Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- EUROPEAN STOCKS GAIN AGAIN, GLOBAL TECH STOCKS LAG

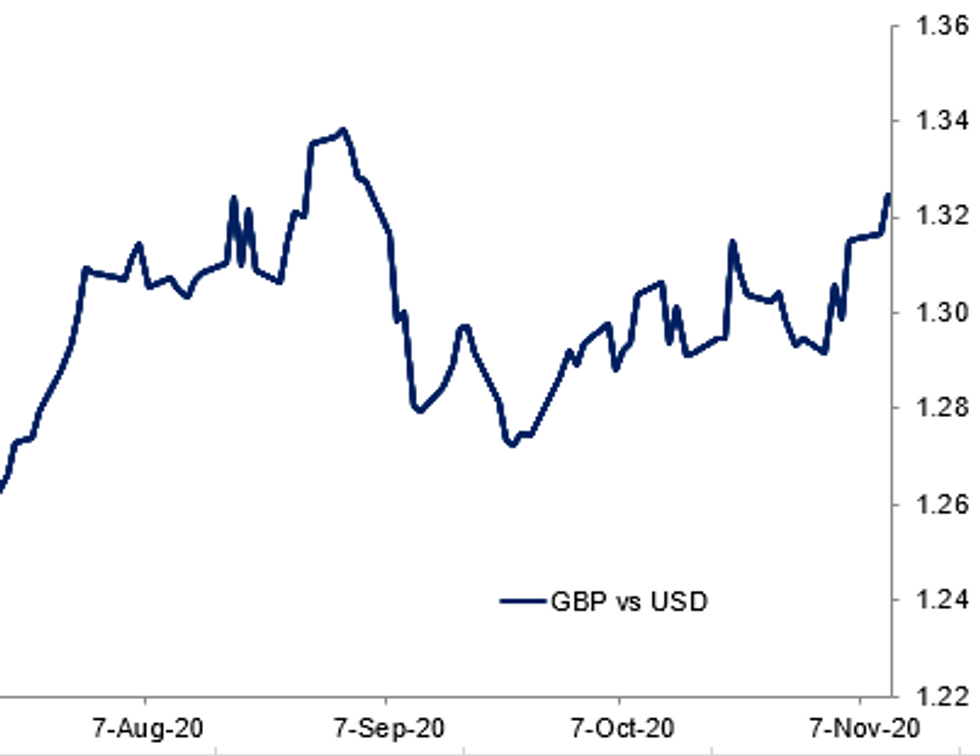

- BRITISH POUND OUTPERFORMS AS DOLLAR HEADS LOWER

- GERMAN ZEW SENTIMENT SEES FURTHER SHARP DECLINE IN NOVEMBER

- YUAN RALLY LOSING STEAM, CHINESE ADVISORS SAY (MNI EXCLUSIVE)

Fig. 1: Cable Pushes Higher

BBG, MNI

BBG, MNI

NEWS:

EQUITIES: Stocks in Europe higher for a second session, although gains so far much shallower than yesterday's rally. Spanish, French stocks outperform with the sectoral breakdown very similar to Monday: energy, financials the best performing sectors, while tech lags.- - EuroStoxx (VGZ0) already closing in on yesterday's highs of 3,441. Should markets top 3,445 that'd be the best levels since the COVID sell-off in early March.

- - Volumes yesterday were considerably higher than average (over twice the daily average) and today's also busy - volumes running around 40% above average for this time of day.

GBP AND EUR: EUR/USD hitting fresh intraday lows and nearing yesterday's lows at 1.1796. Moves not headline driven at this stage and EURGBP may be adding some weight (cross breaking below the 200-dma for the first time since May over past few mins).

- Again, no specific newsflow behind GBP move, more likely a confluence of factors: markets pricing out likelihood of easing next year (driven by yesterday's vaccine-induced rally), and could be getting some support from House of Lords resistance to Internal Markets Bill yesterday (makes including the elements that run against international law more difficult).

- Likely an element of short squeeze also - CFTC data still shows markets with a sizeable net GBP short.

GERMANY DATA: The ZEW Expectations fell further in Nov, down by 17.1pt to 39.0, coming in weaker than markets expected (BBG: 44.3). The ZEW Current Conditions eased as well in Nov, down by 4.8pt amid the renewed rise of Covid-19 cases and fresh lockdown measures, however it came in slightly better than forecasts anticipated (BBG: -65.0). The report notes that economic sentiment has deteriorated sharply again in Nov, indicating a slowdown of economic recovery in Germany. Financial experts are worried about the impact of the second wave of Covid-19 and concerns regarding a renewed recession increased. Economic Sentiment in the Eurozone dropped again as well, down 19.5pt to 32.8 in Nov, while current conditions edged up marginally by 0.2pt to -76.4.

