Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

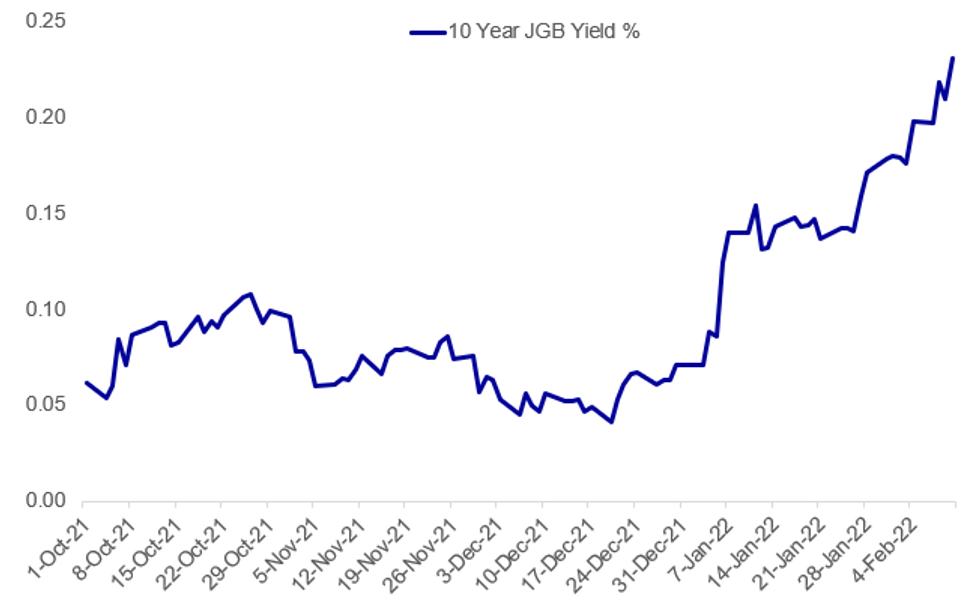

- BOJ TO LAUNCH UNLIMITED 10Y JGB PURCHASE OPERATION AS YIELDS RISE

- U.S. CPI SEEN MODERATING M/M IN JANUARY

- RIKSBANK HOLDS, SEES QE STOCK STEADY IN 2022

- ECB TO LET BANK CAPITAL RELIEF EXPIRE

Fig. 1: BOJ Steps In As 10Y JGB Yield Nears 0.25%

Source: BBG, MNI

Source: BBG, MNI

NEWS:

BANK OF JAPAN (BBG): The Bank of Japan offered to buy an unlimited amount of bonds at a fixed rate, pushing back against weeks of trader speculation about policy normalization. The central bank will buy 10-year bonds at 0.25% on Feb. 14, according to a statement on its website. This is the first such operation since July 2018 as yields creep closer to its tolerated level under its yield curve control policy. Policy normalization bets have gathered pace in recent months as soaring inflation spurs global central banks to unwind pandemic-era stimulus and raise rates. The BOJ has remained an outlier, with Governor Haruhiko Kuroda repeatedly stating the need to keep easing.

BANK OF JAPAN (MNI INTERVIEW): Any rise in Japanese inflation above 2% will prove unsustainable and should not prompt the Bank of Japan to reduce monetary easing, a former BOJ chief economist told MNI. For full article contact sales@marketnews.com

MNI US INFLATION PREVIEW: U.S. CPI for January is released on Thu at 0830ET/1330GMT.

- Consensus is for a modest moderation after a strong December, with the median seeing core CPI at +0.5% M/M (average 0.45%) after 0.55% M/M.

- Core inflation was previously led by surging core goods (+1.9% M/M) as core services plateaued, with both categories expected to ease this month and the latter potentially slowed by first round effects from Omicron.

- With markets increasingly pricing in more hikes, the largest reaction could come from a downside surprise.

- See the full report here including previews from 12 sell-side analysts.

SWEDEN RIKSBANK (MNI BRIEF): The Riskbank left policy unchanged at its February meeting, but brought forward the projected timing of the first hike to H2 2024. There had previously been divisions on the Executive Board over the case for early non-reinvestment of maturing assets acquired through quantitative easing but the board forecast that asset holdings would "remain approximately unchanged in 2022', a restatement of its existing position. The detailed rate forecast showed the policy rate starting to edge up, to 0.06%, at the start of 2024 and then to climb steadily to 0.31% by the end of the forecast period three years out. That profile was steeper than the previous one, from November, which had the policy rate at 0.19% at the end of the forecast,. Some analysts had expected the projected timing of the first hike to be brought forward into 2023 but the changes the Riksbank has made are modest and do not represent any big overhaul of the policy approach of leaving the existing stimulus in place this calendar year.

ECB/ EUROZONE BANKS: Banks will be required to hold larger capital reserves going forward, ECB banking supervisors said Thursday, with most Euro area banks already operating at capital levels above those required. Capital requirements and guidance are increased from 14.9% in 2021 to 15.1% of risk-weighted assets in 2022. Capital requirements and guidance in CET1 increase from 10.5% in 2021 to 10.6% of risk-weighted assets in 2022.

