Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

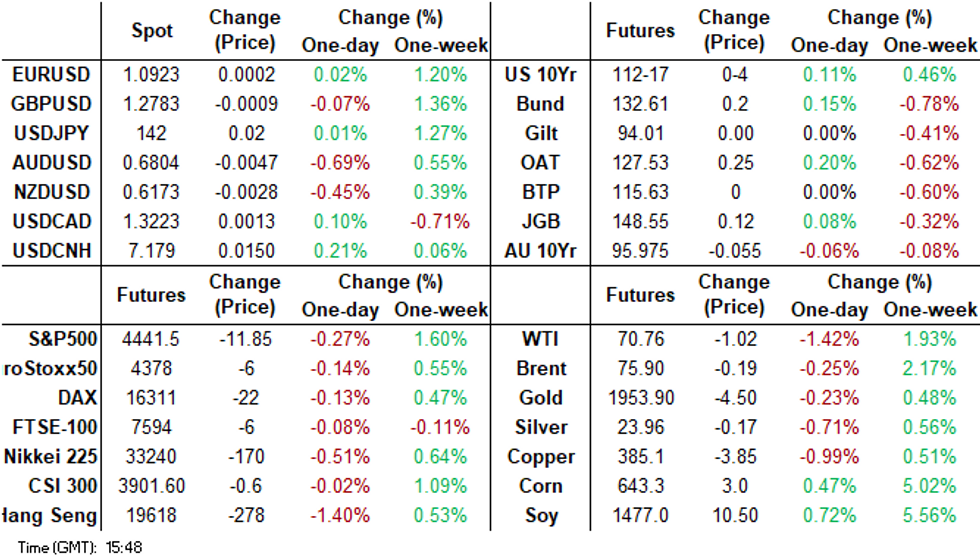

- Despite the RBA minutes not showing explicit dovishness, market sentiment appears to have been influenced by subtle changes in wording regarding the necessity of additional tightening, along with the finely balanced decision on whether to raise interest rates or maintain the status quo. ACGBs are currently sitting in the middle of the Sydney session’s range (YM flat & XM -5.0) after the initial favourable response to the release of the June RBA Minutes faded.

- The AUD is the weakest performer in the G-10 space at the margins on Tuesday. After weakening post the RBA-minutes AUD extended losses as risk off flows weighed. Support at $0.6810, high from May 10, was breached and the AUD/USD prints a touch above $0.68. Iron Ore and Copper are weaker also weighing on the AUD. The next support level is $0.6727 the low from 12 June.

- Most regional markets are tracking lower in the first part of Tuesday trade. China LPR cuts have failed to generate positive sentiment, although they had been well anticipated by the market. The 10bps cut to the 5yr LPR was less than the consensus expected (-15bps forecast), although it was a close call. USD/CNH got back above 7.1800, but remains sub recent cyclical highs.

- Looking ahead, the Fed’s Bullard, Williams and Barr speak later. There are also US May housing starts & permits data plus Philly Fed non-manufacturing activity for June. ECB’s De Guindos also speaks.

MARKETS

US TSYS: Marginally Cheaper In Asia

TYU3 deals at 112-28+, -0-05, a 0-07+ range has been observed thus far.

- Cash tsys sit 2-4bps cheaper than Friday's closing levels across the major benchmarks, the curve has bear steepened. Cash US markets were closed yesterday for the observance of a US holiday.

- Tsys firmed off session lows, on spillover from ACGB's rallying after the RBA minutes of the June policy meeting.

- The move didn't follow through and tsys ticked away from session highs, holding marginally cheaper.

- Flow wise a block buyer in TU (2k lots) was the highlight.

- There is a thin docket in Europe today. Further out we have Housing Starts and Philadelphia Fed Non-Mfg. Fedspeak from St Louis Fed President Bullard, NY Fed President Williams and VC Barr will cross.

