Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- RUSSIA WARNS U.S. ON WARSHIPS; NATO SEC-GEN SAYS RUSSIA MUST WITHDRAW FROM UKRAINE BORDER

- CHINA WARNS 34 TECH FIRMS TO CURB EXCESS IN ANTITRUST REVIEW

- U.K. FEB GDP UP, TRADE SEES MODEST RECOVERY

- BITCOIN RALLIES TO ALL-TIME HIGH AS TRADERS EYE COINBASE LISTING

- GERMAN ZEW INVESTMENT SENTIMENT UNEXPECTEDLY FALLS IN APRIL

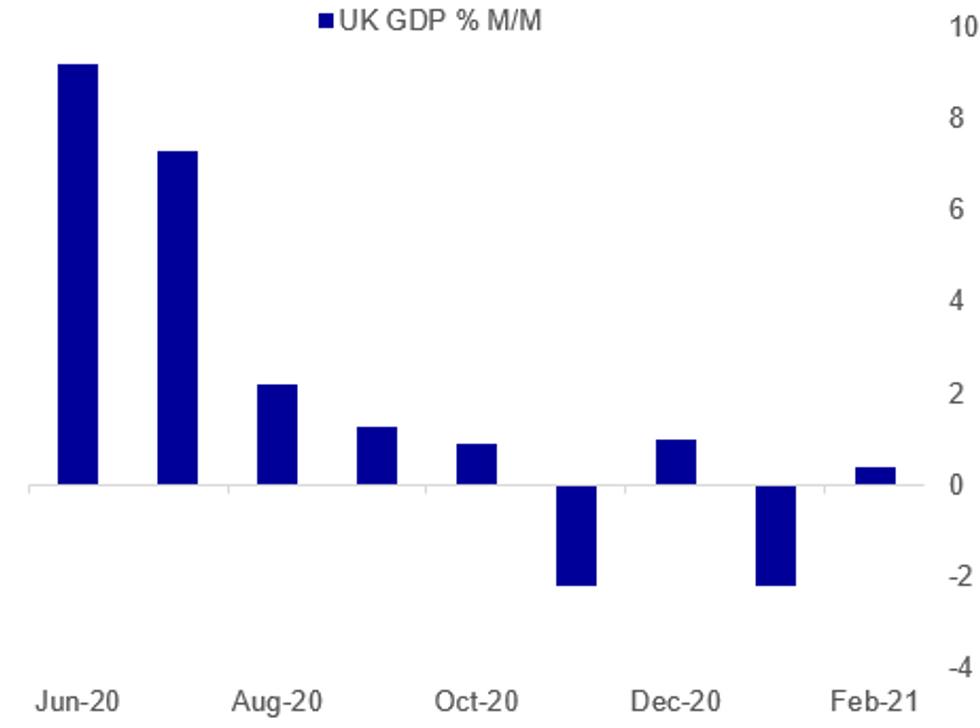

Fig. 1: Slow Grind For UK Activity

ONS, MNI

ONS, MNI

NEWS:

RUSSIA/UKRAINE/U.S. (RTRS): Russia on Tuesday warned the United States to ensure its warships stayed well away from Crimea "for their own good", calling their deployment in the Black Sea a provocation designed to test Russian nerves. Moscow annexed Crimea from Ukraine in 2014 and two U.S. warships are due to arrive in the Black Sea this week amid an escalation in fighting in eastern Ukraine where government forces have battled Russian-backed troops in a conflict Kyiv says has killed 14,000 people. Russian Deputy Foreign Minister Sergei Ryabkov was cited by Russian news agencies on Tuesday as warning U.S. warships in the Black Sea to keep their distance, saying the risk of unspecified incidents was very high. "There is absolutely nothing for American ships to be doing near our shores, this is purely a provocative action. Provocative in the direct sense of the word: they are testing our strength, playing on our nerves. They will not succeed," Ryabkov was cited as saying. "We warn the United States that it will be better for them to stay far away from Crimea and our Black Sea coast. It will be for their own good."

RUSSIA/UKRAINE/NATO: Speaking alongside Ukraine's Foreign Minister Dmytro Kuleba in Brussels, NATO's Secretary-General Jens Stoltenberg states that Russian military forces massing along the Ukrainian border 'must withdraw'.

- The US Secretaries of State and of Defense are both in Brussels today to meet with Stoltenberg. One of the major sticking points on the US' role in Ukraine is whether the Pentagon begins to provide US-made arms to Ukrainian forces.

- The Ukrainian presidency says that there are an estimated 40k Russian troops massed along the Ukrainian border, with an additional 40k in Crimea.

- Last week, MNI's Political Risk team produced an article examining the ongoing crisis.

CHINA / TECH (BBG): China ordered 34 internet corporations Tuesday to rectify their anti-competitive practices within the next month, signaling that Beijing's scrutiny of its most powerful firms hasn't ended with the conclusion of a probe into Alibaba Group Holding Ltd. Shares in Tencent Holdings Ltd. and Meituan extended losses after the State Administration for Market Regulation issued a stern statement emphasizing it will continue to eradicate abuses of information and market dominance among other violations. Also summoned to an ad-hoc meeting with the watchdog on Tuesday were industry leaders including TikTok owner ByteDance Ltd., search giant Baidu Inc. and JD.com Inc.

BITCOIN (BBG): Bitcoin jumped to an all-time high as the mood in cryptocurrencies turned bullish before Coinbase Global Inc. goes public.The token rose as much as 4.3% to $62,531, exceeding the previous peak in March.Crypto bulls are out in force as growing list of companies embrace Bitcoin, even as skeptics doubt the durability of the boom. In one of the most potent signs of Wall Street's growing acceptance of cryptocurrencies, Coinbase will list on the Nasdaq on April 14 at a valuation of about $100 billion.

US/CHINA: The U.S. Presidential Envoy for Climate John Kerry will likely meet with Chinese counterpart Xie Zhenhua in Shanghai as soon as Wednesday, two sources have told MNI. China's top diplomat Yang Jiechi and Foreign Minister Wang Yi will also likely attend the meeting, one of the sources added.

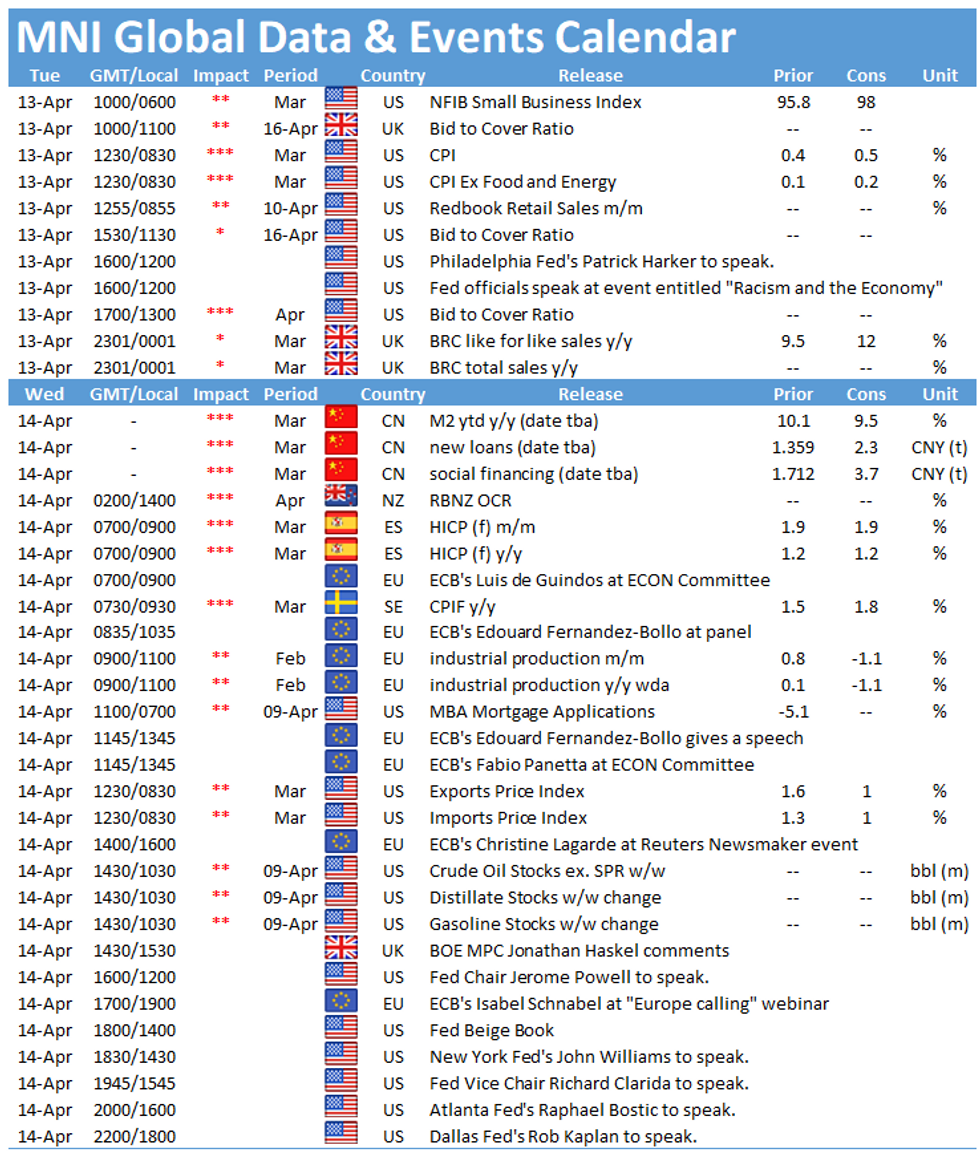

DATA:

MNI DATA IMPACT: UK Feb GDP Up, Trade Sees Modest Recovery

The UK economy expanded modestly in February, while trade with the European Union made up some, but not all, of the extraordinary losses suffered in January, according to the gross domestic product and trade reports released on Tuesday by the Office for National Statistics.

GDP rose by 0.4% between January and February, falling just a bit short of the expected 0.5%, leaving GDP 7.8% below its level a year ago. GDP stands 3.1% the level of October, which marked the peak of the recovery before much of the country headed into an economic lockdown in November.

Services rose by a paltry 0.2% in February, well below the forecast 0.6% increase, contributing 0.17 percentage point to total growth. Services remain 8.8% below the level of February last year. Within services, wholesale and retail trade rose by 3.3%, following an 8.3% plunge in January, lifted by a pick-up in the trade of motor vehicles, according to a statistician. Accommodation and food services increased by 2.6%, but that reflected the application of seasonal factors, as turnover was little changed from January, according to a statistician.

Industrial production rose 1.0% in February, falling by 3.5% over the same month of last year. Manufacturing increased by 1.3%, but declined by 4.2% over February 2020. Construction increased by 1.6%, falling by 4.3% over last February.

January GDP was revised upward, showing a decline of 2.2%, versus the initially-reported 2.9% decline. Services accounted for much of the upward revision. That means GDP must rise by 6.4% in March for first quarter GDP to match the level of the final three months of 2020. GDP growth exceeded that margin in June and July of last year, as much of the country emerged from the first economic lockdown.

TRADE

EU trade made up some of the ground lost in February, when Brexit-related friction contributed to a sharp fall in both imports and exports. EU exports rebounded by 46.6%, while imports increased by 7.3%. That leaves exports down by 15.1% since the end of 2020, while imports are down 24.5%.

The headline total trade deficit increased to GBP7.123 billion in February from GBP3.370 billion in the first month of the year (initially reported was a shortfall of GBP1.630 billion). The goods trade deficit increased to GBP16.442 billion from GBP12.592 billion. Excluding trade in precious metals (including non-monetary gold), the total trade deficit increase to GBP1.388 billion from GBP845 million in January.

Italian Industrial Production Up in Feb

- Feb SA ind. output +0.6% m/m (Jan revised up +1.1% m/m), WDA -0.6% y/y

- Feb data registered slightly below market expectations looking for a 0.7%-uptick

- Feb SA ind. output m/m ticks up third consecutive month--ISTAT says

- Feb SA m/m consumer goods rose; intermed. capital gds, energy fell—ISTAT SAYS

- Feb WDA y/y consumer, capital gds, energy fell--ISTAT SAYS

- Feb WDA y/y intermediate goods tick up +2.1%

- There were 20 working days in Feb 2021 vs. 20in Feb 2020.

ZEW Expectations Sentiment Fell in April

GERMANY APR ZEW ECONOMIC SENTIMENT +70.7; MAR +76.6

GERMANY APR CURRENT CONDITIONS -48.8; MAR -61.0

- ZEW Expectations fell by 5.9pt to 70.7 in Apr, in contrast to markets expectations of an uptick (BBG: 79.0)

- This marks the first decline after four consecutive months of gains and the lowest reading since Jan, nevertheless expectations remain at a very high level

- The ZEW Current Conditions rose markedly, up 12.2pt to -48.8, which is significantly better than anticipated (BBG: -55) and the highest level since Mar 2020.

- Nevertheless, the the current conditions index remains in deep negative territory, hence the divergence between the expectations and the current situation persists.

- Financial market experts are concerned about a stricter lockdown which led to a decrease in expectations for private consumption says ZEW President Achim Wambach.

- "Nevertheless, the outlook for exports is better than in the previous month", Wambach added.

- EZ economic sentiment dropped by 7.7pt to 66.3 in Apr, while current conditions edged up by 4.3pt to -65.5.

- Inflation expectations for the EZ declined 5.5pt to 75.1, although the indicator still signals rising inflation over the next 6 months.

FIXED INCOME: Supply and CPI

- Core fixed income has moved moderately lower this morning as the market digests a huge amount of issuance. Italian and Dutch spreads have widened due to issues from those countries.

- It's a big day for supply: Italy has already held a 3/5/15y BTP auction and the UK a 50-year gilt auction. Spain and the Netherlands are launching 15y issues, Austria holding a 4y/50y syndication, Germany selling linkers via auction and the US is selling $24bln 30-year USTs via auction. The EGB issues are likely to sum to around E28.5bln.

- With the reflation trade having been one of the key talking points of 2021, there will be huge interest in today's US CPI print, which is due for release at 8:30ET/13:30BST. There are also a number of Fed speakers today with Harker, Daly, Barkin and Mester all due to make appearances.

- TY1 futures are down -0-5 today at 131-15 with 10y UST yields up 2.3bp at 1.691% and 2y yields up 0.3bp at 0.172%.

- Bund futures are down -0.14 today at 171.16 with 10y Bund yields up 1.1bp at -0.284% and Schatz yields up 0.3bp at -0.709%.

- Gilt futures are down -0.04 today at 128.08 with 10y yields up 0.8bp at 0.796% and 2y yields up 0.5bp at 0.052%.

FOREX: Markets Await CPI, Fedspeak

- Currencies largely trade inside recent ranges, with traders awaiting today's CPI release and a deluge of Fedspeak ahead of the media blackout period that comes this weekend. The USD is mixed, with some pre-NY hours weakness emerging to erase modest gains seen in Asia-Pac trade.

- Price action again favours GBP, although GBP/USD is yet to top the Monday high. NOK and CAD are again softer as middling oil prices do little prop up the oil-tied currency outlook.

- Front-end implied vols are inching lower, with GBP implieds seeing the most notable decreases. The 1m contract now trades below the early April lows to rival February's post-pandemic low.

- After a quiet Monday, the events calendar gets considerably busier Tuesday, starting with US CPI, which is forecast to have risen 0.5% in March. There are also a number of Fed speakers, with Harker, Daly, Barkin, Mester, Bostic and Rosengren all due.

EQUITIES: U.S. Futures Flat As Earnings Season Gets Underway

- Asian stocks closed mostly higher, with Japan's NIKKEI up 212.88 pts or +0.72% at 29751.61 and the TOPIX up 3.96 pts or +0.2% at 1958.55. China's SHANGHAI closed down 16.478 pts or -0.48% at 3396.47 and the HANG SENG ended 43.97 pts higher or +0.15% at 28497.25.

- European equities are flat/higher, with the German Dax up 41.46 pts or +0.27% at 15246.97, FTSE 100 down 1.87 pts or -0.03% at 6879.4, CAC 40 up 19.49 pts or +0.32% at 6179.11 and Euro Stoxx 50 up 10.76 pts or +0.27% at 3972.82.

- U.S. futures are flat, with the Dow Jones mini up 24 pts or +0.07% at 33655, S&P 500 mini up 0.75 pts or +0.02% at 4121, NASDAQ mini down 3.75 pts or -0.03% at 13805.

COMMODITIES: Silver Outperforms As Gold Continues To Fall

- WTI Crude up $0.1 or +0.17% at $60.03

- Natural Gas down $0.02 or -0.59% at $2.544

- Gold spot down $4.28 or -0.25% at $1727.53

- Copper up $1.95 or +0.49% at $402.4

- Silver up $0.15 or +0.61% at $24.941

- Platinum down $1.54 or -0.13% at $1173.9

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.