ECB / EUROZONE BANKS: Pillar 2 capital relief for banks will end in December this year, with leverage relief set to end in March, the ECB said Thursday -- a strong signal that the central bank's regulators at least judge the Covid-19 pandemic’s crisis phase is over. “The capital space that we created for banks at the onset of the pandemic helped them to continue lending to households and businesses,” ECB Supervisory Board chair Andrea Enria said. “Today we are providing clarity on the path back to normality. We are confirming the initially envisaged timeline for a return to normal supervision of banks’ capital adequacy and leverage.”

RBA (MNI INSIGHT): The Reserve Bank of Australia is unlikely to re-invest any of its AUD350 billion government and semi-government bond portfolio when it begins to tighten interest rates and will take a call at its May meeting on the mechanics as reported, MNI understands. For full article contact sales@marketnews.com

UK-RUSSIA (RTRS): British foreign minister Liz Truss told Russia on Thursday there was still time to end its aggression towards Ukraine, which, she said, was undermining the country's international standing and strengthening the resolve of the NATO alliance. "The aggression by the Russian government and attempts to relitigate the past are seriously undermining Russia's international standing," she told a news conference in Moscow, standing alongside Russian Foreign Minister Sergei Lavrov. "These acts have actually had the effect of strengthening NATO's resolve and turning the Ukrainian people further away from Russia."

UK-RUSSIA: At a joint presser between Russian Foreign Minister Sergey Lavrov and his UK counterpart Liz Truss in Moscow, Lavrov offers stark criticism of the United Kingdom, saying that talks with the UK are 'like speaking to a deaf person who listens but does not hear'. Body language between the two extremely frosty. Truss threatens the "toughest sanctions" if Russia invades Ukraine. Catherine Philip at The Times tweets: "Lavrov next to Truss in Moscow: Uk-Russia relations are at "lowest level over many years". Then pointedly talks about scale of trade between two countries, after Truss said before talks she would threaten sanctions. Lavrov talks about how he told Truss about the ties Russia is building with China (translation: we've got a very big Big Brother)".

EU INFLATION: The European Commission is forecasting eurozone inflation to be below the European Central Bank's 2% target by the end of 2023, according to the latest round of economic forecasts out of Brussels. Despite upping their outlook for end-2023 from the Autumn projection, the EC is forecasting inflation at just 1.7%, up from the 1.4% seen in November. "Inflation in the euro area is projected to peak in the first quarter of 2022 and remain above 3% until the third quarter of the year," the report notes, before adding that "as the pressures from supply constraints and energy prices fade, inflation is expected to decline markedly" in Q4, before settling "below 2% next year."

PORTUGAL POLITICS: The final results from Portugal's legislative elections have finally come through, confirming that Prime Minister Antonio Costa's centre-left Socialist Party (PS) has won an outright majority in the Assembly of the Republic. The PS now holds 119 seats in the 230-member chamber, ahead of the 116 required for an outright majority. The PS gained 11 seats in the snap election, called after the PS' two former leftist allies refused to vote for the gov'ts budget in late-2021.

DATA:

CHINA: New Loans Rise to Record High in January

- CHINA JAN. AGGREGATE FINANCING 6,170.0B YUAN; EST. 5,400.0B

- CHINA JAN. NEW YUAN LOANS 3,980.0B YUAN; EST. 3,700.0B

- CHINA NEW YUAN LOANS IN JANUARY ARE HIGHEST ON RECORD

MNI: NORWAY Jan CPI CPI -0.9% M/M, +3.2% Y/Y

- MNI: NORWAY Jan CORE CPI -0.3% M/M, +1.3% Y/Y

- NORWAY JAN CPI-ATE -0.3% M/M, +1.3% Y/Y

FIXED INCOME: EGBs underperform on ECB sources story while Tsys await CPI

Bunds and gilts have moved lower this morning while Treasuries have outperformed ahead of this afternoon's CPI print.

- The market is focusing on a Bloomberg sources story released overnight which stated that an increasing number of Governing Council members were losing faith in the ECB's staff projections and were moving in a more hawkish direction. There has been discussion of this in the market for some time, but the report has still seen the Euribor strip under pressure while the German curve has bear steepened and peripheral spreads have widened (led by Italy +2.1bp to 10y Bund and Greece +3.8bp).

- There has been little market-moving UK news so far, with the SONIA strip largely reacting to the wider risk-on enviroment. Governor Bailey's speech later will be closely watched for any more explicit pushback on market rates.

- CPI is the highlight of the day for Treasuries. Markets are looking for around a 0.45% print for both headline and core CPI. This will be the over encompassing event for markets today, with a surprise either way likely to be market-moving.