JGBS: Futures Holding Morning Gains, Narrow Afternoon Range

JGB futures are holding firmer at 148.57, +14 compared to the settlement levels, after strengthening in morning Tokyo trade after the latest data from Japan Securities Dealers revealed trust banks had bought a record amount of super-long JGBs last month as speculation of a possible tweak to the BoJ’s yield-curve control policy receded. JBU3 reached a session high of 148.69.

- There hasn’t been much in the way of domestic drivers to flag, outside of the JSDA announcement.

- The local data calendar saw April Industrial Production (Final) print +0.7% m/m versus -0.4% prior. April Capacity Utilisation rose 3.0% versus +0.8% in March. The final May Machine Tool Orders are due to print at the top of the hour.

- The cash JGB curve bull flattens with yield movement ranging from 0.2bp lower (2-year zone) to 1.8bp lower (30-year zone). The benchmark 10-year yield is 1.0bp lower at 0.390%, below the BoJ's YCC limit of 0.50%.

- The 5-year benchmark is underperforming on the curve ahead of supply later in the week with the yield 0.2bp lower at 0.078%.

- The swap curve has also bull flattened with swap spreads tighter across the curve.

- The local calendar tomorrow sees the BoJ Minutes of the April meeting.

AUSSIE BONDS: Richer After RBA Minutes But Off Best Levels

ACGBs are currently sitting in the middle of the Sydney session’s range (YM flat & XM -5.0) after the initial favourable response to the release of the June RBA Minutes faded. Currently, 3-year and 10-year futures are 6bp and 3bp firmer post-Minutes after being as much as +11bp and +7.5bp at one stage.

- Despite the RBA minutes not showing explicit dovishness, market sentiment appears to have been influenced by subtle changes in wording regarding the necessity of additional tightening, along with the finely balanced decision on whether to raise interest rates or maintain the status quo. The surge in pricing can also be attributed to an oversold condition for futures prior to the release.

- RBA Deputy Governor Bullock has just addressed the AIG in Newcastle. Her speech was focused on recent labour market developments.

- The 3/10 cash curve has twist steepened with pricing 1bp richer to +5bp cheaper.

- Swaps are flat to 5bp higher on the day.

- Bills strip steepens with pricing -1 to +3.

- RBA dated OIS pricing is 2-5bp softer across meetings with November leading.

- The local calendar is light tomorrow with Westpac-MI Leading Index as the highlight.

- The AOFM plans to sell A$700mn of the 3.50% 21 December 2034 bond tomorrow.

RBA: Tightening Bias Retained As Persistent Inflation Risk Rises

In June the RBA discussed both a 25bp hike and a pause and while the decision was again “finely balanced”, the “stronger” arguments were for another rate rise. As mentioned in the meeting statement, upside inflation risks and not meeting the target by mid-2025 were the drivers of the June decision. May labour market data was very tight, the other key variables before the July 4 meeting are May CPI on June 28 and retail sales June 29 with Q2 services prices not until July 26.

- The meeting minutes were generally hawkish with the discussion of a hike described before the pause (unlike May), upside inflation risks firmly stated, little spare capacity, reduced risks to global growth and achieving target “drawn out”. While the concluding paragraph removed “further increases in interest rates may still be required”, it added the Board’s “willingness to do what is necessary to achieve” a return to target. The RBA will hike again if it believes it must to achieve its inflation forecast.

- Indexing of wages and prices to the CPI along with sticky services inflation seemed to drive the RBA’s assessment of increased risks to inflation, and thus expectations and rates. Wages can increase in line with inflation only if productivity picks up. Also, there were yet to be signs of easing services inflation and goods prices had moderated less than some other countries.

- Rising house prices were seen to temper the consumer slowdown “in the coming year” and stable home loan approvals indicated that financial conditions may not be as tight as previously thought.

- The arguments to pause tightening included downside risks to inflation from weaker consumption and global markets/shipping, time to assess impact of hikes to date given lags & refis, consumption has slowed significantly and market inflation expectations are little changed.

