Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- EUROZONE INFLATION NEARS 30-YR HIGH

- MODERNA CEO PREDICTS VACCINES TO STRUGGLE WITH OMICRON: FT

- GERMANY MULLS LOCKDOWN ON UNVACCINATED AS EUROPE TIGHTENS CURBS

- EMA IN POSITION TO APPROVE NEW OMICRON JABS IN 3-4 MONTHS

- BANK OF JAPAN ON GUARD OMICRON COULD HIT ECONOMIC RECOVERY (MNI INSIGHT)

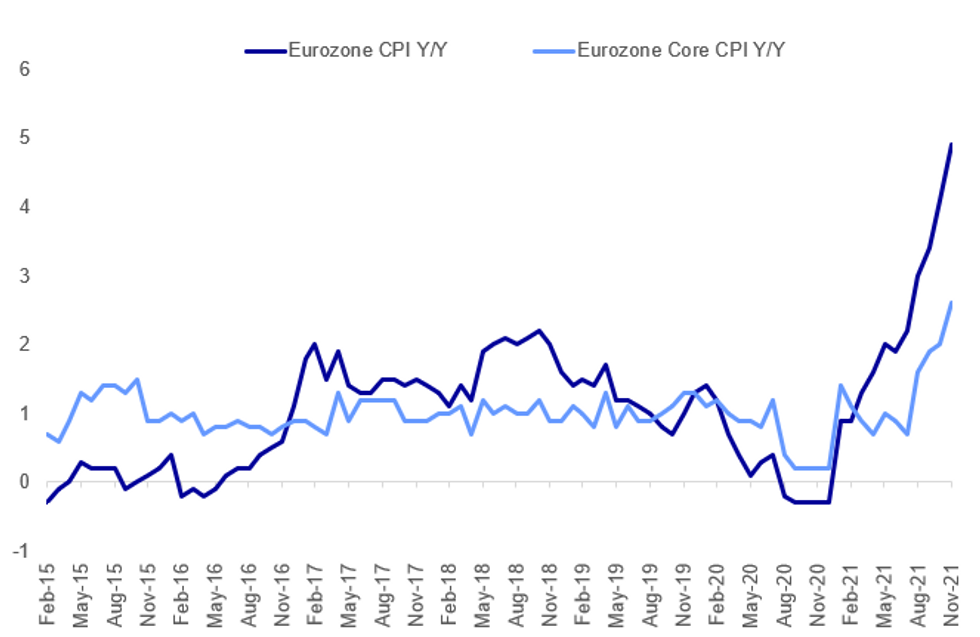

Fig.1: Eurozone Inflation Near 30-Yr High In November

Source: Eurostat, MNI

Source: Eurostat, MNI

NEWS:

EU / COVID (BBG): The European Medicines Agency (EMA) could be in a position to approve new versions of the vaccines to address the Omicron variant within three to four months, Emer Cooke, the agency’s director, told the European Parliament on Tuesday. “We think that the time from, we could be in a position that were there a need to change the vaccines, we could be in a position to have those approved within three to four months,” said Cooke adding that a lot of the work would need to take place at the company-level stage.

COVID / MODERNA (FT/BBG): Existing vaccines will be less effective at tackling Omicron than earlier strains of Covid-19 and it may take months before pharmaceutical companies can manufacture new variant-specific jabs at scale, Moderna Chief Executive Stephane Bancel said in an interview with the Financial Times. The high number of Omicron mutations on the spike protein, which the virus uses to infect human cells, and the rapid spread of the variant in South Africa, suggested the current crop of vaccines may need to be modified next year, Bancel told the newspaper. “There is no world, I think, where [the effectiveness] is the same level... we had with Delta,” he told the Financial Times in an interview at the company’s headquarters.

GERMANY / COVID (BBG): Germany’s incoming vice chancellor called for a nationwide “lockdown for the unvaccinated,” the latest sign of tougher restrictions sweeping across Europe to check the latest surge in Covid-19 infections.Ahead of pandemic talks on Tuesday between German federal and regional officials, Robert Habeck, a co-leader of the Greens, said only people who are inoculated or recovered should be allowed into non-essential stores and “public settings” across the country, rather than just in virus hotspots.Robert Habeck“We will need to face the winter with further coordinated measures,” Habeck said in an interview with ZDF television. He also raised the prospect of bringing forward or extending the Christmas school vacation.

