Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

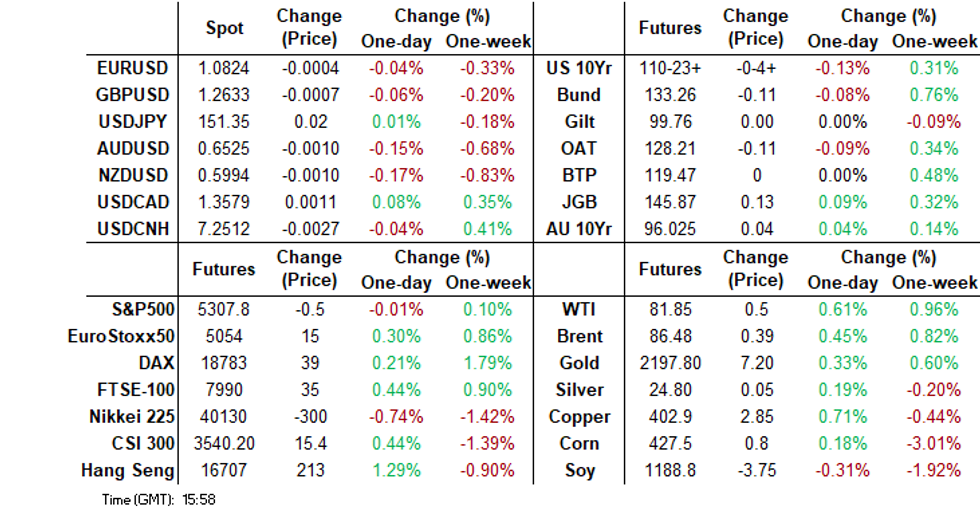

- US Jun'24 10Y gapped lower this morning as Fed Reserve Gov Waller spoke where he mentioned the Fed should wait to see more data before cutting rates. US Tsy yields sit 0.5-4bps higher across the major benchmarks, led by the front end.

- The USD spiked higher but there wasn't much follow through. Better China/HK equity sentiment has helped temper USD gains. NZD/USD did hit fresh YTD lows with weaker consumer and business confidence readings weighing. USD/JPY has been relative steady, as the market assesses intervention risks.

- Looking ahead, German retail sales figures are out. Later in the day, final readings for Q4 US GDP, initial jobless claims, MNI Chicago PMI and pending home sales are all scheduled, alongside Canada January GDP.

MARKET

TSYS: Treasury Futures Edge Lower, Curve Bear-Flattens

- Jun'24 10Y gapped lower this morning as Fed Reserve Gov Waller spoke where he mentioned the Fed should wait to see more data before cutting rates. Futures have continued to edge lower reaching a low of 110-20+, before recovering some of those loses to trade at 110-23+ down - 04 since NY closing.

- Looking at technical levels: Initial support lays at 110-08+ (Mar 21 low) while below here the 109-24+ (Mar 18 low/ the bear trigger), further down 109-14+ (Nov 28 low). While to the upside resistance holds at 110-30+ (Mar 21 & 22 high), above here 110-31+ (50-day EMA), while a break above here would open a retest of 111-24 (Mar 12 high).

- US Credit Rating Affirmed at AA+ by S&P With Stable Outlook

- Cash Treasury curve has bear-flattened on Thursday with the 2Y yield +3.9bps at 4.608%, 10Y +1.6bps to 4.206%, while the 2y10y -2.355 at -40.355.

- Thursday Data Calendar: Weekly Claims, GDP, PCE, PMI, UofM Sentiment.

JGBS: Twist-Flattener, Heavy Local Calendar Tomorrow Incl Tokyo CPI & 2Y Supply

JGB futures are stronger and at session highs, +17 compared to the settlement levels, after more than reversing the gap lower that followed the release of the BoJ Summary of Opinions for the March MPM.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined BoJ Summary of Opinions (March MPM) and Weekly International Investment Flows.

- (Bloomberg) -- Japanese bonds suffered the heaviest selling by foreign investors in more than a year last week, as the country’s central bank raised its short-term policy rate for the first time in 17 years. (See link)

- This morning’s BoJ Rinban operations saw negative spreads and lower offer cover ratios (3-5-year: 1.43x, 5-10-year: 1.49x and 10-25-year: 2.52x). This appeared to generate some support in the early rounds of the Tokyo afternoon session.

