Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Bonds boosted as Biden Considers Brainard

- USD/JPY extends downtick, lower for a fourth session

- CB speak remains thick and fast, with a number of Fed, BoE and ECB members up

US TSYS SUMMARY: Brainard Buzz Boosts Tsys Ahead Of PPI And 10Y Supply

Treasuries have gained overnight Tuesday, ahead of PPI data and 10Y supply.

- The 2-Yr yield is down 2.6bps at 0.4168%, 5-Yr is down 3.1bps at 1.0861%, 10-Yr is down 2.8bps at 1.4619%, and 30-Yr is down 2.6bps at 1.856%.

- Dec 10-Yr futures (TY) up 9/32 at 131-18.5 (L: 131-10.5 / H: 131-20)

- Tsys gained in Asia-Pac hours on a BBG sources piece that Pres Biden has interviewed Fed Gov Brainard for the Chair's position - she's up to ~33% probability vs 22% 24 hours ago on PredictIt. Implying she's seen as a more dovish alternative to Powell.

- $39B 10Y Note auction features at 1300ET.

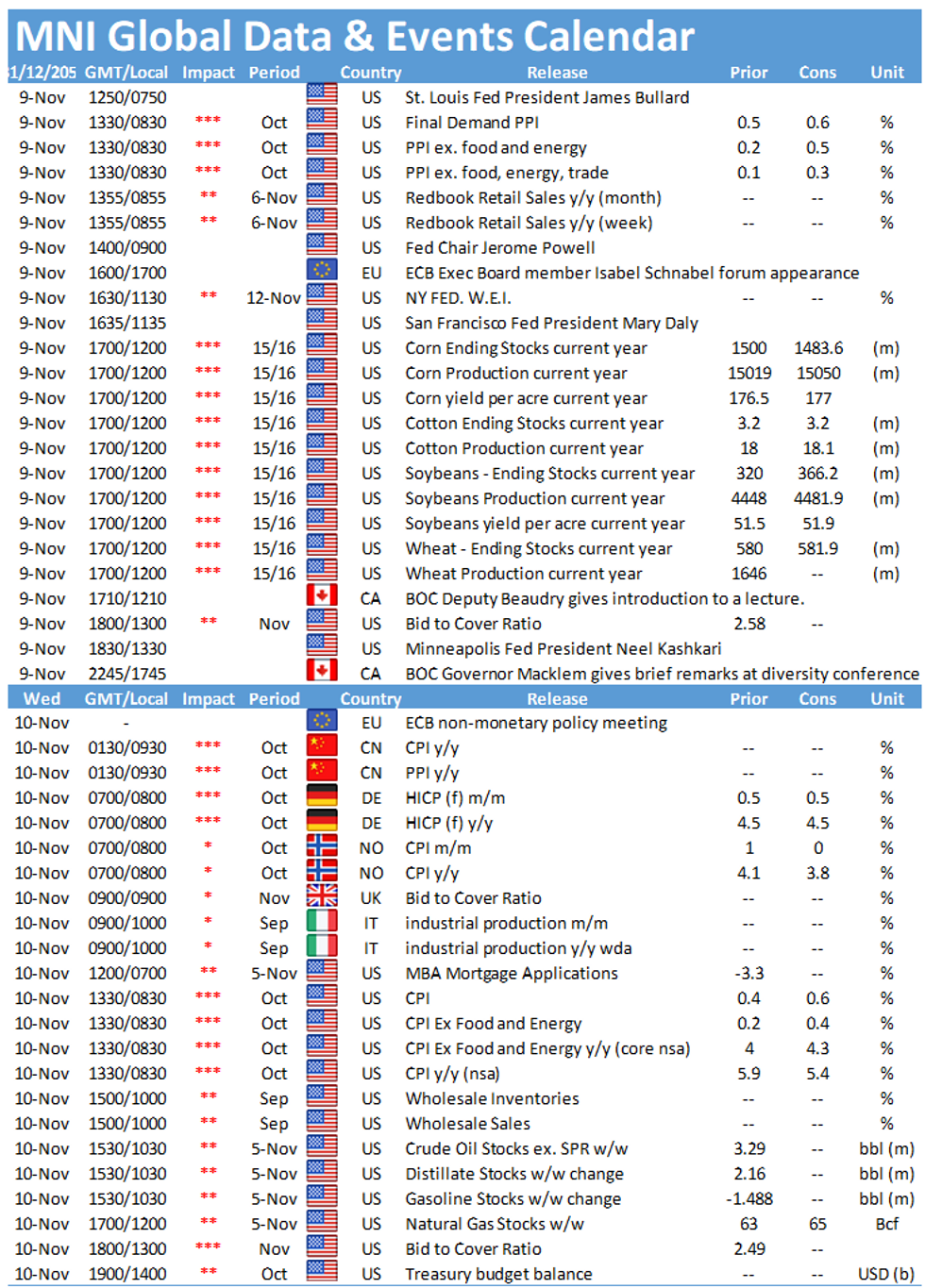

- Another busy day for Fed speakers: St Louis' Bullard at 0750ET and 0900ET at a UBS event; Powell speaking at a diversity conference at 0900ET; SF's Daly speaking at the NABE Conference at 1135ET, and Minn's Kashkari in a town hall at 1330ET. That's it for scheduled Fed speakers until Friday.

- The October PPI report at 0830ET is the data focus. Earlier, NFIB small business optimism came in a little below expectations, decelerating to 98.2 in Oct (99.1 prior, 99.5 survey).

EGB/GILT SUMMARY: Core Bonds Bid, With Gilts Tipped to Highest Since End-Sept

- Bund futures trade well ahead of the NY crossover, with prices nearing Friday's best print of 171.24. In yield space, the German curve trades modestly flatter, with outperformance noted in the longer-end.

- Bonds have received an underlying bid globally on the back of reports from the US that Brainard had been interviewed by Biden for the Fed Chair position, a story that's considerably boosted the implied odds for her succeeding over current Chair Powell.

