Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- S&P FUTURES REGAIN LATE THURSDAY LEVELS, TSYS ALSO REVERSE LOWER

- E.U. ACCUSES U.K. OF NOT BUDGING ON KEY ISSUES, TALKS CONTINUE

- ...THOUGH E.U. AMBASSADORS TOLD "GOOD CHANCE" OF A DEAL (SKY)

- NO CHINA TIT-FOR-TAT ON NEW U.S. MOVES: ADVISORS (MNI EXCLUSIVE)

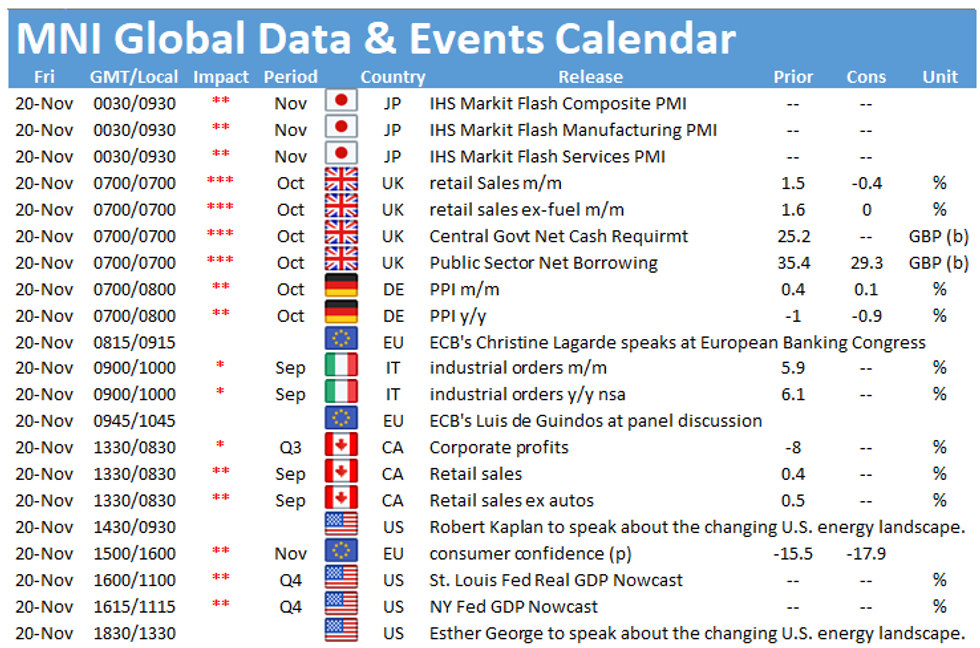

- U.K. RETAIL SALES UP MORE THAN EXPECTED IN OCTOBER

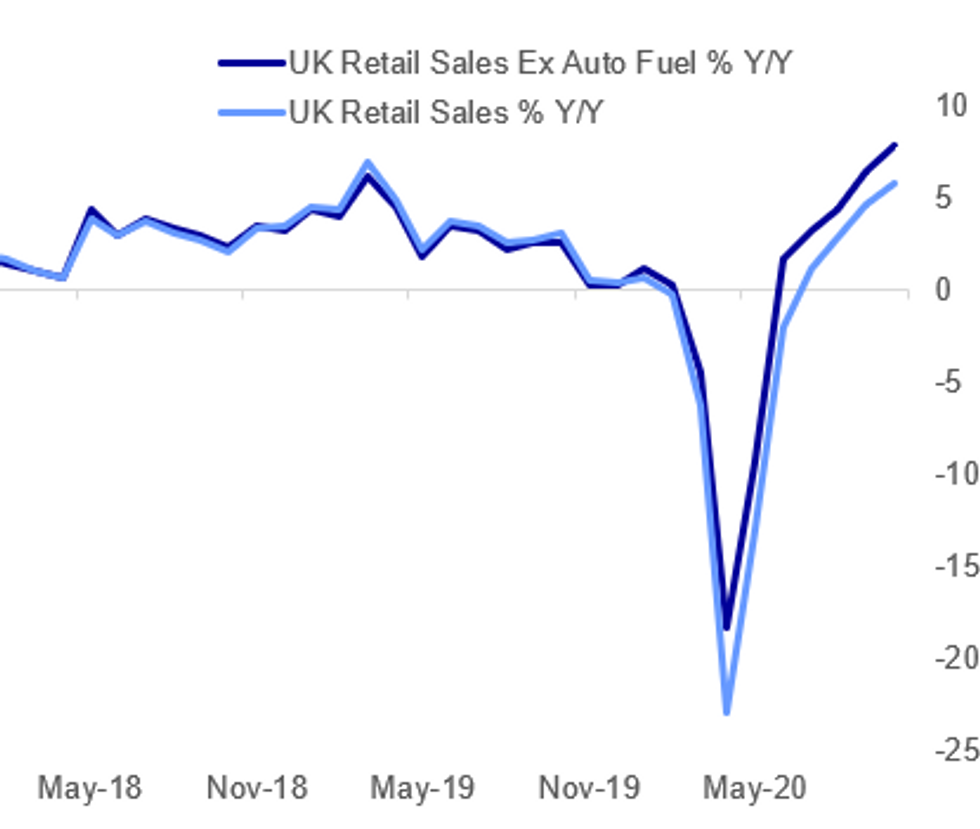

Fig. 1: U.K. Retail Sales Surprise To The Upside

ONS, BBG, MNI

ONS, BBG, MNI

NEWS:

EU-UK: European Secretary General Ilze Juhansone stepped in for chief negotiator with the UK Michel Barnier at this morning's COREPERII meeting of member state ambassadors to the EU, with the latter informed yesterday that a member of his negotiating team had tested positive for COVID-19. According to reports, Juhansone told ambassadors that all three of the primary issues (fisheries, level playing field, governance) remain unresolved. Accused the UK of not budging to allow for compromise.Says that negotiations will continue despite the positive COVID-19 case. Not clear in what format these will take place.

EU-UK: Sky's @adamparsons Tweets: "NEW: At their morning meeting, EU ambassadors were told that there is a good chance of a Brexit trade agreement subject to a political will, according to one diplomatic source."

CHINA-US: China will hold off responding to further economic sanctions from the outgoing U.S. administration, believing that Beijing is not the intended target for President Donald Trump's actions, according to policy advisors to Beijing. For full article contact sales@marketnews.com