- TY1 futures are down -0-2 today at 126-22 with 10y UST yields unch at 1.938% and 2y yields down -1.6bp at 1.350%.

- Bund futures are down -0.14 today at 165.72 with 10y Bund yields up 1.7bp at 0.227% and Schatz yields down -1.1bp at -0.366%.

- Gilt futures are down -0.15 today at 120.76 with 10y yields up 1.3bp at 1.441% and 2y yields up 0.4bp at 1.279%.

FOREX: JPY Slips as BoJ Step In to Cap Yields

- The rally in the Japanese curve continued apace across Asia-Pac hours, pushing the 10y yield to the highest levels since early 2016 and putting the BoJ's yield cap under considerable pressure. In response the Bank stepped in with an unscheduled asset purchase programme, committing themselves to buying an unlimited quantity of 10y JGBs as part of their yield curve control policy tool. USD/JPY rallied in response, adding around 30 pips to touch session highs of Y115.88, keeping the JPY close to the bottom of the G10 pile.

- SEK underperformed all others through the European morning, including the JPY, following a dovish turn from Sweden's Riksbank. The bank's governor Ingves stepped in to block a growing view among the bank board that the pace of asset purchases should be tapered over the coming period. As a result, EUR/SEK rallied to touch 10.4849, just shy of the Monday high at 10.4868.

- US inflation data takes focus going forward, with markets expecting a new multi-decade high for the Y/Y read at 7.2%, with more pressure on the core reading also. Weekly jobless claims also cross, with speeches from ECB's de Guindos, Villeroy and Lane. The Mexican central bank decision is also due.

EQUITIES: FTSE Returns To Pre-Pandemic Levels

- Asian markets closed stronger: Japan's NIKKEI closed up 116.21 pts or +0.42% at 27696.08 and the TOPIX ended 10.39 pts higher or +0.53% at 1962.61. China's SHANGHAI closed up 5.961 pts or +0.17% at 3485.907 and the HANG SENG ended 94.36 pts higher or +0.38% at 24924.35.

- European equities are gaining (FTSE hitting post-2020 nominal highs), with the German Dax up 17.78 pts or +0.11% at 15499.44, FTSE 100 up 10.06 pts or +0.13% at 7653.74, CAC 40 up 8.37 pts or +0.12% at 7139.43 and Euro Stoxx 50 up 5.15 pts or +0.12% at 4209.6.

- U.S. futures are mostly lower, led by tech, with the Dow Jones mini up 13 pts or +0.04% at 35654, S&P 500 mini down 10 pts or -0.22% at 4567.75, NASDAQ mini down 57.5 pts or -0.38% at 14980.75.

COMMODITIES: Mixed So Far, Oil And Copper Leading

- WTI Crude up $0.75 or +0.84% at $90.4

- Natural Gas down $0.01 or -0.2% at $4.004

- Gold spot down $1.71 or -0.09% at $1831.61

- Copper up $6.45 or +1.4% at $466.5

- Silver up $0.01 or +0.05% at $23.3256

- Platinum down $10.55 or -1.02% at $1027.32

LOOK AHEAD:

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/02/2022 | 1000/1100 |  | EU | European Commission Winter Economic Forecasts | |

| 10/02/2022 | 1200/1300 | | EU | ECB de Guindos on Europe post-covid at LSE | |

| 10/02/2022 | 1315/1415 | | EU | ECB Lane on supply chain disruptions panel discussion | |

| 10/02/2022 | 1330/0830 | ** |  | US | Jobless Claims |

| 10/02/2022 | 1330/0830 | *** | | US | CPI |

| 10/02/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 10/02/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 10/02/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 10/02/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 10/02/2022 | 1700/1700 |  | UK | BOE Bailey speech at TheCityUK Dinner | |

| 10/02/2022 | 1800/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 10/02/2022 | 1900/1400 | ** | | US | Treasury Budget |

| 10/02/2022 | 1900/1400 | *** |  | MX | Mexico Interest Rate |

| 10/02/2022 | 0100/2000 | | US | Richmond Fed's Tom Barkin | |

| 11/02/2022 | 0700/0700 | ** | | UK | UK monthly GDP |

| 11/02/2022 | 0700/0700 | ** | | UK | Output in the Construction Industry |

| 11/02/2022 | 0700/0700 | ** | | UK | Index of Services |

| 11/02/2022 | 0700/0700 | *** | | UK | Index of Production |

| 11/02/2022 | 0700/0700 | ** | | UK | Trade Balance |

| 11/02/2022 | 0700/0700 | *** | | UK | GDP First Estimate |

| 11/02/2022 | 0700/0800 | *** |  | DE | HICP (f) |

| 11/02/2022 | 0730/0830 | *** |  | CH | CPI |

| 11/02/2022 | 0805/0905 | | EU | ECB Elderson on sustainable finance discussion at Finance Summit | |

| 11/02/2022 | 1500/1000 | *** | | US | University of Michigan Sentiment Index (p) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.