Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- TURKISH CENTRAL BANK INTERVENES TO STABILIZE LIRA

- U.S. HOUSE OF REPS COULD VOTE ON GOV'T FUNDING BILL TODAY

- 2ND DAY OF POWELL, YELLEN TESTIMONY

- OECD: CENTRAL BANKS SHOULDN'T PANIC IN FACE OF INFLATION SPIKE

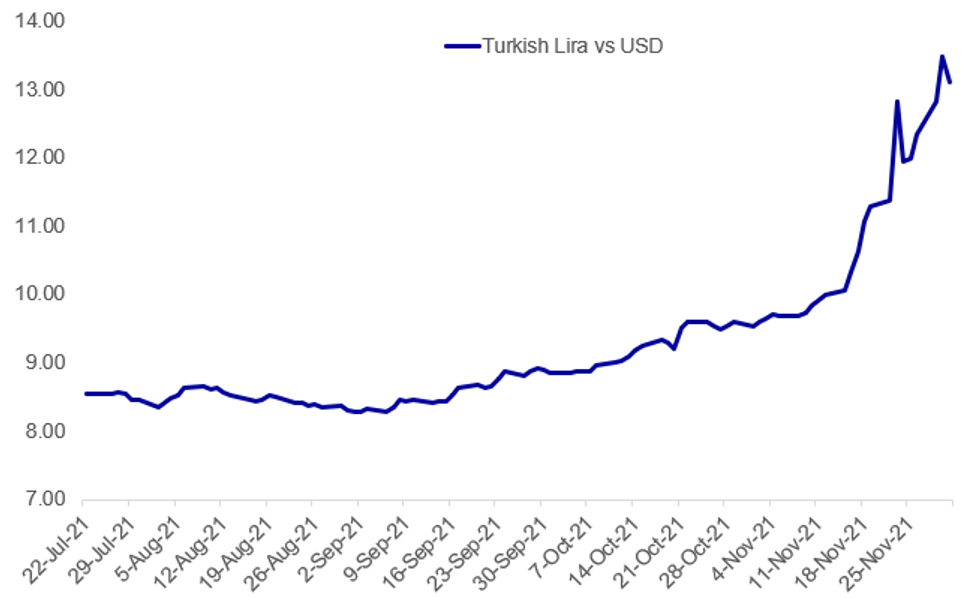

Fig.1: TRY Pares Some Depreciation On Official Intervention

Source: BBG, MNI

Source: BBG, MNI

NEWS:

TURKEY: The CBRT has announced its first official intervention on the books to stabilise the lira after a few weeks of letting the currency go. This comes after getting pledges from Turkmenistan and the UAE to support the CBRT through currency swaps, but reserves remain in a critically constrained position.- This is the first time the bank has made an official announcement since the last heavy bout of intervention in 2018/19 where the CBRT burned through $128bn in to defend the currency (unsuccessfully).

- The question is whether the CBRT views the 14.00 level as its line in the sand, and how aggressively it wishes to defend the currency amid sustained depreciation pressures.

- This could also be a prelude to more aggressive unconventional measures to curb lira weakness with the leadership team hell bent on reducing rates further in an environment that is not conducive to TRY strength.