UK DATA: Despite stricter measures to mitigate the spread of the virus, retail sales continued to increase in Oct. Sales rose 1.2%, marking the sixth consecutive month of gains, beating market forecasts expecting a decline by 0.4%. Ex-fuel sales were up 1.3% following Sep's 1.5% gain. Total sales are now 6.7% above Feb's pre-crisis level, while m/m ex-fuel sales are 8.5% higher. Oct's uptick was mainly driven by a sharp increase in non-store retailing which rose 6.4%. Moreover, household goods stores and department stores contributed positively in Oct. Clothing stores recorded a m/m decline of 1.1% after having recovered in recent months. Anecdotal evidence suggests that a reduction of footfall had impacted sales in Oct. The ONS further noted online sales were up again in Oct, while in-store sales dropped in terms value sales. Internet sales were up 4.7% on a monthly basis.

UK DATA: Year-to-date borrowing rose to GBP 214.9bn in Oct, which is GBP 169.1bn higher than in the same period a year ago and the highest borrowing in any Apr to Oct since records began in 1993. YTD borrowing was revised down by GBP15.9bn for Sep. Debt-to-GDP registered at 100.8% in Oct and ratios in recent recorded the highest levels since the 1960s. Borrowing was estimated at GBP 22.3bn in Oct which is GBP10.8bn more than in the previous year and the highest Oct borrowing on record.

GLOBAL TRADE (BBG): The World Trade Organization said the strong rebound in global trade during the third quarter may slow in the closing months of the year as nations battle a resurgence of the Covid-19 virus, according to a report issued Friday.The Geneva-based trade body's quarterly goods trade barometer rose to 100.7 last quarter, a dramatic improvement from a reading of 84.5 released in August. A level of 100 indicates growth over the next quarter that's in line with medium-term trends.

