Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- SPAIN PMI SURPRISES TO UPSIDE, MANUFACTURERS MORE OPTIMISTIC ABOUT COVID

- OIL HITS FIVE-MONTH LOW ON SUPPLY, LOCKDOWN CONCERNS

Fig.1: Spain PMI Surprises To The Upside

Markit, MNI

Markit, MNI

NEWS:

SPAIN DATA: Interesting from Spain PMI press release, looks as though firms looking through short-term case rises "expectations for output over the coming 12 months strengthened in October, with confidence reaching its highest level since February. Positive sentiment was linked to hopes that COVID-19 will have been brought fully under control by this time next year, and that a strong economic recovery will be under way. "

EUROZONE DATA (IHS MARKIT): The IHS Markit Eurozone Manufacturing PMI® indicated a further improvement in manufacturing sector growth during October. After accounting for seasonal factors, the headline index moved up to 54.8, from 53.7 in September and better than the earlier flash reading. October's number was also the best recorded by the survey for 27 months and maintained the current run of continuous growth that began in July.

UK DATA (IHS MARKIT): The recovery in the UK manufacturing sector continued at the start of the final quarter, as output and new orders rose again supported by improved demand from both domestic and overseas sources. That said, the upturn showed further signs of losing impetus, as the initial boost to growth from the economy reopening faded and job losses accelerated.The seasonally adjusted IHS Markit/CIPS Purchasing Managers' Index® (PMI®) fell to 53.7 in October, down from54.1 in September but above the earlier flash estimate of53.3. The PMI has remained at an above-50.0 level, signalling expansion, for five months running.

OIL (BBG): Oil kicked off what promises to be a turbulent week of trading by plunging to a five-month low as a continued increase in Libyan crude production coincided with a wave of new virus-lockdown measures in Europe. The double whammy of falling demand and growing supply pushed futures in New York down as much as 6% in Asian trading. That could be just the curtain raiser for price action as Americans head to the polls on Tuesday in an election set to have far-reaching consequences for battered financial markets.

CHINA: China will need another five years of fiscal stimulus to overcome the hit from the Covid-19 pandemic to global trade, a high-ranking advisor to fiscal authorities told MNI in an interview in which he also said the government may consider new taxes on booming digital industries and should shoulder a greater share of the spending burden rather than relying on heavily-indebted local administrations. For full article contact sales@marketnews.com

CFTC: CoT Data Shows Markets Favoured MXN, Dropped GBP in Most Recent Week

Friday's CFTC CoT update shows speculators built MXN & trimmed GBP positions in the latest week of data. MXN saw the most sizeable change, with markets adding a net of 8k contracts,representing a 6.3 percentage point swing higher in the net long. GBP positions moved in the opposite direction, with GBP now at a near 7k netshort position as speculators trimmed positions by close to 5k contracts. Both NZD and CHF net positions remain close to their 52w highs at 17.3% and29.4% of open interest respectively.

EQUITIES (BBG): Institutional investors are buying Ant Group Co.'s Hong Kong shares before this week's debut at a premium to the listing price.Some trades were executed for HK$120 apiece in gray-market trading Monday, according to people familiar with the matter. That's 50% higher than the listing price of HK$80. The people declined to be identified as they are not authorized to speak to the media.

DATA:

MNI: EZ FINAL OCT MFG PMI 54.8; FLASH 54.4; SEP 53.7

MNI: ITALY OCT MFG PMI 53.8; SEP 53.2

MNI: SPAIN OCT MFG PMI 52.5; SEP 50.8

MNI: FRANCE FINAL OCT MFG PMI 51.3; FLASH 51.0; SEP 51.2

MNI: GERMANY FINAL OCT MFG PMI 58.2; FLASH 58.0; SEP 56.4

MNI: UK FINAL OCT MFG PMI 53.7; FLASH 53.3; SEP 54.1

FIXED INCOME: Mixed start to big week

It's a blockbuster week with the US election as well as FOMC and BOE MPC policy decisions.

- The week has started on a mixed note with Treasuries and Bunds lower as risk appetite recovers somewhat but gilts have moved higher after the UK lockdown was announced over the weekend (and had been less telegraphed ahead of the market close on Friday than the lockdowns that had already been announced around the Eurozone).

- PMIs this morning have helped sentiment with some small upside surprises and with firms sounding fairly optimistic about the year-ahead outlook despite increasing Covid-19 cases near-term.

- TY1 futures are flat today at 138-07 with 10y UST yields down -1.0bp at 0.865% and 2y yields down -0.2bp at 0.153%.

- Bund futures are down -0.16 today at 175.99 with 10y Bund yields up 1.0bp at -0.618% and Schatz yields unch at -0.798%.

- Gilt futures are up 0.13 today at 135.81 with 10y yields down -1.4bp at 0.246% and 2y yields down -1.7bp at -0.55%.