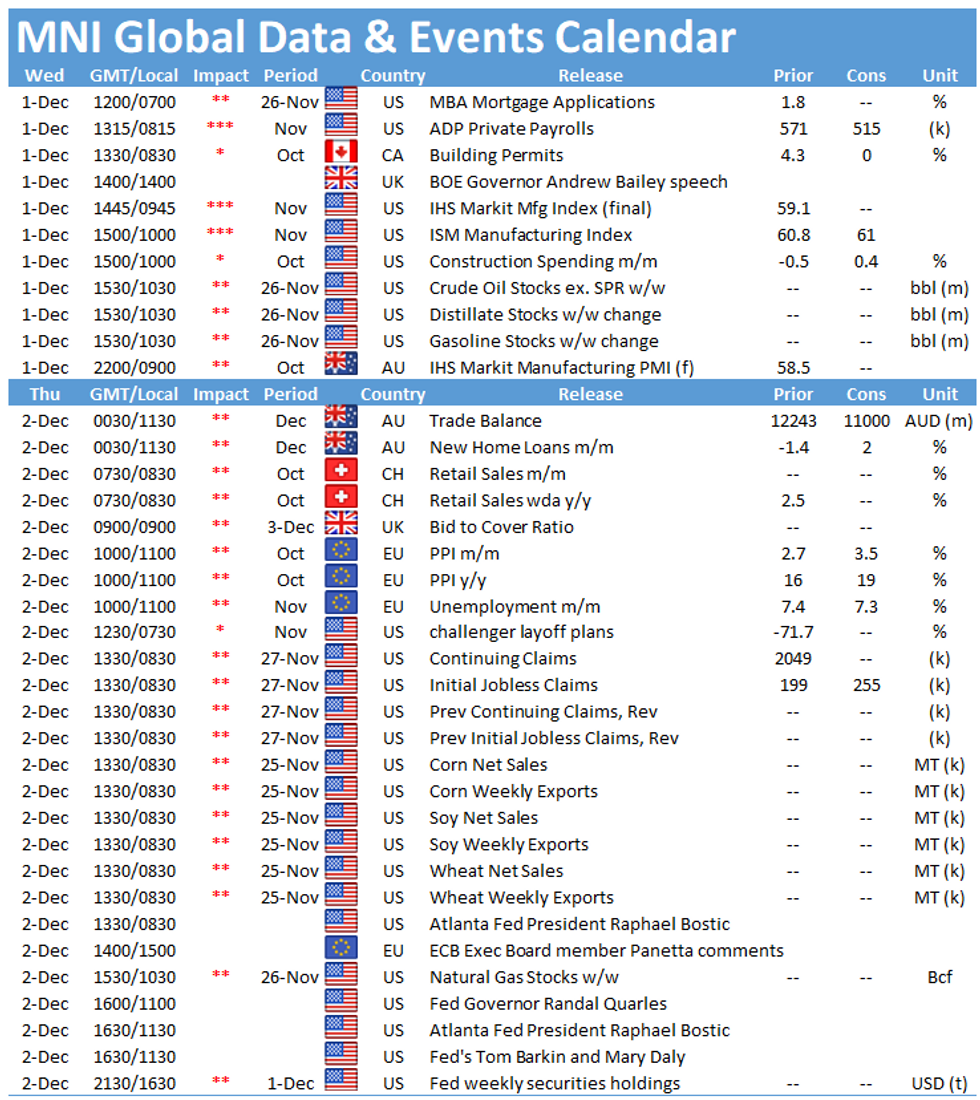

U.S. CONGRESS: Busy day in the US Congress today. The House of Representatives could vote on a bill to avoid a gov't shutdown ahead of the deadline of 23:59:59 on Friday 3 December. Despite narrow Democrat majority, this is likely to pass, but issue with passing in Senate given 50-50 split. Treasury Secretary Janet Yellen and Fed Chairman Jerome Powell are up infrontof the House Financial Services Committee to answer questions on inflation and pandemic relief. Testimony due to start at 1000ET (1500GMT, 1600CET).

DATA:

SPAIN DATA: Manufacturing PMI 57.1 (57.9 expected, 57.4 previous)

Spain manufacturing PMI for November 57.1 (57.9 expected, 57.4 previous).

PMI data paints a familiar story - but is pre-Omicron

- The story of the Spanish manufacturing PMI is a familiar one of growing demand (although recall this is before any Omicron uncertainty) and a shortage of inputs, with the latter in particular leading to higher prices.

- Not much market reaction, as expected, given this data is now outdated somewhat with the Omicron variant

- Highlights from the press release:

- "Demand growth remained positive, with new orders rising markedly, supported in part by a stronger gain in new export orders. There were reports that market demand maintained a strong underlying trend, although some concerns amongst clients over rising prices were reported.

- "Output charges amongst Spanish manufacturers were increased in November at the sharpest rate in the survey history"

- "Transportation difficulties, especially in sea freight, also persisted, and the general challenge in procuring inputs was reported to have been a major impediment to production growth in November."

ITALY DATA: Manufacturing PMI 62.8 (61.1 exp, 61.1 prev)

Italy manufacturing PMI for November 62.8 (61.1 expected, 61.1 previous)

Manufacturing PMI same story as in Spain

- Same story for the Italian PMI manufacturing as in Spain: output expectations higher, input pressures weighing on production and input price increases being passed through to higher output prices.

