Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- NEW ZEALAND DOLLAR FALLS AS COUNTRY RE-ENTERS LOCKDOWN

- U.K. SEES STRONG GROWTH IN JOB VACANCIES, WAGES

- JAPAN PM TO EXTEND TOKYO COVID STATE OF EMERGENCY

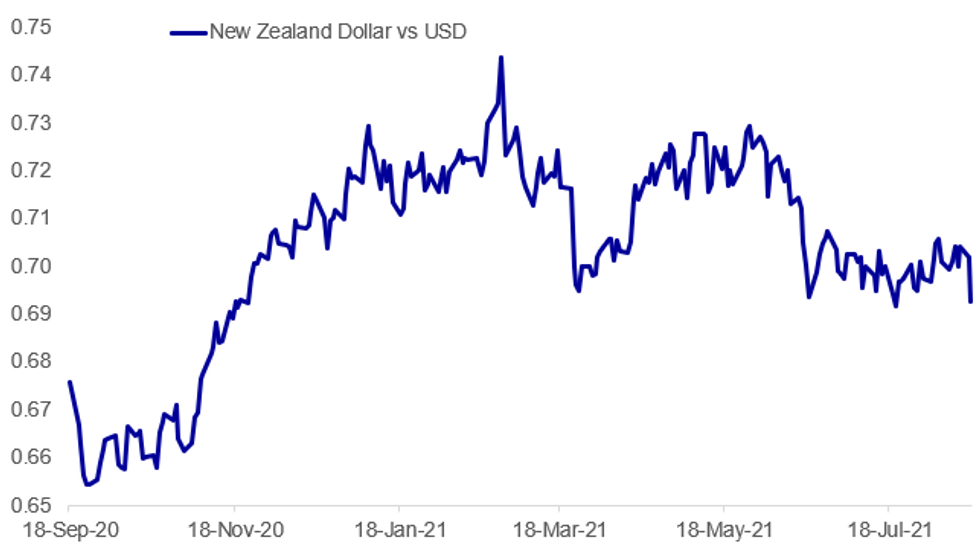

Fig. 1: Kiwi Falls On COVID Lockdown

Source: BBG, MNI

Source: BBG, MNI

NEWS:

NEW ZEALAND / COVID: NZD/USD trades at new daily and monthly lows as New Zealand PM Ardern confirms the country is to enter a 3-day lockdown after the detection of one COVID case. The 3-day lockdown is effective in all areas outside of Auckland and Coromandel, which undergo a 7-day lockdown. The PM also confirms that all vaccinations have been suspended for 48 hours, warning that "we all see what happened in Sydney, don't want that here".

NEW ZEALAND / RBNZ: Following the discovery of community transmission and the nationwidelockdown, Westpac revise their call for a rate hike from the RBNZ this week(decision due tomorrow) and now see policy unchanged. Westpac and the broad consensus was for a 25bps hike to 0.50%.

JAPAN / COVID: Gearoid Ready at Bloomberg tweets the latest COVID-19 figures from the Japanese capital, Tokyo: "Tokyo coronavirus case count for today is 4,377. Previous two Tuesdays: 2,612, 3,907. Serious cases +8 to 276. Newly reported deaths: 8. Cases last week were likely impacted by three-day weekend" The continued rise in cases is set to prompt an extension of the full state of emergency measures in place in Tokyo. These were due to expire on 31 August, but now are set to last until 12 September at the earliest. The full state of emergency measures will also be extended to the prefectures of Ibaraki, Tochigi, Gunma, Shizuoka, Kyoto, Hyogo and Fukuoka according to Reuters, and will end up applying to 60% of the Japanese population.

AFGHANISTAN (AP): The Taliban declared an "amnesty" across Afghanistan and urged women to join their government Tuesday, seeking to convince a wary population that they have changed a day after deadly chaos gripped the main airport as desperate crowds tried to flee the country.Following a blitz across Afghanistan that saw many cities fall to the insurgents without a fight, the Taliban have sought to portray themselves as more moderate than when they imposed a brutal rule in the late 1990s. But many Afghans remain skeptical.