AU RATES: AU-NZ 10-Year Differential Reverts As Market Prices RBA Catch-Up

Today, the NZGB 10-year yield has increased by 4bp. However, NZGBs have still demonstrated stronger performance compared to ACGBs, as evidenced by the 2bp widening of the AU/NZ 10-year yield differential. This follows a widening of 5bp observed yesterday.

- At -42bp, the AU/NZ 10-year yield differential is currently standing at a five-month high.

- In early March, the AU-NZ 10-year yield differential narrowed to -100bp, its lowest level since the late 1990s on the back of a worse-than-expected deterioration in NZ’s current account deficit and the resultant S&P bond ratings comments.

- The recent movement in the market can be attributed to the diverging expected rate paths for the RBNZ and the RBA. The market is adjusting its pricing to reflect the anticipation of the RBA catching up to the rate hikes that have already been implemented by the RBNZ.

Figure 1: AU/NZ 10-Year Yield Differential Vs. 1Y3M Swap Differential

Source: MNI – Market News / Bloomberg

NZGBS: Weaker On The Day But Richer After RBA Minutes

NZGBs closed 3bp weaker, but off session cheaps as ACGBs positive reaction to the release of the June RBA Minutes crossed the Tasman. Australian market sentiment was influenced by subtle changes in wording regarding the necessity of additional tightening, along with the finely balanced decision on whether to raise interest rates or maintain the status quo. The NZ/AU 10-year yield differential was unchanged on the day at +43bp, a five-week low.

- Swap rates closed 2-3bp higher with implied swap spreads little changed.

- RBNZ dated OIS pricing closed 1-2bp firmer for meetings beyond November. Terminal OCR expectations closed at 5.60%.

- The government wants to help Kiwibank to continue to be a disruptor in NZ’s banking market, Finance Minister Grant Robertson told reporters Tuesday in Wellington. (See link)

- Later today sees the results of the Global Dairy Trade Auction. The last result was -3.0% reflecting strong NZ autumn supply and soft Chinese demand.

- The US calendar is slated to release May Housing Starts and Building Permits.

NZ RATES: NZ-UK 10-Year Yield Differential Turns Negative Again

The NZ-UK 10-year yield differential has turned negative, marking the first occurrence since the UK market turbulence in September/October 2022, which coincided with Liz Truss serving as Prime Minister.

- Yesterday, UK interest rates continued their steady ascent, primarily driven by the short end of the yield curve. The 2-year gilt yield experienced an increase of 14bp, while the 10-year rate saw a rise of 8bp.

- Consensus expects another strong UK CPI print (Wed) and a hawkish 25bp hike from the BoE (Thu).

- The recent development in the 10-year yield differential can be attributed to the diverging expected rate paths of the RBNZ and the BoE. The BoE is catching up to the rate hikes that have already been implemented by the RBNZ. Presently, the BoE's official bank rate stands at 4.50% compared to the RBNZ's OCR of 5.50%.

Figure 1: NZ-UK 10-Year Yield Differential

Source: MNI – Market News / Bloomberg

FOREX: AUD Pressured In Asia

The AUD is the weakest performer in the G-10 space at the margins on Tuesday. After weakening post the RBA-minutes AUD extended losses as risk off flows weighed.

- Support at $0.6810, high from May 10, was breached and the AUD/USD prints a touch above $0.68. Iron Ore and Copper are weaker also weighing on the AUD. The next support level is $0.6727 the low from 12 June.

- Kiwi is also pressured, NZD/USD is down ~0.4%. The pair sits a touch above session lows, bears target the 20-Day EMA at $0.6159.

- Yen is marginally firmer, USD/JPY briefly dealt about ¥142 handle before paring gains and grinding lower through the session. The pair last prints at ¥141.70/80.

