Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- U.S. CPI SEEN DECELERATING IN JUNE, WITH "TRANSITORY" COMPONENTS IN FOCUS

- E.C.B. SIGNALS READINESS TO CURB BANK DIVIDENDS WHEN CAP LIFTS

- P.B.O.C. SAYS PRUDENT POLICY TO GUIDE NEXT STEPS

- B.O.E. SEES SHORT-TERM RECOVERY RISKS REMAINING

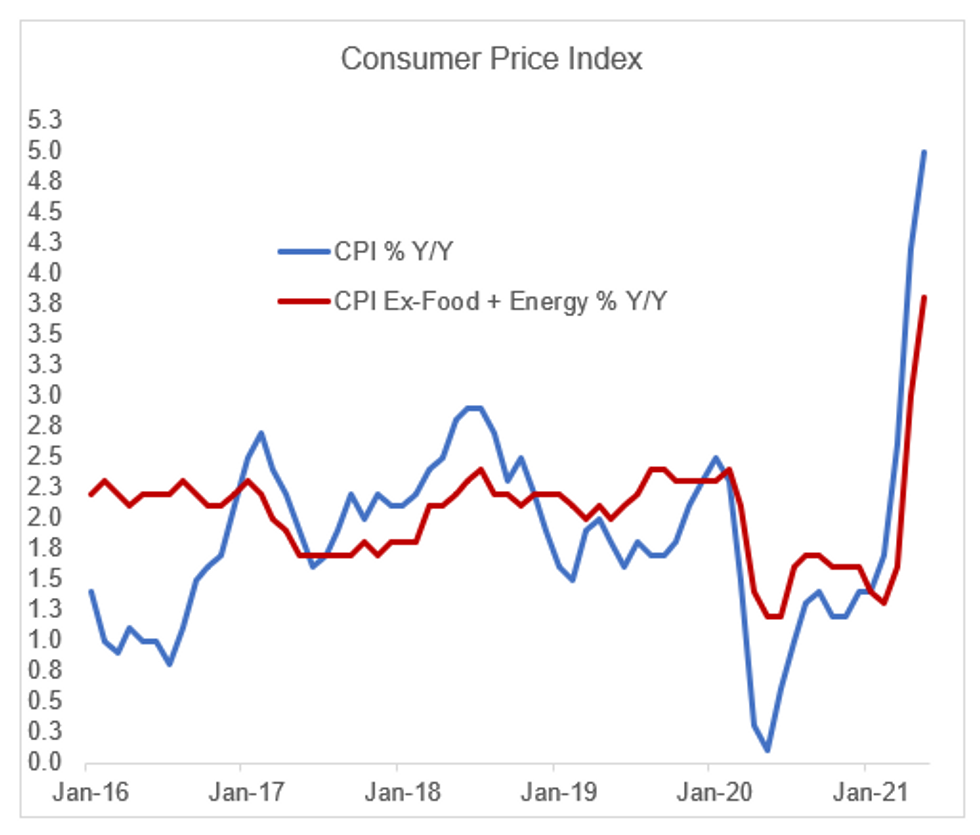

Fig. 1: U.S. CPI Seen Decelerating In June

Source: BLS, MNI

Source: BLS, MNI

NEWS:

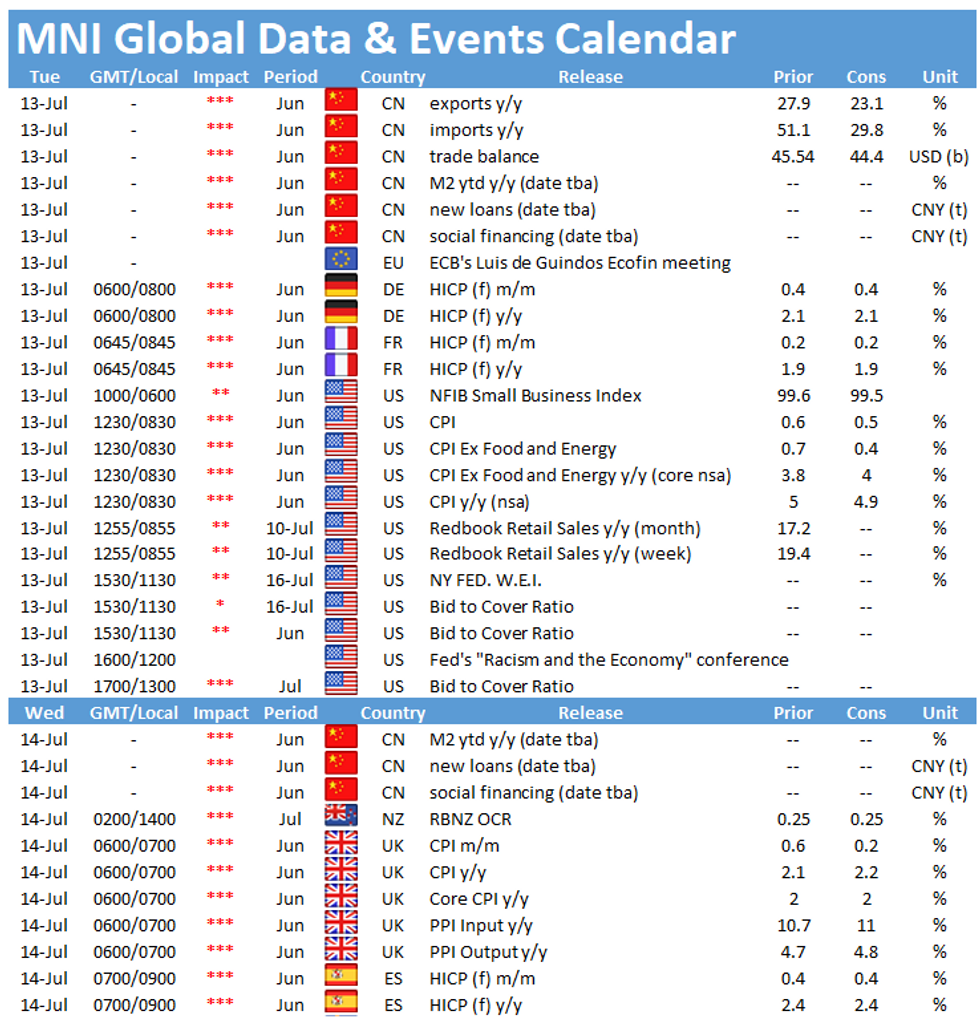

U.S. CPI: Bloomberg Consensus sees June U.S. headline CPI (0830ET/1330BST) slipping to +0.5% M/M vs +0.6% in May (and +4.9% Y/Y vs +5.0 prior), with core falling to +0.4% M/M vs +0.7% in May (though ticking up to +4.0% Y/Y vs +3.8% prior).

- MNI's data team writes that price pressures continued through June as labor shortages and ongoing supply chain disruptions hampered goods production and demand rose solidly. High inflation readings are being amplified by pandemic base effects / transitory factors should begin to fade soon, but will likely running above 2.5% Y/Y through 2022.

- With base effects continuing to distort the Y/Y figures, focus will be on the M/M readings, particularly for core: BBG survey range is +0.2-+0.6% (avg 0.44%, with a fairly narrow standard deviation of +0.09%, suggesting a potentially amplified reaction to an outsized miss).

PBOC: Monetary policy stability will guide the People's Bank of China in the second half of this year based on domestic inflation and the overall economic situation with a possible tightening move by the US Federal Reserve ahead not a main factor, said Sun Guofeng, head of the central bank's monetary policy department, at a briefing on Tuesday. A surprise 50 bps cut for all banks in the cash reserve requirement ratio last week was outlined as a regular monetary policy operation after conditions returned to the pre-pandemic norms in H1, and did not alter a prudential policy stance, said Sun, giving no details when asked if there will be more cuts in the cash ratio, or other rates, coming.

B.O.E.: Although the economic outlook has improved since the publication of the Bank of England's December Financial Stability Report, risks to the recovery are still there, particularly in the near-term, the central bank's latest edition says Tuesday. Pointing to examples, the Bank's report says despite the better outlook on the vaccine rollout, "economic activity could be curtailed following a further pickup in Covid case numbers, or a possible drop in vaccine effectiveness arising from mutations of the virus."

E.U. (Twitter): Ursula von der Leyen on Twitter: "More than half of all adults in the EU are now fully vaccinated! Enough doses have been delivered to vaccinate 70% of adults in the EU."

DATA:

MNI: FRANCE JUN FINAL HICP +0.2% M/M, +1.9% Y/Y; MAY +1.8% YY

GERMANY JUN FINAL HICP +0.4% M/M, +2.1% Y/Y; MAY +2.4% YY

FIXED INCOME: Two "I"s: Inflation and Issuance

The focus for fixed income markets this morning is on the two "I"s: inflation and issuance.

- The data calendar has already seen final prints of German and French HICP (in line with the flash estimates) but the real focus of the day will be on US CPI. The Bloomberg consensus looks for 0.5% M/M headline reading (although only 31/68 analysts forecast the 0.5% figure). There are almost as many forecasts for 0.4% and 0.6% with slightly more going for the higher print. For the ex-food and energy print, analysts are split between 0.4% and 0.5% M/M.

- It has also been a big day for issuance. The EU has held a dual-tranche transaction, selling E5.25bln of 10-year EFSM/MFA and E10bln of 20-year NGEU bonds. The UK a GBP7bln syndication for its new 1.125% Jan-39 gilt. The Netherlands and Italy have also held auctions for E2.42bln and E9bln respectively. Germany is still due to sell Schatz for E5bln and the US will reopen its 30-year bond for USD24bln.

- Against this backdrop core fixed income is largely unchanged on the day.

- TY1 futures are down -0-0+ today at 133-12+ with 10y UST yields down -0.1bp at 1.365% and 2y yields up 0.4bp at 0.232%.

- Bund futures are up 0.01 today at 174.06 with 10y Bund yields down -0.3bp at -0.299% and Schatz yields up 0.2bp at -0.676%.

- Gilt futures are down -0.02 today at 128.92 with 10y yields down -0.6bp at 0.644% and 2y yields down -1.0bp at 0.078%.

FOREX: USD Outlook Remains Constructive

- The USD outlook remains constructive, with European hours seeing some modest greenback buying against most other majors. EUR/USD and GBP/USD have been dragged off the overnight highs of 1.1875 and 1.3905 respectively, as markets also took the opportunity to keep the equity uptrend in tact. The e-mini S&P is already gravitating toward the alltime highs posted late Monday.

- Antipodean currencies continue to trade favourably, with the AUD and NZD among the strongest in G10 so far. Moves come ahead of the RBNZ rate decision due overnight, at which the bank are expected to open up the possibility of policy tightening to head off any simmering overheating pressures.

- CNH is firmer for a third consecutive session, with USD/CNH back below the 100-dma at pixel time. A break below 6.4586 would open further losses for the pair, with the 6.4354 level the next downside target.

- The June US CPI release is expected to slow slightly from the previous, with consensus seeing 0.5% M/M (Prev. 0.6%) and 4.9% Y/Y (Prev. 5.0%).

- Separately, the Fed are holding an event discussing racism and the economy from 1700BST/1200ET onwards. Fed's Kashkari, Bostic and Rosengren are due to appear.

EQUITIES: S&P Futs Still Around All-Time Highs, With Earnings Looming

- Asian markets closed stronger, with Japan's NIKKEI up 149.22 pts or +0.52% at 28718.24 and the TOPIX up 14.31 pts or +0.73% at 1967.64. China's SHANGHAI closed up 18.686 pts or +0.53% at 3566.522 and the HANG SENG ended 448.17 pts higher or +1.63% at 27963.41.

- European equities are trading mixed but basically flat, with the German Dax down 5.51 pts or -0.03% at 15769.61, FTSE 100 up 21.52 pts or +0.3% at 7140.55, CAC 40 down 8.69 pts or -0.13% at 6550.52 and Euro Stoxx 50 down 0.19 pts or 0% at 4091.61.

- U.S. futures are flat, with the Dow Jones mini up 3 pts or +0.01% at 34878, S&P 500 mini up 0.5 pts or +0.01% at 4377, NASDAQ mini up 29.25 pts or +0.2% at 14898.5.

COMMODITIES: Oil Ticks Higher As Metals Stall

- WTI Crude up $0.58 or +0.78% at $74.52

- Natural Gas down $0.01 or -0.21% at $3.744

- Gold spot up $2.61 or +0.14% at $1811.55

- Copper down $1.75 or -0.41% at $432.55

- Silver up $0.04 or +0.14% at $26.3006

- Platinum down $2.81 or -0.25% at $1123.82

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.