Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- GERMAN IFO BUSINESS CLIMATE UP, BUT OUTLOOK DIPS

- BUSIEST WEEK OF THE QUARTER FOR U.S. CORPORATE EARNINGS

- TOO SOON FOR SWEDISH RIKSBANK TO SIGNAL TIGHTENING (MNI STATE OF PLAY / MNI MARKETS PREVIEW)

- CHINA WIDENS INTERNET CRACKDOWN WITH MEITUAN MONOPOLY PROBE

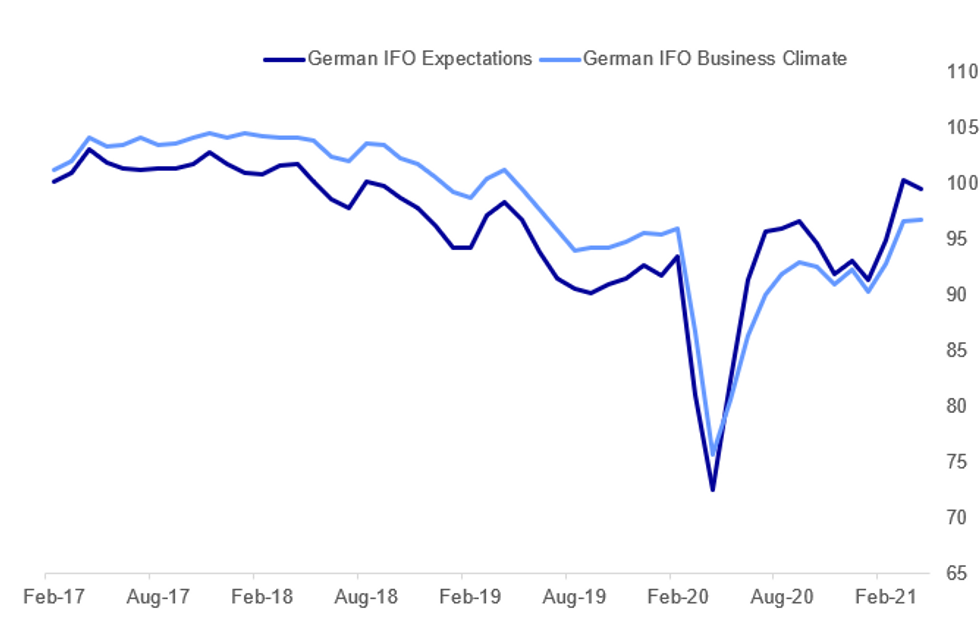

Fig. 1: German Investor Sentiment Stalls

IFO, MNI

IFO, MNI

NEWS:

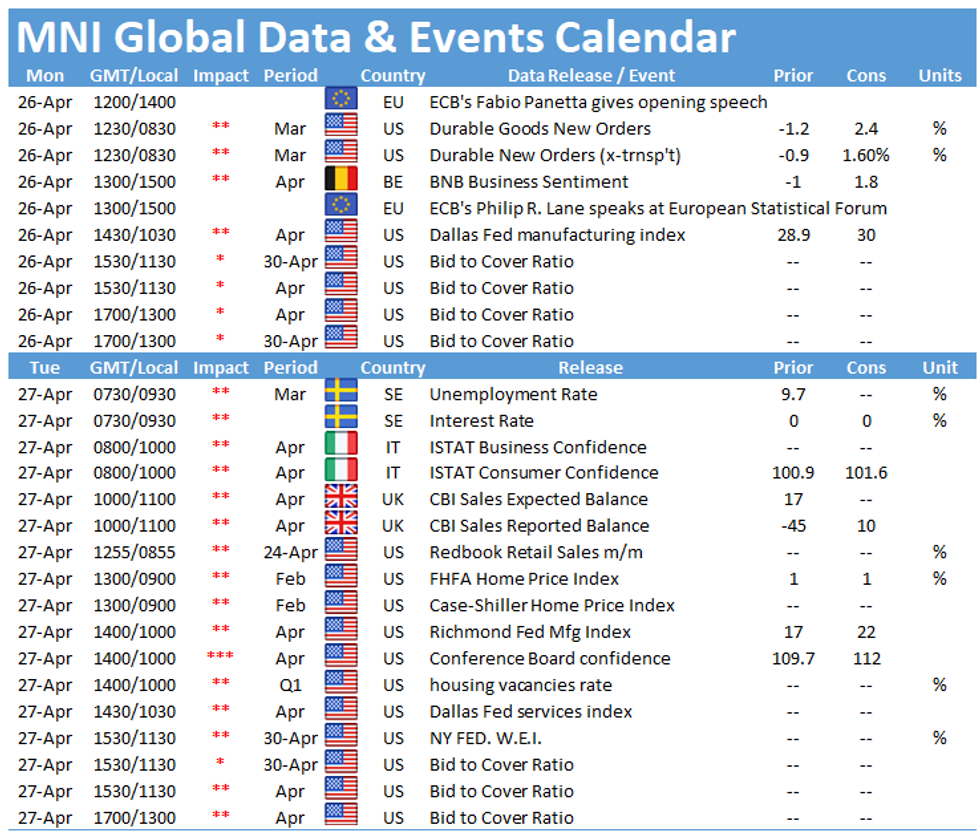

U.S. CORPORATE EARNINGS: In comfortably the busiest week for earnings of the quarter, close to half of the S&P 500 by market cap are due to report. Four trillion dollars are due, with Amazon, Microsoft, Apple and Alphabet all due to report. This keeps focus on the tech and consumer discretionary sectors for the coming week. Tuesday is the busiest session for the index. Link here to full MNI report

GERMAN IFO: German business confidence rose in April, as assessments of the current business situation improved, but optimism over the coming six months eased, as "the third wave of infections and bottlenecks in intermediate products are impeding Germany's economic recovery," the Ifo Institute said Monday. Manufacturing sentiment rose to the highest level since May 2018 with firm's opinion about the current situation improving markedly. While capacity utilization increased above the long-term average for the first time in 2 years, optimism decreased as "45% of companies reported bottlenecks in intermediate products – the highest value since 1991." Business climate in the construction sector dipped as many firms reported material shortages. Service sector business climate eased in April, as industries such as hospitality and tourism are still suffering. Meanwhile, business sentiment in trade ticked up slightly, despite a fall in optimism. The Ifo business climate indicator edged up in April to 96.8, although falling short of market expectations looking for an uptick to 101.0. Current conditions rose 1pt to 94.1, while the Ifo Expectations index ticked down 0.8pt to 99.5, in contrast to markets projecting an increase.

RIKSBANK (MNI STATE OF PLAY): The Riksbank may slightly boost forecasts for growth and inflation in its quarterly Monetary Policy Report on Tuesday, but policymakers are likely to leave their collective rate forecast flat at the current 0% over the next three years, judging it too soon to start signalling future tightening after a prolonged inflation undershoot. For full article contact sales@marketnews.com

RIKSBANK (MNI MARKETS PREVIEW):Three questions to ponder: Will asset purchases be front-loaded again in Q3?- Will the repo rate path be flat?- Will CPIF move above 2.00% in the forecasts? We look at these 3 questions in our full preview alongside summaries of 13 sell-side views and a roundup of key comments from Executive Board members since the last meeting. http://enews.marketnews.com/ct/uz10098501Biz48303521

U.K.: The main opposition Labour Party has requested an Urgent Question for Cabinet Office Secretary Michael Gove relating to the Ministerial Code, which is likely set to be used as an opportunity to seek answers regarding the ongoing leaking scandal that has hit No.10 Downing Street. UQ due at 1535BST. PM Boris Johnson is under pressure on a number of fronts due to the leaks, most pressingly when he allegedly told Cabinet colleagues to "let the bodies pile high in their thousands", rather than go into another COVID-19 lockdown.

CHINA (BBG): China's government has expanded its antitrust crackdown beyond Jack Ma's technology empire, launching an investigation into suspected monopolistic practices by food-delivery behemoth Meituan. The State Administration for Market Regulation announced the investigation, which began recently, in a statement Monday. The antitrust watchdog is looking into alleged abuses including forced exclusivity arrangements known as "pick one of two." The company said it will actively cooperate with the probe and step up efforts to comply with regulations. Operations are currently normal, it added in a statement.

ITALY / EU (BBG): Prime Minister Mario Draghi goes to Parliament on Monday to present details of his 235 billion-euro ($284 billion) plan to re-engineer Italy's economy that will be a test of the European Union's post-pandemic recovery fund.Draghi's plan taps 191.5 billion euros in EU grants and loans plus 30 billion euros in domestic funding and other small amounts of separate EU funds. The premier estimates the investment will boost gross domestic product by at least 3.6%. He is seeking parliamentary backing ahead of an April 30 deadline to submit the plan to the European Commission.

BANKS (BBG): European lenders are about to show investors if they can ride the pandemic-induced wave of investment banking revenue that propelled U.S. peers to a record quarter.While Credit Suisse Group AG kicked off Europe's bank earnings season on Thursday, its gains in trading and advising on deals were a sideshow given blow-ups related to Greensill Capital and Archegos Capital Management. This week, four of the biggest securities firms are up.The focus will be on Deutsche Bank AG's ongoing efforts to regain market share in debt trading, UBS Group AG's performance in wealth management and Barclays Plc's ability to bolster earnings by releasing reserves for bad loans.

DATA:

FIXED INCOME: Off To A Weak Start

Sovereign bonds broadly opened lower and have remained offered through the first half of the morning session alongside modest gains for equities.

- The UST curve has bear steepened with the 2s30s spread 2bp wider on the day. TYM1 trades at 132-10, near the middle of the morning range (L: 132-07+ / 132-15).

- Gilts have similarly traded lower with cash yields 1-2bp higher and the short/belly marginally underperforming.

- Bunds opened lower but soon recovered losses, while still trading marginally below the Friday close.

- BTPs remain under some pressure with long-end yields 4bp higher and printing fresh highs for the morning.

- UK PM Boris Johnson has come under increasing pressure over the weekend as his former chief advisor Dominic Cummings alleges that he was willing to accept a higher death toll rather than another lockdown. This comes on top of ongoing criticism over private sector lobbying of the government.

- The German IFO survey for April came in slightly below consensus with the expectations component reading 99.5 vs 101.2 expected.

FOREX: AUD, NZD Buoyed While Copper Strikes Decade High

- Antipodean currencies outperform early Monday, with AUD/USD, NZD/USD nearing last week's best levels as commodity markets - particularly industrial metals - trade well at the start of the week. Copper prices have hit new cycle highs this morning, trading again at the best levels in a decade having cleared the previous top in late February.

- The greenback trades marginally lower, with the USD slipping against most others. This has helped buoy EUR/USD, which continues to defy the bearish signals emanating from last week's gravestone doji candle (Tuesday). Instead, the EUR/USD uptrend remains in tact and is approaching bear channel resistance at 1.2119.

- GBP trades modestly firmer, erasing some of the damage done at the tail-end of last week. Lower crude prices are working against the likes of NOK ahead of this Wednesday's OPEC+ meeting.

- Preliminary US durable goods numbers cross later today, with speeches from ECB's Lane and Panetta also due.

EQUITIES: Tech Lagging To Start The Week

- Asian stocks closed the session mixed, with Japan's NIKKEI down 29020.63 pts or +0.36% at 29126.23 and the TOPIX up 3.17 pts or +0.17% at 1918.15. China's SHANGHAI closed down 33 pts or -0.95% at 3441.166 and the HANG SENG ended 125.92 pts lower or -0.43% at 28952.83.

- European equities are mixed/flat, with the German Dax down 1.79 pts or -0.01% at 15275.5, FTSE 100 up 1.74 pts or +0.03% at 6938.85, CAC 40 up 6.87 pts or +0.11% at 6265.98 and Euro Stoxx 50 up 0.4 pts or +0.01% at 4013.28.

- U.S. futures are flat/lower, with the Dow Jones mini up 8 pts or +0.02% at 33949, S&P 500 mini down 4.5 pts or -0.11% at 4167, NASDAQ mini down 43.25 pts or -0.31% at 13883.75.

COMMODITIES: Oil And Copper Go In Opposite Directions

- WTI Crude down $1.07 or -1.72% at $61.15

- Natural Gas down $0.01 or -0.37% at $2.719

- Gold spot up $3.29 or +0.19% at $1779.41

- Copper up $6.85 or +1.58% at $440.95

- Silver up $0.04 or +0.14% at $26.023

- Platinum up $7.07 or +0.57% at $1237.61

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.