 22/09/2023 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 22/09/2023 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 22/09/2023 | 1100/1300 | | EU | ECB's de Guindos Speaks at Event | |

| 22/09/2023 | 1230/0830 | ** |  | CA | Retail Trade |

| 22/09/2023 | 1250/0850 | | US | Fed Governor Lisa Cook | |

| 22/09/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 22/09/2023 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 22/09/2023 | 1400/1000 | | US | Boston Fed's Susan Collins | |

| 22/09/2023 | 1700/1300 | | US | San Francisco Fed's Mary Daly | |

| 22/09/2023 | 1700/1300 | | US | Minneapolis Fed's Neel Kashkari |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.