- In the UK, Gilts are similarly bid, gaining a tailwind from firmer German and US markets. Today's high print at 127.24 marks the highest price on the active contract since end-September.

- US PPI data crosses later today, with M/M price pressures expected to tick higher ahead of Wednesday's possibly more influential CPI release. Central bank speak remains dominant, with Fed's Bullard, Powell Daly & Kashkari due as well as ECB's Lagarde, Knot and BoE's Bailey. Topics are varied, with speeches ranging from inequality to diversity to banking supervision.

EUROPE ISSUANCE UPDATE

Germany allots €4.777bln 0% Dec-23 Schatz, Avg yield -0.71% (Prev. -0.69%), Bid-to-cover 1.00x (Prev. 1.35x), Buba cover 1.26x (Prev. 1.72x)

Netherlands sells €1.835bln Jan-38 DSL, Avg yield 0.118% (Prev. 0.188%), Price 98.11 (Prev. 96.90)

FOREX: Markets Chew Through CB Speak Ahead of US PPI

- Germany's ZEW survey came in mixed, with current situation falling short of forecast while expectations recorded a decent beat on expectations. The read through for EUR was muted however, with EUR/USD continue to trade just either side of the 1.16 handle.

- A weaker greenback today twinned with a stronger JPY has extended the streak of lower lows, with the pair on track to record four consecutive sessions of losses. 112.34 undercuts as first support as the 50-day EMA ahead of 112.08 which marks the Sep 30 high and recent breakout level.

- NZD is the poorest performing currency in G10, partially reversing the outperformance from the Sunday open as markets responded to the government's announcement of re-opening for a number of the larger cities. NZD/USD remains comfortably above Monday's low of 0.7104 as well as the 200-dma of 0.7100.

- US PPI data crosses later today, with M/M price pressures expected to tick higher ahead of Wednesday's possibly more influential CPI release. Central bank speak remains dominant, with Fed's Bullard, Powell Daly & Kashkari due as well as ECB's Lagarde, Knot and BoE's Bailey. Topics are varied, with speeches ranging from inequality to diversity to banking supervision.