GERMANY / COVID (AP): Germany's highest court on Tuesday rejected complaints against curfews and other restrictions imposed by federal legislation earlier this year in areas where the coronavirus was spreading quickly — a decision that could help the country's leaders as they struggle to tackle a sharp rise in infections. The ruling from the Federal Constitutional Court came hours before outgoing Chancellor Angela Merkel and her designated successor, Olaf Scholz, planned to hold talks on the situation with the country's 16 state governors.

BANK OF JAPAN (MNI INSIGHT): Bank of Japan officials are concerned the emergence of the Omicron variant of Covid-19 could impede a recovery in industrial production, exports and consumer spending, MNI understands. For full article contact sales@marketnews.com

JAPAN / COVID: Japan has discovered its first Omicron case, the Nikkei reported on Tuesday, citing a government source. A Namibian man in his 30s has been found to be infected with the heavily mutated variant after he tested positive for the coronavirus at Narita Airport, upon his arrival on Sunday, the source said. The government has decided to suspend entry into the country by foreign nationals starting Tuesday, citing the emergence of the Omicron variant of Covid-19.

GREECE / COVID (BBG): Greek Prime Minister Kyriakos Mitsotakis announced mandatory Covid-19 vaccination for all Greeks above 60 years of age before a cabinet meeting in Athens on Tuesday, in an effort to tackle the new omicron variation threat ahead of the festive season.Those who refuse to get vaccinated will have to pay a monthly fine of 100 euros ($114) for each month they don’t get jabbed, starting on Jan. 16, according to Mitsotakis. The funds collected by the fines will be given to Greek hospitals fighting the pandemic.“It is not a punishment,” Mitsotakis said. “I would say it is a health fee.”

NORWAY / COVID (BBG): Norway advises people return to using face masks again on public transport and in shops, and will now require all adults to isolate for five days if they test positive for Covid-19, regardless of vaccination status.The move extends the time that vaccinated people must remain in isolation from two days, Prime Minister Jonas Gahr Store told parliament on Tuesday. They are now also required to be fever free for 24 hours before going out again, while all adults in the same household must remain in quarantine until returning a positive test, he said.

EUROPE ENERGY (BBG): Europe’s benchmark natural gas price rose above 100 euros, or $190 per barrel of oil equivalent, ahead of a series of auctions for pipeline capacity that are seen as a test of Russia’s willingness to ease a supply crunch. The day-ahead auctions for space on Ukrainian pipelines and capacity at Germany’s Mallnow compressor station will provide a strong signal for how serious Russia is about increasing flows to the west. While the region’s biggest supplier has said it aims to keep refilling European storage sites until the end of December, it hasn’t used short-term auctions to ship more fuel.

GERMAN DATA (BBG): German unemployment extended its decline in November as businesses added staff to work off a backlog in orders.Unemployment in Europe’s largest economy fell by 34,000, beating economists’ forecast for a drop of 25,000. That pushed the jobless rate to 5.3%.

BANK OF JAPAN: The Bank of Japan said on Tuesday it has decided to keep the frequency of government bond buying operations and the scale of each bond buying operation in December unchanged from November. The BOJ will offer to buy JPY450 billion of JGBs with a remaining life of 1 to 3 years (four times), JPY450 billion of JGBs with a remaining life of 3 to 5 years (four times), JPY425 billion of JGBs with a remaining life of 5 to 10 years (four times), JPY150 billion of JGBs with a remaining life of 10 to 25 years (one time) and JPY50 billion of JGBs with a remaining life of more than 25 years (one time).

SWEDEN (BBG): Sweden’s new prime minister Magdalena Andersson has appointed Mikael Damberg to replace her as finance minister. Damberg, who has served as minister of enterprise and interior minister in Stefan Lofven’s government, had been one of the frontrunners for the post. While he is controversial among more left-leaning Social Democrats, his negotiation skills and pragmatism may be needed for Andersson’s Social Democratic government to secure center-right support.

DATA:

MNI: GERMANY NOV UE RATE (SA) 5.3%; OCT 5.4%

MNI: FRANCE NOV FLASH HICP +0.4% M/M, +3.4% Y/Y; OCT +3.2% Y/Y

MNI: SWISS NOV KOF ECON BAROMETER 108.5; OCT 110.2r

EZ NOV FLASH HICP +0.5% M/M; +4.9% Y/Y; OCT +4.1% Y/Y

EUROZONE DATA: Flash EZ inflation nears 30-year high

Eurozone inflation surged to an annual rate of 4.9% in November from 4.1% a month earlier, according to data released by Eurostat on Tuesday. The outturn far exceeding analysts’ expectations, taking inflation within spitting distance of the 5.0% pace recorded in July 1991.