FOREX: Equities on Firmer Footing in Election Week

Equities trade on a more solid footing early Monday. Stock markets in Europe are higher by 0.8-1.5% while the E-mini S&P is higher by 40 points or so. Currencies are broadly non-directional, with the USD index inside last week's range, although the haven JPY is a touch weaker. CAD, NZD outperform slightly.

GBP was softer from the off, with the currency underperforming all others in G10 at the NY crossover following the announcement of a month-long lockdown effective Thursday to run until the beginning of December. While the move mimics others seen in France & Germany, Monday's GBP moves clearly show a lockdown wasn't seen as a done deal in the UK. GBP/USD bottomed out at 1.2855 this morning, the lowest since October 7th.

October Manufacturing ISM data as well as Construction spending cross, but broader focus remains on the coming US election, Fed rate decision and Friday's NFP release.

EQUITIES: Futures Higher As Busy Week Underway

A strong start to a busy week for equities, with 'work from home' sectors outperforming in the wake of COVID lockdowns spreading.

- Asian stocks closed higher, with Japan's NIKKEI up 318.35 pts or +1.39% at 23295.48 and the TOPIX up 28.62 pts or +1.81% at 1607.95. China's SHANGHAI closed up 0.588 pts or +0.02% at 3225.12 and the HANG SENG ended 352.59 pts higher or +1.46% at 24460.01.

- European equities are higher, with the German Dax up 193.66 pts or +1.68% at 11610.29, FTSE 100 up 39.84 pts or +0.71% at 5568.36, CAC 40 up 57.68 pts or +1.26% at 4586.05 and Euro Stoxx 50 up 46.44 pts or +1.57% at 2958.21.

- U.S. futures are up, with the Dow Jones mini up 367 pts or +1.39% at 26761, S&P 500 mini up 40.75 pts or +1.25% at 3305.5, NASDAQ mini up 126.25 pts or +1.14% at 11172.5.

COMMODITIES: Oil Hits 5-Month Lows

Oil continues to fall, underperforming on both supply and demand concerns.

- WTI Crude down $0.87 or -2.43% at $34.55

- Natural Gas down $0.07 or -1.97% at $3.315

- Gold spot up $8.73 or +0.46% at $1883.39

- Copper up $0.55 or +0.18% at $304.25

- Silver up $0.37 or +1.57% at $23.8669

- Platinum up $10.09 or +1.19% at $854.79

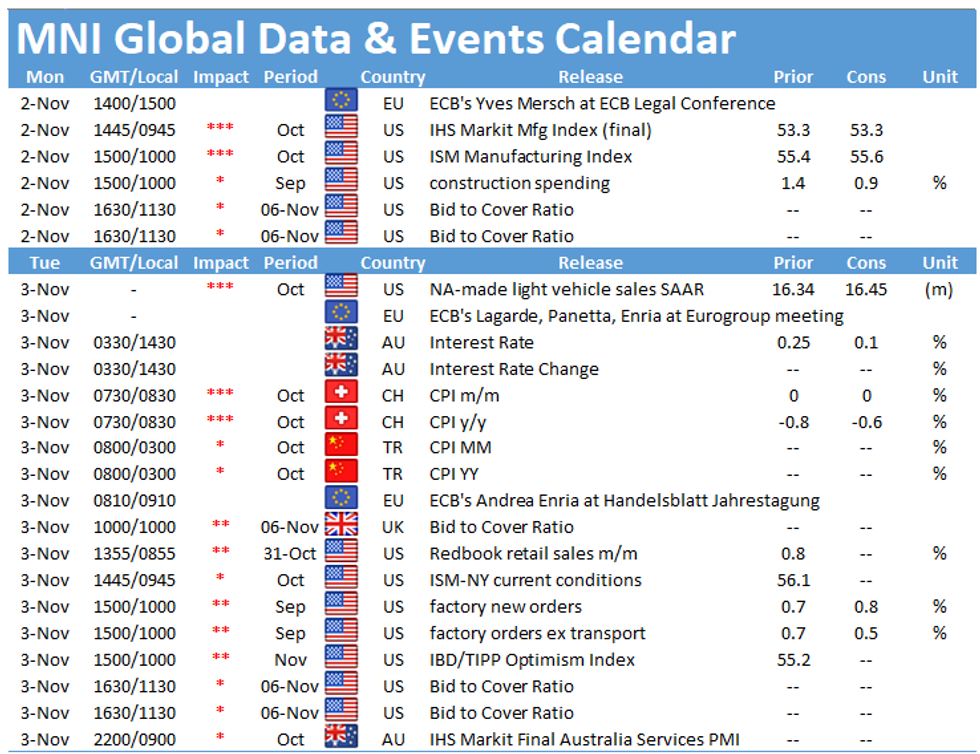

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.