UK DATA: UK headline labour market data largely in line with expectations with the unemployment rate increasing from 4.5% to 4.8% and employment falling -164k (-150k expected). According to the experimental HMRC payroll data:

- "In October 2020, 33,000 fewer people were in payrolled employment when compared with September 2020 and 782,000 fewer people were in payrolled employment when compared with March 2020."

- "Annual growth in payrolled employees in October 2020 was the highest inNorthern Ireland (a fall of 0.9%) and lowest in London (a fall of 4.6%)."

- Very little reaction in the pound to the data release, partly as this was largely in line with expectations and partly due to the market looking through this data given that England is in a second lockdown.

DATA:

UK Jobless Rate Edges Up; Redundancies At Record Level

JUL-SEP LFS JOBLESS RATE 4.8% VS 4.5%

JUL-SEP AVG TOTAL EARNINGS +1.3% VS +0.1% PRIOR

JUL-SEP AVG EARNINGS EX-BONUS +1.9% VS +0.9% PRIOR

OCT CLAIMANT COUNT down 29,800 to 2,633,700

The UK's jobless rate edged up further in Sep to 4.8% which is the highest level since Jun-Aug 2016, up from 4.5% recorded previously and coming in line with market forecasts. The employment rate ticked down to 75.3% in Sep, while the inactivity rate remained almost unchanged at 20.9%. More up-to-date PAYE data showed another decline of payrolled employees. In Oct 33,000 fewer people were in payrolled employment compared to September, leading to 782,000 fewer people since March 2020. The LFS survey showed that redundancies increased in Sep, reaching a record high of 314,000, also a record increase of 181,000 on the quarter. Vacancies ticked up as well by 146,000 on the quarter in Oct, however they remain below pre-pandemic levels. Moreover, avg actual hours worked rose to 28.5 in Sep, up from 27.3 in Aug but it remains below Feb's pre-crisis level. The claimant count rate ticked down marginally by 0.1% to 7.3% in Oct.

Italian IP Weaker Than Expected in Sep

- Sep SA ind. output -5.6% m/m (Aug rev'd dn +7.4% m/m), WDA -5.1% y/y, falling short of market forecasts (BBG: -2.0% m/m)

- Italy Sep SA IND m/m output fell after 4 straight gains--ISTAT

- Italy Sep SA IND m/m output still +1.3% above Jul 2020 level--ISTAT

- Sep SA m/m consumer, capital, intermed. gds, energy dropped—ISTAT

- Sep WDA y/y consumer, capital, intermed. gds, energy all fell--ISTAT

- There were 22 working days in Sep 2020 vs. 21 in Sep 2019.

FIXED INCOME: Still digesting the Pfizer vaccine news

It has been a generally risk-positive morning session with equities higher and core bonds lower across the board as markets continue to digest yesterday's positive news regarding the Pfizer vaccine.

- Treasuries and gilts have remained within yesterday's range while Bund futures have broken through yesterday's low and are currently flirting with the 100-dma which comes in at 174.24 ahead of support from the Oct 8/7 lows at 174.04/93.

- The EC has come back to the market today to issue another EUR14bln of the EU SURE bonds - EUR8bln of the 5-year and EUR6bln of the 30-year with huge books. This puts total issuance from the EU SURE programme at EUR31bln since its launch three weeks ago.

- There has been little unique movement in gilts after yesterday's vote against the controversial elements of the Internal Market bill.

- TY1 futures are up 0-2 today at 137-20+ with 10y UST yields up 1.4bp at 0.938% and 2y yields up 0.4bp at 0.178%.

- Bund futures are down -0.14 today at 174.22 with 10y Bund yields up 1.2bp at -0.499% and Schatz yields up 0.3bp at -0.732%.

- Gilt futures are up 0.03 today at 134.30 with 10y yields up 0.7bp at 0.378% and 2y yields up 0.9bp at -0.4%.

FOREX: EUR/GBP Dips to Multi-Month Low

EUR/USD sits below the Monday low headed into the NY crossover, with support at 1.1796 giving way. Moves in currency markets this morning have not been headline driven, but crosses including EURGBP may be adding some weight to the single currency. The cross broke below the 200-dma at 0.8924 for the first time since May, helping GBP sit at the top of the G10 pile early Tuesday.

Sterling may be getting some support as markets rush to price out the likelihood of lower rates in the UK next year (driven by yesterday's vaccine-induced rally), and could be benefitting from resistance in the House of Lords yesterday to the government's Internal Markets Bill, which could make including the elements that run against international law more difficult.

