Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- BANK OF ENGLAND DECISION EYED AT 0800ET/1200GMT

- ITALY SERVICES PMI MISSES EXPECTATIONS; SPAIN BEATS SLIGHTLY

- NORGES BANK SIGNALS STILL ON TRACK FOR DEC HIKE

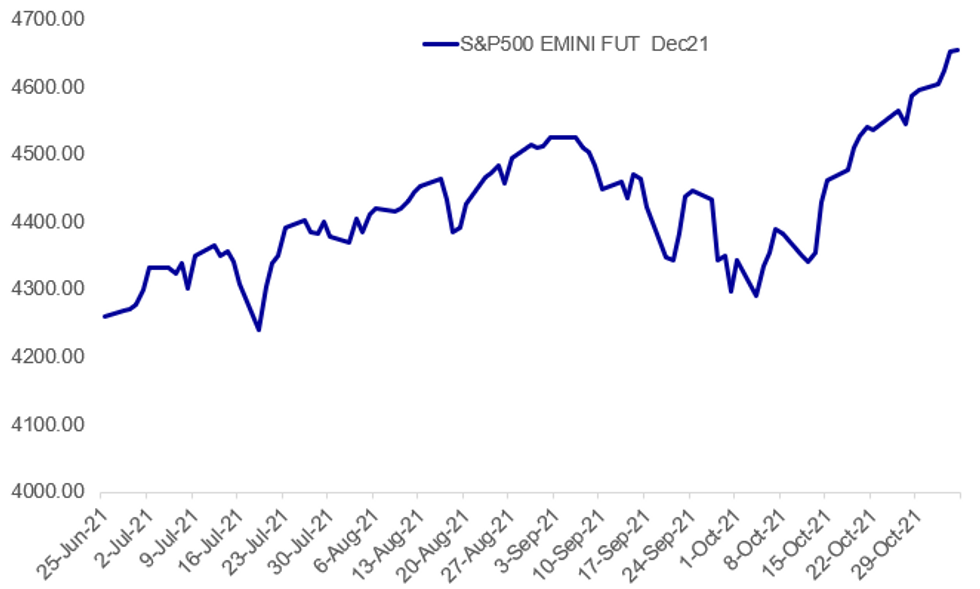

Fig. 1: Stocks At Fresh Highs Post-Fed, Pre-BoE

Source: BBG

Source: BBG

NEWS:

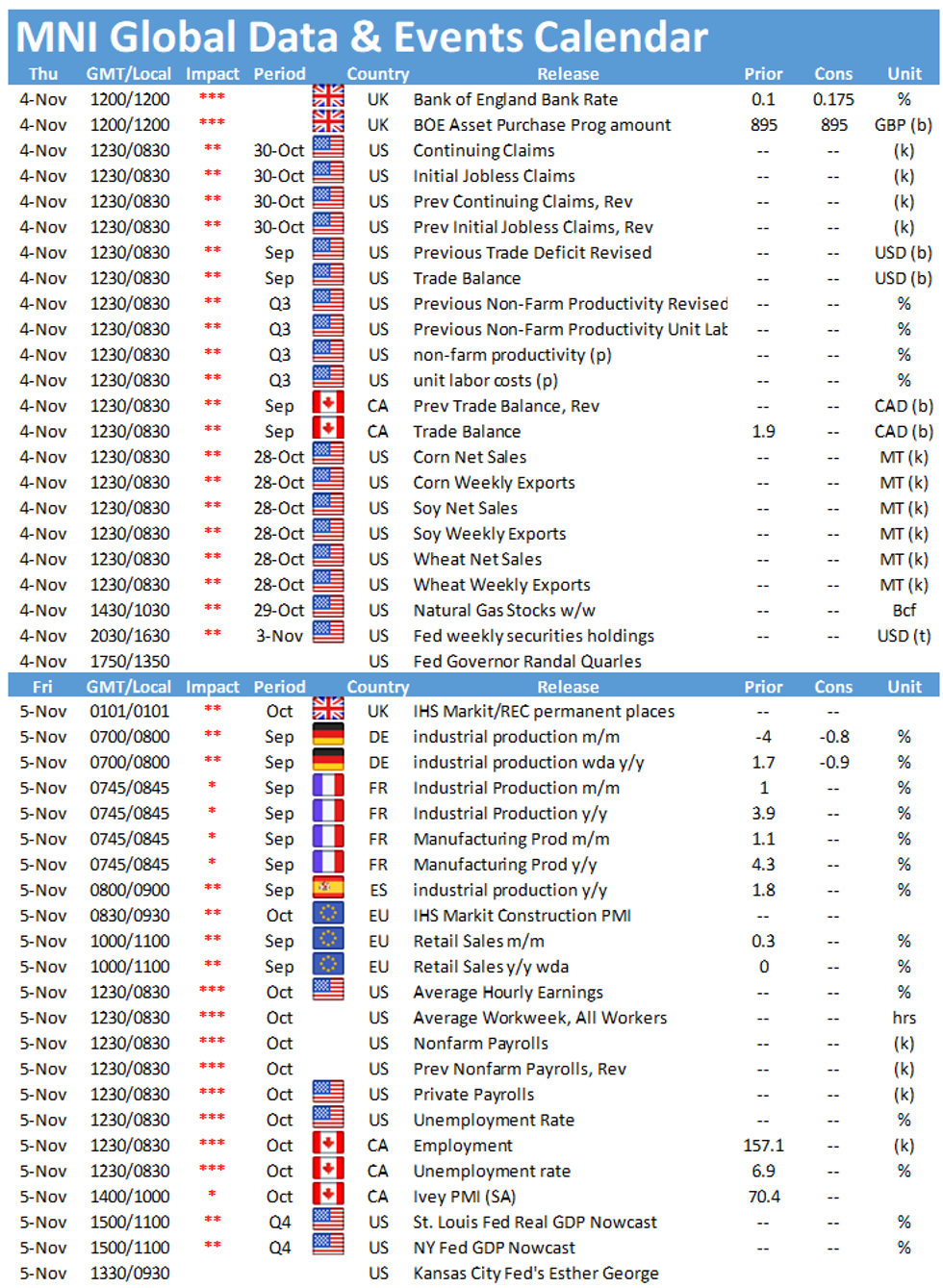

BANK OF ENGLAND DECISION (MNI): The MNI Instant Answers will be the easiest way to quickly digest the key points from the BOE meeting (with the decision due at 12:00GMT and a press conference at 12:30GMT). The key questions:

- Hike or not?

- End QE early?

- Inflation forecasts at 2/3-year horizons

- The answers to all of these will be in the MNI Instant Answers, communicated via Bullets and our Bloomberg chat service at 12:00GMT.

DATA:

*ITALY OCT. COMPOSITE PMI FALLS TO 54.2; FORECAST 55.6*ITALY OCT. SERVICES PMI FALLS TO 52.4; FORECAST 54.5 -bbg

*SPAIN OCT. COMPOSITE PMI FALLS TO 56.2; FORECAST 56*SPAIN OCT. SERVICES PMI FALLS TO 56.6; FORECAST 55.8 -bbg

FIXED INCOME: Fed Done, BOE Upcoming

Bonds have moved higher this morning, but remain off yesterday's highs. The FOMC tapering announcement yesterday was in line with expectations but Powell was fairly dovish, stating that the Fed wouldn't know until at least mid-2022 if the economy was strong enough for a hike (a slower lift off than markets price). Lagarde has also been pushing back against 2022 ECB hikes. However, the moves higher seem to coincide with the gilt open at 8:00GMT so suggest there could be some late positioning ahead of today's BOE meeting.

- Markets price a 15bp hike from the BOE today and then rates at 1.25% by the end of next year. As we have discussed in our BOE preview, we think there will be a 15bp hike on balance but would prefer the Bank waited until December. The decision will be at 12:00GMT with the press conference at 12:30GMT.

- TY1 futures are up 0-1 today at 130-25+ with 10y UST yields down -2.7bp at 1.578% and 2y yields down -0.8bp at 0.461%.

- Bund futures are up 0.20 today at 169.54 with 10y Bund yields down -1.5bp at -0.185% and Schatz yields down -2.5bp at -0.718%.

- Gilt futures are up 0.31 today at 125.11 with 10y yields down -3.3bp at 1.038% and 2y yields down -3.2bp at 0.655%.

FOREX: ALL EYES on the BoE

- USD is mainly better bid during our morning European session.

- EURUSD touches session low, USD remains fairly bid in G10s, DXY edges towards best levels.

- USD leads against the EUR up 0.47%.Recall, noted yesterday decent option expiry at 1.1550 (1.1bn), which may act as a magnet.

- Technically support is seen at 1.1535, but better is seen at 1.1524.

- Recall that good demand ahead of 1.1500 was seen last Month and this month, in spot as well as expressed via option put sellers.

- The last time we traded below 1.1500 was over a year ago in July 2020.

- The British Pound is so far mixed, down 0.41% versus the USD and up a small 0.12% versus the NOK.

- ALL EYES are on the BoE, Economists are going for no hike as per Bloomberg survey.

- Banks/Traders majority (64% from our internal survey) are going for a hike of 15bps and above.

- And from all the UK Banks, only Lloyds is going for a hike.

- Today, also sees OPEC+ meeting which will be watch given inflation risks from energy prices

EQUITIES: Still Gaining Post-Fed, Pre-BoE

- Asian markets closed higher, with Japan's NIKKEI up 273.47 pts or +0.93% at 29794.37 and the TOPIX up 23.89 pts or +1.18% at 2055.56. China's SHANGHAI closed up 28.329 pts or +0.81% at 3526.866 and the HANG SENG ended 200.44 pts higher or +0.8% at 25225.19

- European stocks are higher, with the German Dax up 45.9 pts or +0.29% at 16008.6, FTSE 100 up 19.04 pts or +0.26% at 7268.52, CAC 40 up 27.18 pts or +0.39% at 6984.18 and Euro Stoxx 50 up 16.55 pts or +0.38% at 4329.58.

- U.S. futures are gaining, with the Dow Jones mini down 19 pts or -0.05% at 36015, S&P 500 mini up 4.25 pts or +0.09% at 4656.5, NASDAQ mini up 70 pts or +0.43% at 16199.75.

COMMODITIES: Broad Gains Despite Sharp Dollar Rise

- WTI Crude up $0.17 or +0.21% at $81.14

- Natural Gas up $0 or +0.07% at $5.68

- Gold spot up $7.07 or +0.4% at $1774.8

- Copper up $1.9 or +0.44% at $433.1

- Silver up $0.11 or +0.46% at $23.5845

- Platinum up $16.74 or +1.62% at $1047.54

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.