ECB: Policymakers reacted quickly and effectively to combat the short-term disruption from the Covid-19 pandemic, but the virus has 'exposed and accelerated' longer-term trends, European Central Bank President Christine Lagarde said Friday, accepting that these trends could generate significant benefits but also disruption during the transition.

BELGIUM: Belgium's consumer confidence index rises to 8-month high of minus 15 in November as households become less pessimistic about the prospects of the Belgian economy, according to emailed statement on Friday from the National Bank of Belgium.

DATA:

MNI: UK OCT CGNCR GBP14.480 BN

MNI: UK END-OCT DEBT-TO-GBP 100.8%, SEP REVISED TO 101.2%

FIXED INCOME: Brexit progress and CB speakers in focus later today

After a strong start to the morning, core fixed income markets have given up most of their gains.

- Perhaps the biggest story of the morning is a breaking news tweet from Sky News that says "EU ambassadors were told there is a good chance of a Brexit trade agreement" - this flies in the face of headlines earlier this morning that suggested little progress had been made. There continues to seem to be little progress on EU Budget negotiations, however.

- Brexit headlines will likely still be dominant (if there are any later today). The market will also focus on speeches from ECB's Weidmann and the Fed's Kaplan, Barkin and George.

- TY1 futures are up 0-2 today at 138-13+ with 10y UST yields up 1.1bp at 0.841% and 2y yields up 0.1bp at 0.164%.

- Bund futures are down -0.01 today at 175.32 with 10y Bund yields down -0.1bp at -0.573% and Schatz yields down -0.5bp at -0.747%.

- Gilt futures are up 0.01 today at 134.95 with 10y yields down -0.1bp at 0.321% and 2y yields up 0.1bp at -0.32%.

FOREX SUMMARY

EUR has seen broader base selling during our early European session.

- The currency touched low of the session against USD, GBP, CNH, CAD, JPY, AUD and is underperforming against all majors besides the SEK

- GBP came under early pressure following report that EU envoys briefed that the UK hasn't moved on 3 main hurdles.

- Cable moved from 1.3269 down to 1.3251, but since recovered after a round of Equity buying hit our screens, with the move higher related to index option expiry.

- Cable is back at 1.3272 at the time of typing

- AUDNZD resumed its downside momentum through lowest levels seen since April 2018, but failed to break the psychological 1.0500 area.

- Looking ahead, we have no data of note, although we still have few more speakers scheduled, including ECB Weidmann, and Fed Kaplan, Barkin and George.

- ALL EYES remains squarely on Brexit, Covid, and US Election certification count going into next week

EQUITIES: On The Front Foot

U.S. futures have regained the ground lost late in Thursday's session (after Treas Sec Mnuchin announced the intention to end key COVID lending programs at year-end).

- Asian stocks closed mixed, with Japan's NIKKEI down 106.97 pts or -0.42% at 25527.37 and the TOPIX up 0.98 pts or +0.06% at 1727.39. China's SHANGHAI closed up 14.639 pts or +0.44% at 3377.727 and the HANG SENG ended 94.57 pts higher or +0.36% at 26451.54.

- European equities are higher, with the German Dax up 42.81 pts or +0.33% at 13141.86, FTSE 100 up 41.62 pts or +0.66% at 6369.18, CAC 40 up 29.31 pts or +0.54% at 5498.62 and Euro Stoxx 50 up 14.62 pts or +0.42% at 3471.92.

- U.S. futures are down slightly, with the Dow Jones mini down 65 pts or -0.22% at 29378, S&P 500 mini down 6.5 pts or -0.18% at 3573.5, NASDAQ mini down 4.5 pts or -0.04% at 11982.75.

COMMODITIES: Copper Leads Broad Gains

Commodities are up across the board today with a risk-on cross-market tone prevailing and the USD trading mixed.

- WTI Crude up $0.02 or +0.05% at $41.76

- Natural Gas up $0.03 or +1.16% at $2.623

- Gold spot up $0.85 or +0.05% at $1867.54

- Copper up $3.6 or +1.12% at $325.6

- Silver up $0.14 or +0.59% at $24.1983

- Platinum up $2.36 or +0.25% at $955.39

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.