While GBP outperforms, EUR is lagging alongside CHF and SEK.

Fedspeak tops the agenda Tuesday, with speeches due from Kaplan, Rosengren, Bostic, Quarles and Brainard. There is no data of note.

EQUITIES: Rotation Out Of Tech Continues

Global equities continue to gain steam in the wake of Monday's Pfizer vaccine news, with one notable sectoral exception: tech (NASDAQ futures lower for instance), as investors rotate out of tech stocks.

- Asian stocks closed mixed, with Japan's NIKKEI up 65.75 pts or +0.26% at 24905.59 and the TOPIX up 18.9 pts or +1.12% at 1700.8. China's SHANGHAI closed down 13.586 pts or -0.4% at 3360.148 and the HANG SENG ended 285.31 pts higher or +1.1% at 26301.48

- European equities are broadly higher, with the German Dax down 21.15 pts or -0.16% at 13097.09, FTSE 100 up 80.13 pts or +1.3% at 6187.49, CAC 40 up 75.5 pts or +1.41% at 5327.74 and Euro Stoxx 50 up 19.24 pts or +0.56% at 3413.43.

- U.S. futures are mixed, with the Dow Jones mini up 182 pts or +0.63% at 29238, S&P 500 mini up 3.25 pts or +0.09% at 3547.25, NASDAQ mini down 96.25 pts or -0.81% at 11724.5.

COMMODITIES: WTI Regains $40/bbl

Another impressive pro-cyclical move takes WTI crude again above the $40/bbl mark after overnight losses. Resistance is at $41.33 (yesterday's high) then $42.02 Sept 18th high.

- WTI Crude up $0.66 or +1.64% at $40.44

- Natural Gas up $0.03 or +1.08% at $2.897

- Gold spot up $12.7 or +0.68% at $1888.77

- Copper down $1.25 or -0.4% at $314.4

- Silver down $0.08 or -0.34% at $24.3505

- Platinum up $4.3 or +0.49% at $879.95

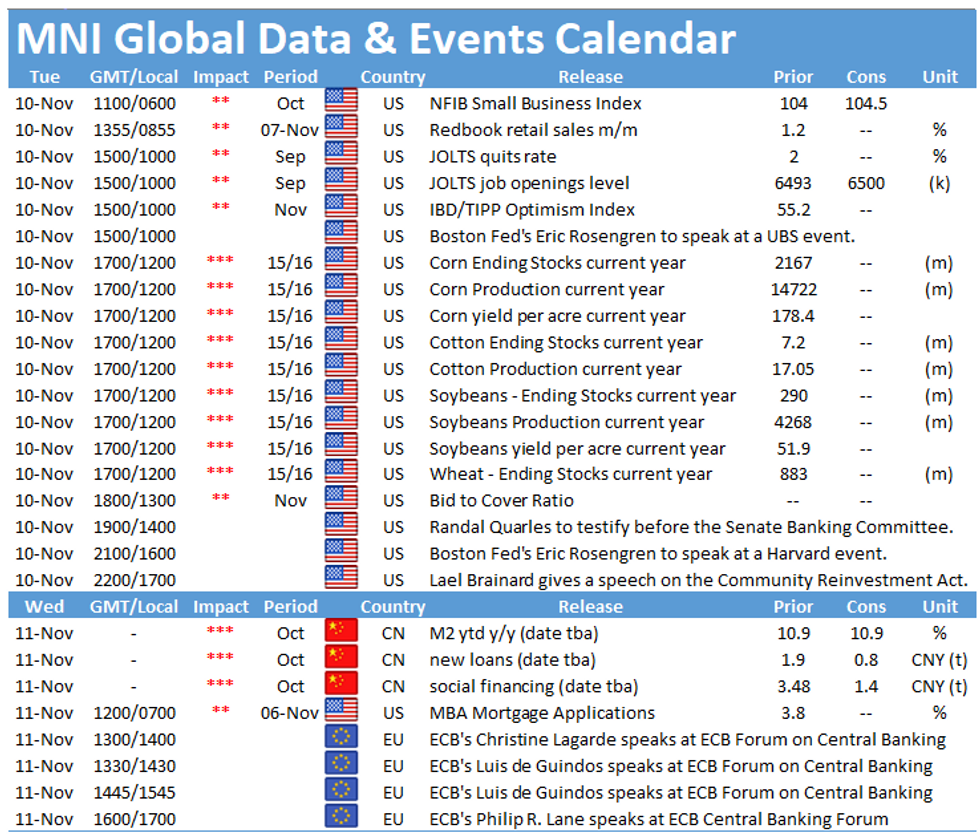

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.