Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

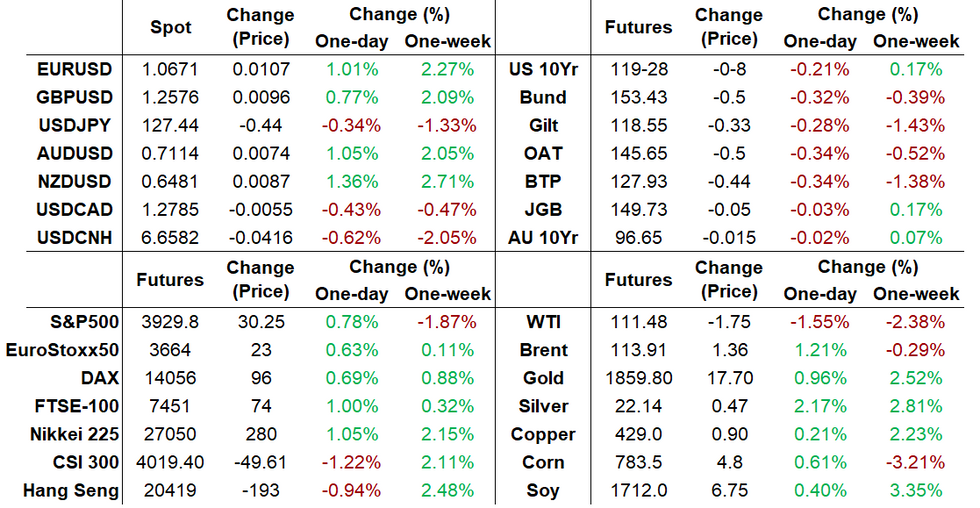

- US dollar weakness has been the focus overnight, with the DXY driven to 1-month lows by multiple developments.

- EURUSD hit May's high after ECB Pres Lagarde backed a July hike and the end of negative rates by September.

- Earlier, the yuan jumped vs USD after Pres Biden said he was considering lifting some Chinese tariffs.

US TSYS: Treasuries Tentatively Soften

- Modest risk-on sees Cash Tsys sell-off largely across the curve, driven by higher real yields despite relatively little change in Fed hike expectations for the rest of 2022.

- Fresh highs in the number of new Covid cases in Beijing are eyed despite a steady decline in Shanghai cases in recent days, with a trade-off in lower growth and higher inflation implications. Further support comes very recently from China releasing multiple measures to further stabilize its economy.

- 2YY +3.6bps at 2.616%, 5YY +3.9bps at 2.839%, 10YY +4.7bps at 2.860% and 30YY +3.3bps at 3.019%.

- TYM2 sits 9+ ticks lower at 119-26+ on marginally below average volumes. It currently holds onto last week’s gains and whilst the primary trend direction is down, any resumption of strength would open important short-term resistance at 120-18+ (Apr 27 high). Support still eyed at 118-16 (May 18 low).

- Fedspeak: Bostic (’24) at 1200ET, George (’22) at 1930ET

- Data: Chicago Fed Nat Activity Index for April at 0830ET

- Bill issuance: US Tsy $45B 13W, $42B 26W bill auctions at 1130ET

STIR FUTURES: Hanging Onto 2x50bp Fed Hikes

- Fed Funds implied hikes for near-term meetings are little changed from Friday afternoon’s softer levels, with 51bps for Jun and 100.5bps Jul.

- Hikes further out have cooled recently, in part from Beijing reporting the most new Covid cases of the current outbreak, but at 139bp for Sep and 193bp for Dec are close to where they ended last week. More explicit guidance from ECB’s Lagarde (APP net purchases end very early in Q3 allowing rate lift-off in July) saw a small uptick that’s since been reversed.

- Light on data and Fedspeak today, with only Bostic (’24 voter) scheduled for the main session at 1200ET before George (’22) later at 1930ET at an Agricultural Symposium.

Source: Bloomberg

Source: Bloomberg

EGBs/GILTS: Lagarde leads Schatz yields higher

- The main event of the morning session has been the release of a blog post by ECB President Christine Lagarde in which she explicitly stated that she expected the APP to end "very early" in Q3 with a July rate hike and an end to negative rates by the end of Q3. This is the most explicit policy steer from an ECB Executive Board member to date and has seen the Euribor curve steepen and Schatz yields increase more than 2-year UST or gilt yields. Lagarde was actually confirming something that is more than fully priced into the market - but the market will see this as the base case, with the prospect of more being needed if inflation moves even higher.