- As with the Spanish print, little market interest in this today given this data is pre-Omicron.

UK DATA: Final manufacturing PMI 58.1 (58.2 flash)

Final manufacturing PMI for November 58.1 (58.2 flash).

FIXED INCOME: Continued reaction to Powell

Bear steepening has been the theme of core fixed income markets this morning as European investors continue to digest comments yesterday from Powell that seemed to put a faster pace of tapering pace back on the table. The Eurodollar strip has underperformed the Euribor and short sterling strips this morning.

- There was a sharp move lower in Bunds around 8:00GMT/3:00ET with no new headline trigger. The moves seem to be attributed largely to continued reaction to Powell yesterday.

- Gilts have continued their downside moves following a very weak 10-year auction which saw a tail of 1.9bp (last matched in June 2019). Liquidity in gilt markets remains constrained, particularly with the lower supply and continued buying over the next three weeks from the BOE.

- Looking ahead ISM manufacturing will be the highlight (with ADP employment due before that). US data will be back in focus after Powell's comments yesterday.

- TY1 futures are down -0-16 today at 130-10 with 10y UST yields up 4.8bp at 1.495% and 2y yields up 3.5bp at 0.603%.

- Bund futures are down -0.53 today at 171.84 with 10y Bund yields up 3.4bp at -0.317% and Schatz yields up 2.0bp at -0.777%.

- Gilt futures are down -0.43 today at 125.85 with 10y yields up 6.5bp at 0.872% and 2y yields up 10.3bp at 0.573%.

FOREX: G10 FX Calmer, But Fragility Clear Looms Beneath the Surface

- Markets trade on a calmer footing early Wednesday, with equities higher and haven currencies on the backfoot. This has extended the recovery in USD/JPY off yesterday's lows of 112.53 to put the pair either side of 113.50 at the NY crossover.

- Despite the consolidation among spot rates, implied vol measures remain elevated, suggesting some fragility below the calmer surface of currency markets so far Wednesday.

- Markets are taking the news that the omicron variant has spread further in its stride, with focus shifting to any incoming data on vaccine efficacy or elevated side effects resulting from the new strain.

- Growth proxies and commodity-tied FX outperform, putting AUD, NZD at the top of the G10 pile. This puts NZD/USD around a point above the YTD lows printed yesterday at $0.6773, which remains key support.

- Data may take some focus going forward, although releases could be taken with a pinch of salt given the recent emergence of the omicron variant. ADP employment change data crosses, shortly followed by the ISM manufacturing survey for November. Both are expected to come in broadly inline with previous readings.

- Powell and Yellen testify for a second time on the CARES Act, which normally wouldn't phase markets, but extra attention may be paid given the volatility prompted by Powell's appearance yesterday.

EQUITIES: Energy And Financials Lead Early Bounce

- Asian markets closed higher, with Japan's NIKKEI up 113.86 pts or +0.41% at 27935.62 and the TOPIX ended 8.39 pts higher or +0.44% at 1936.74. China's SHANGHAI closed up 12.998 pts or +0.36% at 3576.885 and the HANG SENG ended 183.66 pts higher or +0.78% at 23658.92

- European bourses are bouncing, with the German Dax up 224.51 pts or +1.49% at 15100.13, FTSE 100 up 99.75 pts or +1.41% at 7059.45, CAC 40 up 89.61 pts or +1.33% at 6721.16 and Euro Stoxx 50 up 67.29 pts or +1.66% at 4063.06.

- U.S. futures are higher, with the NASDAQ leading: Dow Jones mini up 299 pts or +0.87% at 34756, S&P 500 mini up 52.75 pts or +1.16% at 4619, NASDAQ mini up 214 pts or +1.33% at 16364.5.

COMMODITIES: Big Bounce In Crude, But WTI Still Under $70

- WTI Crude up $2.83 or +4.28% at $67.88

- Natural Gas down $0.15 or -3.24% at $4.491

- Gold spot up $9.26 or +0.52% at $1786.88

- Copper up $5.1 or +1.19% at $432.2

- Silver up $0.06 or +0.25% at $22.9452

- Platinum up $17.33 or +1.85% at $954.5

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.