- Energy prices rose by 2.9% between October and November, for an annual rise of 27.4%, far above the 17.6% increase of October. Excluding food, energy, alcohol and tobacco, core HICP rise by 2.6%, up from 2.0% in October.

- The surge in inflation has left the European Central Bank with a communications dilemma. Earlier on Tuesday, Vice President Luis de Guindos admitted that ECB -- like other forecasters --underestimated inflation developments in 2021. “The outlook for price developments isn’t entirely clear,” he told the French newspaper Les Echos, adding that prices pressures should “fade next year.”

- Tuesday’s release is the final HICP reading before the ECB next announces a policy decision on 16 December.

FIXED INCOME: What's happening with curves? Omicron vs Inflation

The morning session has seen a distinct risk-off feel with core fixed income higher across the board let by Treasuries. Against this backdrop we have also seen French and later Eurozone HICP data, with the French data in particularly helping to slow the move higher in EGBs.

- The Treasury curve continues to bull flatten with 2-year yields down 2.4bp on the day but 10-year yields 8.1bp lower. 10-year yields are now almost 22bp lower than they were prior to Thanksgiving. The MNI Chicago PMI and Powell/Yellen's Senate testimonies will be watched later, but are likely to take a back seat to any more news on the Omicron variant.

- The German curve has also bull flattened but to a much smaller extent. Schatz yields are down 1.6bp on the day but 10-year Bund yields are 3.4bp lower. This puts 10-year Bund yields around 12bp lower than pre-Thanksgiving levels.

- Gilts have seen more of a parallel curve shift (with a flattening bias). 2-year yields are down 4.6bp on the day while 10-year yields are 5.0bp lower. 10-year gilts have split the difference between USTs and Bunds, falling around 18bp since pre-Thanksgiving levels. 2-year gilt yields have seen the biggest moves in that sector however.

- We note that 10-year Treasuries have seen the biggest moves as the Omicron variant has the ability to impact both the pace of tapering and push back rate hikes. In the UK, rate hikes have been pushed back but may ultimately still be needed given the tight labour market. While the Eurozone, the ECB were unlikely to raise rates any time soon, and the only policy impact could be to make the successor to PEPP more generous.

- Therefore, to us it makes sense that we have seen Treasuries outperform gilts which have outperformed Bunds.

FOREX: Monday's Risk Rally Reversed at Expense of AUD, CAD, NOK

- Risk sentiment took a knock during Asia-Pac hours, with Moderna's CEO pouring some water on hopes that the current suite of vaccines would retain effectiveness in the face of new variants. Equities were solid, Treasuries were bid and CHF, JPY gained at the expense of AUD, CAD and NOK.

- EUR/USD resumes the upswing seen on Friday, with the pair topping 1.1350 as markets continue to work against pricing that sees a Fed rate hike in Q3 next year. The pair's correction also runs counter to the recent multi-month trend of rising equities and rallying US yields, so could suggest further position squaring as another catalyst for the move.

- Sour oil markets continue to pressure NOK, with the currency touching its lowest level against the USD of the year, despite markets continuing to expect another rate hike from the Norges Bank at the upcoming December meeting.

- Data due Tuesday includes MNI Chicago PMI, seen moderating to 67.0 from 68.4, with Canadian monthly GDP and November US consumer confidence.

- Fed's Powell is due to make an appearance alongside Treasury Secretary Yellen, although their policy-specific commentary could be limited as they're due to be testifying on the CARES act relief program. Fed's Clarida could be of more relevance, speaking on Fed Independence at 1800GMT/1300ET.

EQUITIES: S&P Futures Testing Friday's Lows

- Asian stocks closed weaker. Japan's NIKKEI closed down 462.16 pts or -1.63% at 27821.76 and the TOPIX ended 20.13 pts lower or -1.03% at 1928.35. China's SHANGHAI closed up 1.19 pts or +0.03% at 3563.887 and the HANG SENG ended 376.98 pts lower or -1.58% at 23475.26

- European equities are headed lower again, with the German Dax down 192.31 pts or -1.26% at 15128.34, FTSE 100 down 97.32 pts or -1.37% at 7109.95, CAC 40 down 101.26 pts or -1.49% at 6776.25 and Euro Stoxx 50 down 59.38 pts or -1.44% at 4064.25.

- U.S. futures are pointing to a weak cash open, with the Dow Jones mini down 452 pts or -1.29% at 34625, S&P 500 mini down 47.75 pts or -1.03% at 4603.25, NASDAQ mini down 75.25 pts or -0.46% at 16315.5.