CHINA / TECH (BBG): China's latest moves to tighten its grip on the nation's internet giants helped trigger a fifth consecutive day of selling in the nation's bellwether technology stocks. The Hang Seng Tech Index dropped 3.1%, after the market regulator issued draft rules banning unfair competition among the nation's online platform operators. Alibaba Group Holding Ltd. fell nearly 5% and was the biggest point-drag on the benchmark Hang Seng Index, which closed 1.7% lower. Losses accelerated in afternoon trade as China issued separate rules to protect key network facilities and information systems, effective next month.

CHINA / GLOBAL SHIPPING (BBG): The partial closure of the world's third-busiest container port is worsening congestion at other major Chinese ports, as ships divert away from Ningbo amid uncertainty over how long virus control measures in the city will last. In nearby Shanghai and in Hong Kong, congestion is once again increasing after dropping due to the reopening of Yantian port in Shenzhen, which shut in May for a seperate outbreak. The number of container ships anchored off Xiamen on China's southeast coast rose to 24 from 6 at the start of the month, according to shipping data compiled by Bloomberg.

DATA:

UK job vacancies surge, above a million for the first time in July

JUN UNEMPLOYMENT RATE 4.7% (APR 4.8%)

JUL CLAIMANT COUNT -7,800 TO 5.7% (JUN 5.8%)

APR-JUN AVG TOTAL EARNINGS 8.8% vs 6.6% MAY

APR-JUN AVG EARNINGS EX-BONUS 7.4% VS 7.3% MAY

------------------------------------------------------------------------------------------

UK employment levels continued to pick up in the three months to June, with the unemployment rate down to 4.7%. The more up-to-date RTI payroll employee number rose 182,000 between June and July to 28.9 million, now 201,000 below Feb 2020 levels. Average hours worked rose 1.5 to 31.0 in the three months to June.

There were a record 953,000 vacancies on average in the last three month period, with over 1 million recorded for the first time in July for the first time, touching 1,000,034 - up 50,000 on the month.

The strong growth in wages was again cautioned with the proviso of including both base and compositional effects, the ONS said.

MNI DATA BRIEF: UK Pay Growth Tops 8%; Dilemma for Sunak

UK total wages surged by an annual rate of 8.8% in the second quarter, well above the Bank of England's forecast of 8.6%. Excluding bonuses, pay growth jumped by 7.4%, topping the 6.6% pace in the three months to May. Bonuses soared by 41.1% in the second quarter and by 45.4% in the month of May.

Accelerating wage growth presents a fiscal conundrum for the chancellor, Rishi Sunak, who is bound to the triple lock, which lifts pensions by the highest of inflation, wage growth or 2.5%. The reference period for the triple lock is the three months to July, but that period will include the elevated June rate reported on Tuesday.

The ONS has attempted to adjust earnings for base and compositional effects, but their estimate is wide. Underlying regular earnings stand between 3.5% and 4.9%, while underlying total earnings range from 4.9%-6.3%. Real regular earnings rose by an annual rate of 6.6% in Q2, while real regular earnings rise by 5.2%

MNI DATA BRIEF: UK Job Vacancies Hit Record High

Employment rose by 182,000 in July, according to PAYE data, after a vastly-downwardly revised 193,000 in July (originally reported as +356,000), the Office for National Statistics said Tuesday. LFS data, which includes a wider range of workers and targets a different period, rose by a more modest 95,000 in Q2, but that was enough to push the unemployment rate down to 4.7% from 4.8% in the three months to May.

But vacancy data suggest a mismatch in worker skills and job requirements, with vacancies rising by 290,000 in the three months to July (compared with the three months to April), lifting vacancies to a record high 953,000, above the pre-pandemic level. Between June and July, vacancies increased by 50,000 to a record 1.034 million. The inactivity rate, which has been a bit sticky over the previous months of strong job creation, declined to 21.1% from 21.3% in the three months to May, while the employment rate rose to 75.1% in Q2 from 74.8% between March and May.

EUROZONE DATA: Recovery Regains Momentum in Q2

Q2 FLASH GDP +2.0% Q/Q SA, +13.6% Y/Y WDA (Q1 -0.3% Q/Q)

Q2 Y/Y FLASH GDP REVISED DOWN 0.1% FROM PRELIM. FLASH

---------------------------------------------------------------------------

- The eurozone economy expanded by 2.0% in Q2, according to a flash estimate, unchanged from the first iteration, following a 0.3% increase in Q1.

- That takes output 13.6% above the same period of 2021, slightly below the first estimate of a 13.7% rise, Eurostat said Tuesday.

- German output rose by 1.5% in Q2, while France expanded by 0.9%, Italy increased by 2.7% and Spain improved by 2.8%.

- Eurozone growth outpaced the 1.6% q/q expansion in the US and the 1.3% growth in China, although both larger economies have recovered output lost to Covid, while the eurozone is unlikely to return to pre-Covid levels until later this year at the earliest. The UK expanded by 4.8% between April and June, but remains 4.4% below its level at the end of 2019.

- Employment across the eurozone rose by 0.5 in Q2, after a 0.2% decline in the opening three months of the year. On an annual basis, eurozone employment rose by 1.8% in Q2, after slumping by 1.8% in the same period of 2020.

FIXED INCOME: Moves higher continue

After a pullback after the European open, core fixed income has continued its march higher (while the curve bull flattens) and now gilts, Treasuries and Bunds all stand above yesterday's highs. All have now fully reversed any moves lower following payrolls.

- Lockdowns in the Antipodes and the political situation in Afghanistan are weighing on sentiment today.

- The data focus for today will be US retail sales (and to a lesser extent IP). We have already received UK labour market data which had something for everyone, and was largely in line with expectations while the second print of Eurozone GDP was in line with the first.

- Powell is due to speak later; markets will watch but he is not expected to say anything new on the economy. Kashkari is also due to speak.

- TY1 futures are up 0-6+ today at 134-17 with 10y UST yields down -4.0bp at 1.227% and 2y yields down -1.1bp at 0.200%.

- Bund futures are up 0.36 today at 177.16 with 10y Bund yields down -2.6bp at -0.496% and Schatz yields down -0.9bp at -0.752%.

- Gilt futures are up 0.32 today at 130.12 with 10y yields down -3.6bp at 0.537% and 2y yields down -1.9bp at 0.118%.

FOREX: NZD Sold at Fastest Pace Since March as Ardern Cracks Down

- NZD has slipped aggressively against all others, with markets swiftly paring rate hike expectations as New Zealand re-enters lockdown.

- The NZ authorities have detected the first case of community-transmitted COVID-19, prompting a 3-day nationwide lockdown (and a 7-day lockdown in Auckland and surrounding areas), a move that's prompted a number of sell-side analysts to revise their calls for a 25bps rate hike from the RBNZ this week.

- NZD/USD fell at the fastest rate since March to put the pair in close proximity to the late July lows of 0.6902, sitting ahead of the key support and bear trigger at 0.6881.

- GBP/NZD has also narrowed in on some key levels, with the psychological 2.00 handle in view as well as the bull trigger at 2.0069 (late July high). If topped, the cross would trade at the highest levels since August 2020, with 2.0272 the next upside level.

- AUD is lower in sympathy, while haven currencies including JPY, CHF and USD are firmer.

- Advance US retail sales and industrial production are the data highlights, while Fed's Kashkari speak on the economy. Powell is scheduled to appear at an event with educators, but it's unclear whether he'll comment on policy.

EQUITIES: S&P Futures Retreat From Record Highs

- Japan's NIKKEI down 98.72 pts or -0.36% at 27424.47 and the TOPIX down 9.35 pts or -0.49% at 1915.63. China's SHANGHAI closed down 70.369 pts or -2% at 3446.976 and the HANG SENG ended 435.59 pts lower or -1.66% at 25745.87.

- European equities are slightly weaker, with the German Dax down 51.23 pts or -0.32% at 15854.3, FTSE 100 down 2.96 pts or -0.04% at 7128.89, CAC 40 down 31.79 pts or -0.46% at 6792.19 and Euro Stoxx 50 down 12.73 pts or -0.3% at 4183.59.

- U.S. futures are lower, with the Dow Jones mini down 150 pts or -0.42% at 35384, S&P 500 mini down 19 pts or -0.42% at 4455, NASDAQ mini down 54.25 pts or -0.36% at 15080.5.

COMMODITIES: Industrials Slip As Global Growth Concerns Linger

- WTI Crude down $0.35 or -0.52% at $66.83

- Natural Gas down $0.05 or -1.34% at $3.91

- Gold spot up $7.05 or +0.39% at $1794.74

- Copper down $2.95 or -0.68% at $429.55

- Silver up $0.06 or +0.27% at $23.8922

- Platinum down $0.64 or -0.06% at $1023.02

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.