- Looking ahead there is a policy panel at an Austrian National Bank event. The panel topic will be "Monetary policy, policy interaction and inflation in a post-pandemic world with severe geopolitic altensions" with panelists including Holzmann, Bundesbank's Nagel and BOE Governor Bailey.

- We are also due to hear from ECB's de Cos and Villeroy and the Fed's Bostic while this morning's German IFO survey was slightly stronger than expected.

- TY1 futures are down -0-7+ today at 119-28+ with 10y UST yields up 4.1bp at 2.824% and 2y yields up 3.2bp at 2.616%.

- Bund futures are down -0.56 today at 153.37 with 10y Bund yields up 4.0bp at 0.981% and Schatz yields up 5.3bp at 0.380%.

- Gilt futures are down -0.38 today at 118.50 with 10y yields up 2.6bp at 1.918% and 2y yields up 2.4bp at 1.518%.

EUROPE BOND AUCTION RESULTS

Belgium:

- E1.258bln 0.80% Jun-25 OLO, 0.67% yield, 1.81x cover

- E1.757bln 0.35% Jun-32 OLO, 1.57% yield, 1.64x cover

- E792mln 2.15% Jun-66 OLO, 2.118% yield, 1.74x cover

EU:

- E2.5bln 1.00% Jul-32 EU NGEU, 1.525% yield, 1.38x cover

Greece:

- E500mln 3.90% Jan-33 GGB, 3.61% yield, 3.19x cover

BOND / RATES OPTIONS

Europe:

- DUN2 109.50/109.20 ps for 10/10.25 in 3k

- ERU2 99.87^ v 99.75p, bought the straddle up to 13 in 4.1k

US:

- EDU2 97.625c, bought for 10 in ~26.6k (ref 97.38)

FOREX: EUR boosted by ECB Lagarde

- Early mover in FX, was in Asia, with USDCNY and USDCNH falling close to 3 big figures, after Biden said that Chinese tariffs imposed by the Trump administration were under consideration.

- Although not all good news regarding potential relations, after Biden replied "yes" when asked if he was willing to defend Taiwan.

- CNY and CNH are now off their highs at the time of typing.

- In G10, the Pound extended gains, with over pips range, as the Dollar trades on the back foot, helped by some recovery in Equities, but note that risk is edging back towards their session lows.

- Next upside target for Cable is at 1.2600, followed by 1.2638 High May 4 and a key resistance.

- EUR found some support and has seen some broader base buying, following ECB Lagarde's Hawkish comments.

- "I expect net purchases under the APP to end very early in the third quarter. This would allow us a rate lift-off at our meeting in July, in line with our forward guidance. Based on the current outlook, we are likely to be in a position to exit negative interest rates by the end of the third quarter."

- The currency test session high versus CHF, USD, CAD, JPY, CNH, GBP, and pare some of its losses against the Kiwi and AUD.

- Looking ahead, focus is on speakers, with no tier 1 data to start the week.

- Today includes, ECB de Cos, Holzmann, Nagel, Villeroy, BoE Bailey, and Fed Bostic.

FX OPTION EXPIRY

FX OPTION EXPIRY (Closest ones).

Of note:

EURUSD 1.04bn at 1.0600

USDJPY 2.64bn at 128.00/128.25

AUDNZD 1.87bn at 1.0965- EURUSD: 1.0600 (1.04bn).

- USDJPY: 128 (387mln), 128.15 (220mln), 128.17 (1.72bn), 128.25 (315mln).

- AUDNZD: 1.0965 (1.87bn)

Price Signal Summary - EURUSD Pushes Through Resistance

- In the equity space, S&P E-Minis found resistance last Wednesday at 4095.00. This has left initial key resistance - 4099.00, the May 9 high - intact. The reversal lower, and Friday’s fresh trend low, signals a resumption of the primary downtrend and attention is on 3801.97, 38.2% of the Mar ‘20 - Jan ‘22 bull leg (cont). 3807.50, Friday’s low is the bear trigger. A break of resistance at 4099.00 is required to alter the short-term picture. The primary trend direction in EUROSTOXX 50 futures is down. However, a corrective cycle is still in play following the recovery from 3466.00, May 10 low. Price last week probed resistance at 3728.50, the 50-day EMA. A clear break of this average would improve a short-term bullish theme. On the downside, key support and the bear trigger is unchanged at 3466.00.

- In FX, EURUSD has cleared the 20-day EMA at 1.0570. The break suggests scope for a stronger recovery and note that today’s climb has resulted in a print above 1.0642, May 5 high. The current bull cycle started at 1.0350, May 13 low and, from the base of a bear channel, drawn from the Feb 10 high. The channel top intersects at 1.0857 and is a potential short-term objective. Initial support is at 1.0533, May 20 low. GBPUSD starts the week on a firmer note, trading above last week’s high of 1.2525 and the 20-day EMA at 1.2491. This signals scope for a stronger recovery and opens 1.2638, the May 4 high and a key resistance. Initial firm support lies at 1.2317, the May 17 low. USDJPY traded lower last Thursday. 127.52, the May 12 low has been breached and this exposes the next key support at 126.95, Apr 27 low. The current pullback is likely a correction. A break of 126.95 however would signal scope for an extension towards the 50-day EMA, at 125.77. A reversal higher and a move above 130.05, May 9 high would be bullish.

- On the commodity front, Gold is starting the week on a firmer note. The yellow metal has traded above resistance at $1859.6, the 20-day EMA. This opens the 50-day EMA at $1886.6. The move higher is still considered corrective and the trend direction remains down. A resumption of bearish activity would refocus attention on last week’s $1787.0 low (May 16). In the Oil space, WTI futures maintain a firm tone. The contract last week breached resistance at $110.07, Mar 24 high. A resumption of gains would open $116.43, the Mar 7 trend high. Initial support is at $103.24, the May 19 low.

- In the FI space, Bund futures resistance has been defined at $155.33 May 12 high. The trend direction remains down and an extension lower would open 150.49, the May 9 and the bear trigger. The broader trend condition in Gilts remains down. The contract has found resistance at 121.07, May 12 high. The bear trigger is at 116.87, May 9 low.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/05/2022 | - |  | EU | ECB Lagarde & Panetta at Eurogroup Meeting | |

| 23/05/2022 | 1300/1500 | ** |  | BE | BNB Business Sentiment |

| 23/05/2022 | 1530/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 23/05/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 23/05/2022 | 1600/1200 | | US | Atlanta Fed's Raphael Bostic | |

| 23/05/2022 | 1615/1715 |  | UK | BOE Governor Bailey Panels Discussion | |

| 24/05/2022 | 2300/0900 | *** |  | AU | IHS Markit Flash Australia PMI |

| 23/05/2022 | 2330/1930 | | US | Kansas City Fed's Esther George | |

| 24/05/2022 | 0030/0930 | ** |  | JP | IHS Markit Flash Japan PMI |

| 24/05/2022 | 0600/0700 | *** | | UK | Public Sector Finances |

| 24/05/2022 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 24/05/2022 | 0715/0915 | ** | | FR | IHS Markit Services PMI (p) |

| 24/05/2022 | 0715/0915 | ** | | FR | IHS Markit Manufacturing PMI (p) |

| 24/05/2022 | 0730/0930 | ** |  | DE | IHS Markit Services PMI (p) |

| 24/05/2022 | 0730/0930 | ** | | DE | IHS Markit Manufacturing PMI (p) |

| 24/05/2022 | 0830/0930 | *** | | UK | IHS Markit Manufacturing PMI (flash) |

| 24/05/2022 | 0830/0930 | *** | | UK | IHS Markit Services PMI (flash) |

| 24/05/2022 | 0830/0930 | *** | | UK | IHS Markit Composite PMI (flash) |

| 24/05/2022 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 24/05/2022 | 1000/1100 | ** | | UK | CBI Distributive Trades |

| 24/05/2022 | - | | EU | ECB de Guindos at ECOFIN Meeting | |

| 24/05/2022 | 1230/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 24/05/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 24/05/2022 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 24/05/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (flash) |

| 24/05/2022 | 1400/1000 | *** | | US | New Home Sales |

| 24/05/2022 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 24/05/2022 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

| 24/05/2022 | 1715/1815 | | UK | BOE Tenreyro Panels Discussion |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok