Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- BOE WOULD SELL GILTS EVEN IF IT CUTS RATES IN FUTURE: RAMSDEN (RTRS INTERVIEW)

- CHINA DRILLS SHOW PREPARATION FOR POSSIBLE INVASION, TAIWAN SAYS

- INFLATION OVER 3% NOT ENOUGH FOR BOJ (MNI INSIGHT)

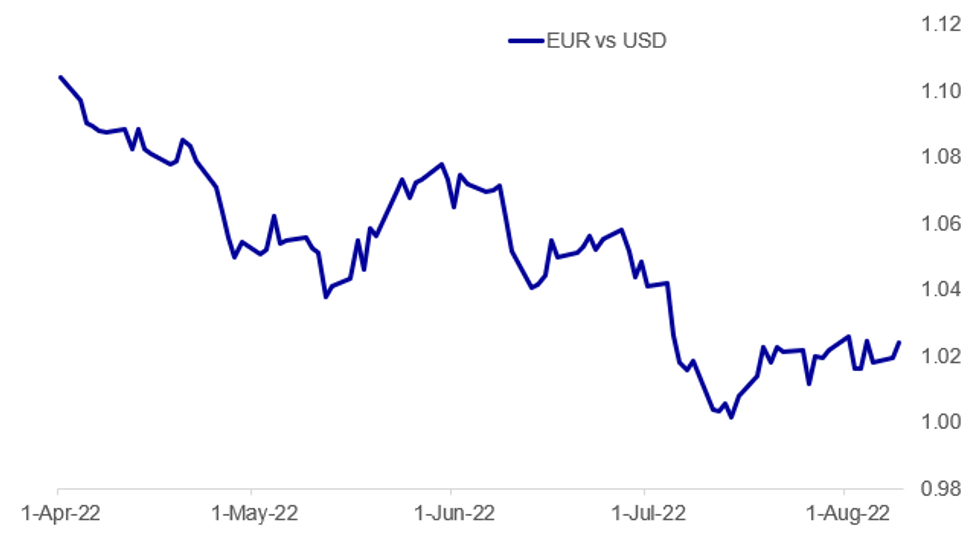

Fig. 1: Euro Outperforms Overnight

Source: BBG, MNI

Source: BBG, MNI

NEWS:

BOE (RTRS): The Bank of England would press on with plans to gradually sell its vast stock of British government bonds even if an economic slowdown eventually forces it to cut interest rates, Deputy Governor Dave Ramsden said. Ramsden, in charge of the BoE's roughly 1 trillion pound balance sheet, told Reuters it was "more likely than not" that borrowing costs would need to rise again after the BoE raised Bank Rate by 50 basis points to 1.75% last week. But, in an interview, he also acknowledged financial market expectations that the recession forecast by the Bank could force it to reverse course on rates next year - a scenario Ramsden said was not his forecast but he was "certainly not ruling out". Even in this situation, the process of selling gilts - or quantitative tightening (QT) - could continue, Ramsden said. "I think that's consistent with the way we communicated things, that we'll carry on with the pace of QT in the background," Ramsden said, speaking in his office at the BoE.

CHINA / TAIWAN (BBG): China used US House Speaker Nancy Pelosi’s visit to Taipei as a pretext to prepare for a possible Taiwan invasion and expand its control throughout the region, the island’s foreign minister said, adding Beijing had been planning the move for some time. China’s recent military drills in the seas and air around Taiwan were aimed at changing the status quo in the Strait, Joseph Wu said at a briefing in Taipei on Tuesday, adding that the activity fueled concern Beijing may proceed with an actual invasion.

BOJ (MNI INSIGHT): The Bank of Japan sees a risk prices will rise more quickly than officials had anticipated at their July meeting, but a jump in inflation to 3% or higher later this year will not be enough to prompt any shift in its easy policy stance unless it feeds into an acceleration of wages next spring, MNI understands.

UK / INFLATION (BBG): Britons booking a break in some of Europe’s most popular holiday destinations this summer are seeing airfares climb by almost a third amid booming demand, high oil prices and curbs on airline capacity. Fares in the first week of August, the peak month for UK travel, were up 30% on average for the top 36 routes compared with pre-pandemic levels, according to data compiled by online travel agency Kayak.

UK (MNI POLITICS): The two hopefuls for the Conservative leadership, Foreign Secretary Liz Truss and former Chancellor Rishi Sunak, face the fifth hustings of the lengthy members voting period in the 'red wall' town of Darlington this evening. Right-winger Truss, who has run a campaign based on cutting taxes swiftly after taking office, remains in the lead in Conservative party member opinion polls and the strong favourite in betting markets. Data from Smarkets shows Truss with a 90% implied probability of winning the contest, to Sunak's 10%. The Darlington hustings takes place 1900-2100BST.

CHINA (BBG): Chinese e-commerce giant Alibaba Group Holding Ltd. let go of 9,241 employees in the three months to June, according to the company’s latest filing. The Hangzhou-based firm reported it had just over 245,000 employees at the end of the most recent reporting quarter, cutting back during a period that marked its first ever contraction in revenue. Alibaba also reduced its workforce in the first three months of the year by 4,375, mirroring widespread moves among global tech companies to rein in spending at a time of rising inflation, materials costs and political tensions.

JAPAN (MNI): Japan's economy grew for the first time in two quarters in the April-June period as private consumption and capital investment recovered, economists predict. Preliminary data at 0850 JST on Aug. 15 (2350 GMT, Aug. 14) should show Q2 GDP higher by 0.7%, or an annualised +2.9%, up from -0.1% q/q or 0.5% y/y in the first quarter of 2022. Forecasts ranged from +0.3% to +0.9% q/q, and from an annualised +1.4% to +3.6%.

DATA:

No key data releases in the European morning session.

FIXED INCOME: Drifting lower

- Core fixed income has drifted lower in European hours, with little in the way of real drivers and seemingly just reversing some of yesterday's moves.

- There is very little on the data calendar today, and the only notable CB contribution has come via a Reuters interview this morning of BOE's Ramsden who said that he hasn't decided what to vote for at the next meeting but that further rate rises were probably needed, although he also acknowledged that Bank Rate could be cut next year, potentially "quite quickly". His comments had little market impact.

- Markets are already looking forward to tomorrow's US CPI print with continued low liquidity.

- TY1 futures are down -0-7+ today at 119-20 with 10y UST yields up 3.3bp at 2.791% and 2y yields up 1.7bp at 3.225%.

- Bund futures are down -0.46 today at 156.25 with 10y Bund yields up 3.3bp at 0.928% and Schatz yields up 3.8bp at 0.476%.

- Gilt futures are down -0.22 today at 117.36 with 10y yields up 2.2bp at 1.972% and 2y yields up 1.2bp at 1.868%.

FOREX: Greenback Fades Amid Light Market Participation

- The greenback trades lower in early Tuesday trade, putting EUR/USD north of 1.02 to reverse the entirety of the post-payrolls rally. This makes the USD the worst performing currency in G10, and comes despite a small uptick in the US 10y yield (higher by 3bps to 2.79% this morning) and rangebound trade in equities.

- Volumes and market activity are distinctly light across currency, equity and fixed income futures, suggesting that traders may be sitting on their hands ahead of the CPI release tomorrow.

- Outside of the greenback move, G10 currencies are quieter, with EUR benefiting from greenback weakness while GBP/USD narrows in on the Monday high at 1.2138 and GBP/JPY eyes 163.92 ahead of the 164.31 50-dma.

- NOK/SEK has staged a solid bounce off the Monday lows, extending the bounce to near 2% off the week's worst levels. Strength through 1.0462 opens the late July highs at 1.0576.

- The data slate is light Tuesday, with no tier 1 releases from across the US or Canada. Some attention may be paid to the nonfarm productivity and unit labor costs data, but focus still rests on tomorrow's inflation prints from China and the US.

EQUITIES: Energy Names Lead In Mixed Trade

- Asian markets closed mixed: Japan's NIKKEI closed down 249.28 pts or -0.88% at 27999.96 and the TOPIX ended 14.39 pts lower or -0.74% at 1937.02. China's SHANGHAI closed up 10.498 pts or +0.32% at 3247.432 and the HANG SENG ended 42.33 pts lower or -0.21% at 20003.44.

- European bourses are trading mostly weaker, with cyclical stocks (Tech, Materials) dragging and Energy / Financials in the green: the German Dax down 61.63 pts or -0.45% at 13632.63, FTSE 100 up 6.86 pts or +0.09% at 7470.07, CAC 40 up 2.86 pts or +0.04% at 6514.34 and Euro Stoxx 50 down 11.99 pts or -0.32% at 3748.87.

- U.S. futures are very slightly higher, with the Dow Jones mini up 48 pts or +0.15% at 32840, S&P 500 mini up 5.75 pts or +0.14% at 4147.5, NASDAQ mini up 9.25 pts or +0.07% at 13192.5.

COMMODITIES: WTI Dips Back Below $90

- WTI Crude down $1.15 or -1.27% at $89.69

- Natural Gas up $0.1 or +1.28% at $7.685

- Gold spot up $2.66 or +0.15% at $1773.38

- Copper up $1.85 or +0.52% at $360.35

- Silver down $0.03 or -0.15% at $20.6492

- Platinum down $3.07 or -0.33% at $946.26

LOOK AHEAD:

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/08/2022 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 09/08/2022 | 1230/0830 | ** | | US | Preliminary Non-Farm Productivity |

| 09/08/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 09/08/2022 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 09/08/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 09/08/2022 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

| 10/08/2022 | 0600/0800 | * |  | NO | CPI Norway |

| 10/08/2022 | 0600/0800 | *** |  | DE | HICP (f) |

| 10/08/2022 | 0800/1000 | ** |  | IT | Italy Final HICP |

| 10/08/2022 | 1100/0700 | ** | | US | MBA Weekly Applications Index |

| 10/08/2022 | 1230/0830 | *** | | US | CPI |

| 10/08/2022 | 1400/1000 | ** | | US | Wholesale Trade |

| 10/08/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 10/08/2022 | 1500/1100 | | US | Chicago Fed's Charles Evans | |

| 10/08/2022 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 10/08/2022 | 1800/1400 | ** | | US | Treasury Budget |

| 10/08/2022 | 1800/1400 | | US | Minneapolis Fed's Neel Kashkari |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.