- Elsewhere in G-10, NOK and SEK are both down ~0.4% however liquidity for both is generally poor in Asia.

- Cross asset wise; e-minis are ~0.2% lower and the Hang Seng is down ~1.6%. BBDXY is up ~0.1%. The Bloomberg Commodity Index is down ~0.4%.

- The data calendar is light today, German PPI headlines in Europe. Further out we have US Housing Starts and Philadelphia Fed Non-mfg Index.

EQUITIES: China LPR Cuts Fail To Lift Broader Sentiment

Most regional markets are tracking lower in the first part of Tuesday trade. China LPR cuts have failed to generate positive sentiment, although they had been well anticipated by the market. EU equities were weaker on Monday trade, while US futures are in the red by -0.20-0.25% at this stage. Eminis were last near 4443. These trends have also weighed on regional sentiment.

- Mainland bourses are close to flat at the break, the CSI 300 near 3931 in index terms. The real estate sub index is down 1.22%, now off around 3.5% since last Thursday. The 10bps cut to the 5yr LPR was less than the consensus expected (-15bps forecast), although it was a close call.

- HK shares are struggling the main HSI off by 1.53% at the break. The tech sub index off by 2.56% at this stage.

- Japan stocks are weaker, with the Nikkei 225 down around 0.40% in latest dealings. The electric appliances sector is weighing, with positive sentiment from Warren Buffett raising allocations to 5 trading houses, not enough to offset broader headwinds.

- South Korea and Taiwan stocks are also lower, but falls are fairly modest at this stage.

- Australian shares are higher, the ASX 200 last up 0.90%, with banks and mining leading the gains. Lower yields, which has weighed on the AUD post the RBA minutes has aided sentiment.

- In SEA, most markets are weaker, with Thai stocks off by nearly 1%.

OIL: Crude Under Pressure As Market Focuses On Lack Of China Stimulus

Oil prices are down again during APAC trading as risk appetite remained soft due to the lack of China stimulus details. WTI is 0.5% lower at $71.16/bbl and Brent -0.2% to $75.94. Both are off their intraday lows of $70.98 and $75.73 respectively. Currently WTI is down 5.7% in Q2 and Brent -4.4% despite further OPEC output cut announcements as demand concerns remain the core driver. The USD index is 0.1% higher.

- Oil has weakened again on continued concerns that measures to stimulate China’s economy will disappoint. This is important to the market as China is the largest crude importer.

- The Fed’s Bullard, Williams and Barr speak later. There are also US May housing starts & permits data plus Philly Fed non-manufacturing activity for June. ECB’s De Guindos also speaks.

GOLD: Extends Last Week’s Decline On Monday

Gold is unchanged in the Asia-Pac session, following a 0.4% decrease on Monday.

- The decline in gold prices continues as the market anticipates further monetary tightening and a decrease in safe-haven demand.

- Last week, the precious metal experienced a 0.2% decrease, reflecting indications that both the US Fed and the ECB are likely to continue raising interest rates. This trend negatively affects gold, which does not offer interest-bearing returns.

- During this month, the price of gold has been trading within the range of $1,925 and $1,985 per ounce.

- Additional downward pressure on gold occurred on Monday after a meeting between Chinese President Xi Jinping and US Secretary of State Antony Blinken, which raised hopes of improved stability in the relationship between the two countries. Gold is often sought as a hedge against geopolitical tensions.

INDONESIA: Indonesia Macro Outlook - Next Move Rate Cut, IDR Best Performer In EM Asia, But Not Cheap

- BI has paused its tightening cycle and the discussion is now on the first easing but FX stability will be a key condition as well as low inflation and a weakening economy. A signal that the Fed has reached its terminal rate is probably also needed, so that the Indonesian-US rate differential doesn't go negative.

- Market expectations look for a resilient backdrop to continue, although the current account is forecast to slip into deficit next year, in line with a terms of trade peak. We should stay away from historical wides though. Market expectations of firmer IDR levels is likely to rest on lower Fed rates in 2024.