FX OPTIONS: Expiries for Nov09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.3bln)

- USD/JPY: Y113.70($2.0bln)

- EUR/GBP: Gbp0.8500(E593mln)

- USD/CAD: C$1.2400-05($700mln), C$1.2460($1.1bln)

Price Signal Summary - USDJPY Cracks A Key Short-Term Support

- In the equity space, the uptrend in the S&P E-minis remains intact and underlying sentiment is still clearly bullish. The contract is consolidating near recent highs and the focus is on 4717.00 next, 1.50 projection of the Jul 19 - Aug 16 - Aug 19 price swing. EUROSTOXX 50 futures are consolidating. The trend needle continues to point north and the focus is on 4371.00, 1.236 projection of Jul 19-Sep 6-Oct 6 2020 swing (cont)

- In FX, EURUSD short-term gains are considered corrective. Last week's print below 1.1524 Friday, the Oct 12 low reinforces the current bearish theme and signals a resumption of the downtrend. The focus is on 1.1493, 50.0% retracement of the Mar '20 - Jan '21 bull phase. Initial resistance this morning is at 1.1617, Nov 4 high. GBPUSD remains vulnerable following last week's bearish pressure and short-term gains are considered corrective. Attention is on the key support at 1.3412, Sep 29 low. Firm resistance is seen at 1.3697, the 50-day EMA. USDJPY has breached support at 113.00, the Oct 12 low. The break signals scope for a deeper pullback and opens 112.08, Sep 30 high.

- On the commodity front, Gold reversed course late last week and maintains a firmer short-term tone. The turnaround opens $1834.0, Sep 3 high. Last week's sell-off in WTI resulted in a breach of $80.58, Oct 28 low and the contract cleared the 20-day EMA. Despite the most recent recovery, the 50-day EMA at $77.51 remains exposed. Key resistance has been defined at $85.41, Oct 25 high. The initial resistance to watch this morning is $83.42, high Nov 4.

- In the FI space, the rally in Bund futures last week breached former resistance at 169.83, Oct 27 high. Note too that futures have also cleared the 50-day EMA. This opens 171.95, 61.8% of the Aug - Nov sell-off. Gilts maintain a firmer tone and the recent double bottom reversal continues to play out. The focus is on 127.69 next, Sep 21 high.

EQUITIES: Stocks Firmer, Keeping Alltime Highs Under Pressure

- Core European markets are almost uniformly higher at the midpoint, with Spanish and French markets outperforming. Europe's communication services, energy and real estate sectors are leading the way higher, with tech and financials slightly lagging. A modest flattening of most core European sovereign curves has worked against the larger continental bank names.

- US futures are higher, with the e-mini S&P adding a few points to keep the outlook tilted higher. Yesterday's 4707 print is the first target ahead of Friday's alltime high at 4711.75.

- Focus turns to today's PPI data ahead of tomorrow's CPI release. The litany of Fed speakers will also take focus, with topics ranging from inequality to diversity to banking supervision.

COMMODITIES: Crude at Weekly High While US Mulls SPR

- Markets remain on watch for a statement from the White House as the energy secretary earlier in the week flagged possible action from Biden on high gas and fuel prices. Deputy Energy Sec Turk spoke this morning, flagging that oil price forecasts will be a factor in any decision the Strategic Petroleum Reserve, which currently holds a capacity of around 620mln bbls.

- Oil markets remain undeterred, with WTI and Brent crude futures both in positive territory and eyeing the Nov04 highs at $83.42/bbl.

- Gold and silver are more rangebound, with precious metals oscillating either side of unchanged. Gold reversed course late last week following the bounce off Wednesday's low of $1759.0.

- The turnaround reinstates a potential bullish outlook and the yellow metal has traded above $1813.8, Oct 22 high. The breach of this level strengthens a short-term bullish case and signals scope for a climb towards $1834.0, the Sep 3 high.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok