Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- AUSTRIA BACK IN LOCKDOWN AHEAD OF MANDATORY VACCINE POLICY

- HEALTH MINISTER SPAHN: GERMANS WILL BE "VACCINATED, CURED OR DEAD"

- SCHOLZ CLOSER TO GERMAN CHANCELLERY; LINDNER AS FINANCE MINISTER

- SOME CHINESE BANKS TOLD TO ISSUE MORE LOANS FOR PROPERTY PROJECTS (RTRS SOURCES)

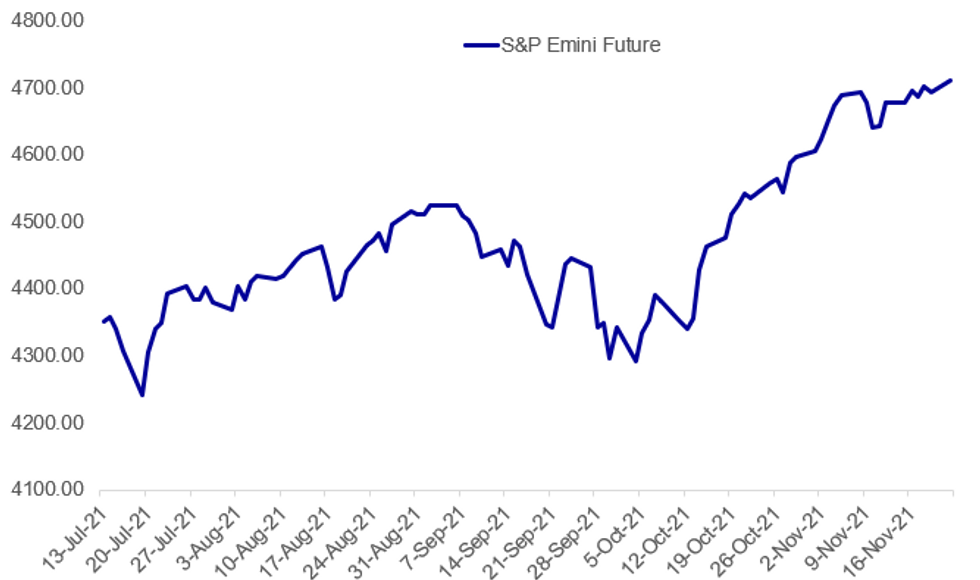

Fig. 1: Stock Futures Edge Higher To Start The Week

Source: BBG, MNI

Source: BBG, MNI

NEWS:

COVID / AUSTRIA (BBG): Austria awoke on Monday to its fourth national lockdown since the start of the pandemic. Through mid-December, Austrians will only be allowed to leave home for work, essential shopping and exercise, measures intended to put a brake on infections that have quadrupled in a month. Restrictions may last longer for the unvaccinated. The Central European nation is also about to become a testing ground for overcoming vaccine skeptics, with mandatory vaccinations due to kick in from February. That would be the first such policy by a country in Europe.

GERMANY / COVID (AFP): Most Germans will be "vaccinated, cured or dead" from Covid in a few months' time, Health Minister Jens Spahn warned Monday, urging more citizens to get jabbed. "Probably by the end of this winter, as is sometimes cynically said, pretty much everyone in Germany will be vaccinated, cured or dead," Spahn said, blaming "the very contagious Delta variant" ."That is why we so urgently recommend vaccination," he added.

GERMAN POLITICS (BBG): Germany's next government under Olaf Scholz as chancellor is taking on more defined contours, with key posts all but filled. Christian Lindner -- the head of the pro-business Free Democrats -- would be tapped as finance minister, and Robert Habeck -- co-leader of the Greens -- would become a "super minister" in charge of economy, climate protection and energy transition. Both would also be vice chancellors, according to a preliminary list of cabinet posts obtained by Bloomberg. Annalena Baerbock, the Greens' former chancellor candidate, would be foreign minister.

CHINA BANKS (RTRS): Some Chinese banks have been told by financial regulators to issue more loans to property firms for project development, two banking sources with direct knowledge of the situation told Reuters on Monday, in efforts to marginally ease liquidity strains across the industry. Chinese authorities have yet to publicly give any signal that they will relax the "three red lines" - financial requirements introduced by the central bank last year that developers must meet to get new bank loans. But lenders have recently adjusted their lending practices to reflect the latest central bank guidance of "meeting the normal financing needs" of the sector.

JAPAN / OIL (RTRS): Japanese officials are working on ways to get around restrictions on releasing national reserves of crude oil in tandem with other major economies to dampen prices, four government sources with knowledge of the plans told Reuters. While Prime Minister Fumio Kishida signalled his readiness over the weekend following a request from Washington, the world's fourth-biggest oil buyer is restricted on how it can act with its reserves - made up of both private and public stocks - which typically can only be used in times of shortage. One of the sources said the government was looking into releasing from the portion of the state-held stocks outside the minimum amount required as a legal workaround. The Biden administration made the unusual request to other major economies to consider releasing oil from their strategic reserves as high prices are starting to produced unwanted inflation and undermine recovery from the COVID-19 pandemic.

EUROPEAN BANKS / ECB: No European bank currently meets all the European Central Bank's expectations on the climate and environment(C&E), Executive Board member Frank Elderson writes in a blog post published Monday, with the considerable variation in the plans for improvement presented and only half set to be in place by the end of next year. It comes as the supervisors publish the results of their first-ever large-scale assessment of banks' climate and environmental risk management provisions, covering 112 directly supervised banks with combined assets of EUR24 trillion.

AIRLINES / TRAVEL (RTRS): The boss of the British Airways owner, IAG, said on Monday its transatlantic bookings had already reached nearly 100% of 2019 levels after the United States dropped restrictions earlier this month. Luis Gallego told the Airlines UK conference that the group was recovering, but he warned that a move by London's Heathrow Airport to hike charges could hit that process. "Now as the world opens up, we are growing our capacity," he said. "Transatlantic bookings have already reached almost 100% of 2019 levels."

DATA:

BELGIUM / CONSUMER CONFIDENCE (BBG): Belgium's consumer confidence index drops to 1, the lowest reading since April, from 4 in October as households became the most pessimistic in 12 months about the economic outlook, according to emailed statement on Monday from the National Bank of Belgium. Gauge of outlook for the Belgian economy at minus 7, down from zero in prior month and the lowest reading since November 2020.FIXED INCOME: Off To A Weak Start

Sovereign bonds have started the week on an uneven footing. Having initially opened lower, European FI recovered early losses and traded above the Friday close before selling off again towards the Monday open.

- USTs have underperformed European bonds with cash yields broadly 2-3bp higher across the curve. TYZ1 trades at 130-17, near the bottom of the day's range (L: 130-16+ / H: 130-24)..

- Gilts have similarly weakened with yields pushing up 2-3bp and the curve marginally bear flattening.

- The sell off in bunds has so far been more contained with yields trading within 1bp of the Friday close.

- The BTP curve has slightly bear steepened with the 2s30s spread 1bp wider.

- Protests towards fresh Covid-related social restrictions in Europe continued over the weekend with the Netherlands, Belgium and Austria being he main flashpoints.

- Speaking at a CBI Conference, UK PM Boris Johnson has said he expects people to resume office working, although there is no formal policy to motivate the return to the office.

- The European data slate is light today.

- Scheduled ECB speakers include Holzman, Kazaks, Kazimir, de Cos and Guindos.

FOREX: AUD Joins Equities in Recovering Off Lows

- AUD trades most favourably early Monday, with AUD/USD inching higher to further erase the losses suffered on Friday. The pair still remains well short of the Friday highs at $0.7291.

- Price action elsewhere has been largely rangebound. EUR/CHF remains a focus, with the cross in a holding pattern below the 1.05 handle. Some attention was paid to the weekly SNB sight deposits data, with CHF running slightly higher as the data showed the central bank did not meaningfully intervene in the FX rate despite recent CHF strength.

- JPY trades at the bottom end of the G10 table, with USD/JPY back above the Y114.00 handle as equities improve off lows. Progress is needed through Friday's 114.54 to cement any improvement in the near-term outlook.

- GBP is similarly offered, further reinforcing the view that recent rallies have been corrective in nature. Moves also follow Friday's CFTC release showing the GBP net position had deteriorated to its largest short position in over 12 months.

- The data slate is typically light for a Monday, with US existing home sales and Eurozone consumer confidence data the sole releases. ECB's Holzmann, de Cos and de Guindos make up the speaker schedule.

EQUITIES: US Futures Edging Higher

- Asian stocks closed mixed, with Japan's NIKKEI up 28.24 pts or +0.09% at 29774.11 and the TOPIX down 1.71 pts or -0.08% at 2042.82. China's SHANGHAI closed up 21.707 pts or +0.61% at 3582.08 and the HANG SENG ended 98.63 pts lower or -0.39% at 24951.34.

- European equities are mostly higher, with energy and communications companies leading - the German Dax is down 9.45 pts or -0.06% at 16150.11, FTSE 100 up 25.09 pts or +0.35% at 7248.66, CAC 40 up 19.45 pts or +0.27% at 7134.3 and Euro Stoxx 50 down 0.11 pts or 0% at 4356.34.

- U.S. futures are a little higher, with the Dow Jones mini up 103 pts or +0.29% at 35652, S&P 500 mini up 14 pts or +0.3% at 4708.5, NASDAQ mini up 64.25 pts or +0.39% at 16639.25.

COMMODITIES: Oil Regains Ground From Drop Friday; Gov'ts Look To Release Reserves

- WTI Crude up $0.38 or +0.5% at $76.35

- Natural Gas down $0.18 or -3.46% at $4.884

- Gold spot up $0.29 or +0.02% at $1845.88

- Copper down $1.3 or -0.3% at $438.2

- Silver up $0.23 or +0.93% at $24.8372

- Platinum up $4.32 or +0.42% at $1038.78

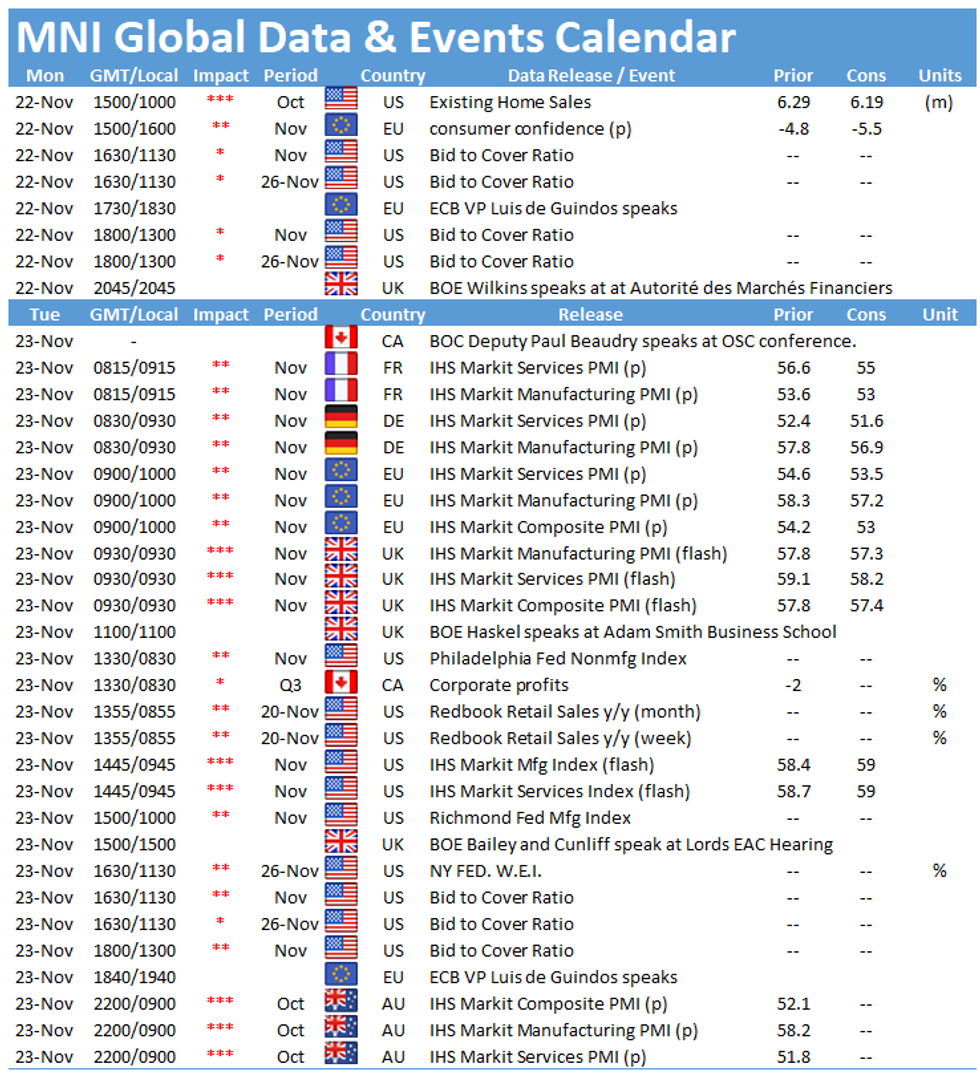

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.