- BI will likely guard against excessive weakness though, with USDIDR moves above 15400 (2023 highs) likely to draw selling interest at the market positions for easier global policy settings in 2024.

- See full chartbook here.

ASIA FX: USD/CNH Continues To Rebound, USD/IDR Above 15000, Won Outperforms

USD/Asia pairs are higher, with the exception of the Korean won, which has seen fresh outperformance. USD/CNH is back to 7.1800, amid disappointment on today's LPR cuts. USD/TWD is threatening to break above its 200-day MA, while in SEA most FX is weaker, except for THB. Still to come is Taiwan export orders, while tomorrow first 20-days trade data for June is due in South Korea.

- USD/CNH sits just below session highs, last near 7.1800 (highs of 7.1853 were printed earlier). CNH has faltered on broader USD strength, coupled with some disappointment around the 10bps cut in the 5-yr LPR rate (with some in the market looking for a 15bps cut). Onshore equities are weaker, albeit modestly.

- The won is outperforming so far today. Spot is back to around the 1281 level, while the 1 month NDF sits sub 1279 in latest dealings. Earlier highs were around the 1282.60 level in the 1 month NDF. There doesn't appear an obvious catalyst for won gains, although it does continue the June trend of won outperformance.

- USD/TWD is sitting at multi-week highs, last at 30.865. This is right on the 200-day MA, which we haven't spent too much time above since mid March. The 1 month NDF has already breached this resistance point and is back at highs to Nov last year (last 30.965). TWD's sensitivity to CNY moves is on display, with renewed weakness in the yuan hurting sentiment, while onshore equities are weak as well. Still, the wedge between local equities and TWD remains large, with the currency not benefiting to any great degree during the tech led bull run from mid May to mid June.

- USD/IDR is higher, last near 15050 in spot terms, around 0.35% weaker versus Monday closing levels. We did see bond outflows at the end of last week, and coupled with broader equity market jitters are likely weighing. We are now through the simple 100-day MA (15017.6), while late March levels may be in focus around 15120 in terms of next upside target. IDR is unwinding some outperformance from this year, but we expect BI to curb weakness. See our full update here.

- USD/INR is ~0.3% firmer as the Rupee softens in early trade. The pair last prints at 82.15/82.20. The broader USD/Asia move has weighed on the Rupee in early dealing; the pair is above the 82 handle for the first time since Thursday.

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing, the measure remains well within recent ranges. We now sit ~0.6% below the upper end of the band. USD/SGD has ticked away from session highs in recent dealing, the pair faced resistance at the 20-Day EMA ($1.3429), and now sits little changed from yesterday's closing levels at $1.3410/20. A reminder that the local docket is empty until Friday's CPI print. Headline CPI is expected to fall to 5.4% Y/Y from 5.7%, and Core CPI is also expected to tick lower to 4.7% Y/Y from 5.0%.

- The Ringgit has weakened to its lowest level since November 11 2022, as USD/MYR follows the broader USD/Asia move in early dealing. The pair has marginally ticked away from session highs and we sit ~0.2% firmer today. May Trade Balance printed at MYR15.42, an MYR13.40bn surplus had been expected.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/06/2023 | 0600/0800 | ** |  | DE | PPI |

| 20/06/2023 | 0800/1000 | ** |  | EU | EZ Current Account |

| 20/06/2023 | 0900/1100 | ** | | EU | Construction Production |

| 20/06/2023 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 20/06/2023 | 1030/0630 |  | US | St. Louis Fed's James Bullard | |

| 20/06/2023 | 1230/0830 | *** | | US | Housing Starts |

| 20/06/2023 | 1230/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 20/06/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 20/06/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 20/06/2023 | 1700/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 20/06/2023 | 1710/1910 | | EU | ECB de Guindos Remarks at German Bernacer Prize |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.