COMMODITIES: Gold Defies Broader Weakness

- WTI Crude down $1.75 or -2.5% at $68.25

- Natural Gas down $0.19 or -3.81% at $4.66

- Gold spot up $12.06 or +0.68% at $1793.14

- Copper down $1.1 or -0.25% at $432.45

- Silver down $0.01 or -0.04% at $22.9072

- Platinum down $17.53 or -1.81% at $958.35

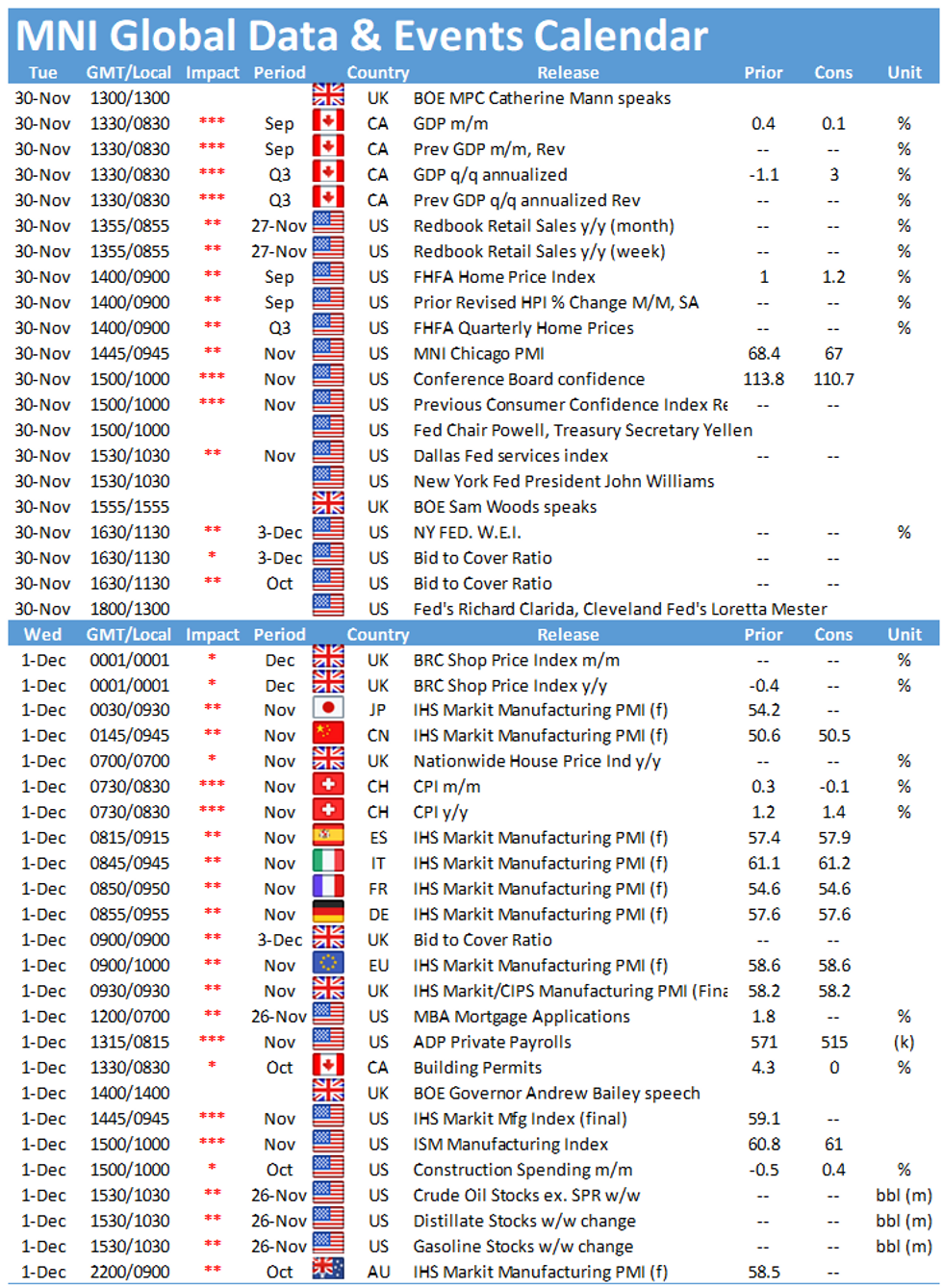

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.