- The cash JGB curve has twist-flattened, pivoting at the 2s, with yield movements bounded by +1.2bps (1-year) and -4.4bps (40-year). The benchmark 10-year yield is 1.8bp lower at 0.707% versus the YTD high of 0.801%.

- Swap rates are mostly lower. Swap spreads are tighter out to the 10-year and wider beyond.

- Tomorrow, the local calendar sees Tokyo CPI, Jobless Rate, Job-To-Applicant Ratio, Retail Sales, Industrial Production and Housing Starts data, along with 2-year supply.

AUSSIE BONDS: Slightly Richer After A Mixed Domestic Data Drop

ACGBs (YM +2.0 & XM +3.0) are holding slightly firmer going into the Easter long weekend. Today’s mixed result domestic data drop (Retail Sales, Consumer Inflation Expectations, Private Sector Credit and Job Vacancies) failed to be a market mover.

- (AFR) There is a lot of complaining about the Reserve Bank of Australia’s 13 interest rate rises. But remarkably, there is little serious financial stress among mortgage holders after more than 4 percentage points of cash rate rises since May 2022. (See link)

- Today’s came despite cash US tsys cheapening 1-5bps in today’s Asia-Pac session following aftermarket comments from the Federal Reserve Governor Waller.

- Fed Waller said the Fed should wait a "couple months" to get a better understanding of the trajectory of inflation. (See MNI link)

- Cash ACGBs are 2-3bps richer, with the AU-US 10-year yield differential unchanged at -24bps.

- Swap rates are 2-3bps lower.

- Bills are slightly mixed across the strip.

- RBA-dated OIS pricing is slightly mixed across meetings. A cumulative 38bps of easing is priced by year-end.

- The local market is closed until next Tuesday for the Easter long weekend.

- Later today, the US calendar sees Weekly Claims, GDP, PCE, PMI and UofM Sentiment.

AUSSIE BONDS: AU-US 10-Year Yield Differential In The Bottom Half Of Range

Today, the AU-US 10-year cash yield differential has increased by 1bp to -23bps ahead of the Easter long weekend.

- At -23bps, the cash AU-US 10-year yield differential currently sits in the bottom half of the range of +/-30bps which has been observed since November 2022.

- A simple regression of the AU-US cash 10-year yield differential against the AU-US 1Y3M swap differential over the current tightening cycle indicates that the 10-year yield differential is currently 15bps too low versus its fair value (i.e., -23bps versus -8bps).

- The 1y3m differential is a proxy for the expected relative policy path over the next 12 months.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: MNI – Market News / Bloomberg

AUSTRALIAN DATA: MI Inflation Expectations Continue Trending Lower

Melbourne Institute inflation expectations had been at 4.5% for the three months to February but eased to 4.3% in March, its lowest since August 2021. Wages are expected to rise 1.2% over the coming year. The continued easing in inflation expectations is good news for the RBA but given the pickup in February services inflation, the April 24 Q1 CPI data will be watched closely.

- The Westpac consumer sentiment survey pointed out that while inflation remains the main concern of household, news items are being viewed as unfavourable by fewer people.

- Monthly inflation prints have also been surprising to the downside just above the top of the RBA’s band. Rates on hold since November are also likely reassuring people that inflation is returning to target.

- The increase in petrol prices over the first few weeks of March didn’t seem to have an impact likely helped by falling 1.1% last week.

Source: MNI - Market News/Refinitiv/ABS

AUSTRALIAN DATA: Underlying Retail Sales Weak

Retail sales in February rose 0.3% m/m, slightly less than expected, to be up 1.6% y/y after +1.1% m/m and 1.2% y/y in January. Spending remains soft though looking through recent volatility and 3-month momentum continued to deteriorate and is now negative. February was boosted by Taylor Swift’s concerts which drove a 4.2% m/m and 0.5% m/m increase in clothing & footwear and restaurant & café sales respectively. Trend retail sales rose 0.1% m/m and household goods fell 0.8% also indicating soft underlying consumption. Recent robust spending on eating out and big events show that people are still prepared to consume for special occasions.

Australia retail sales $mn

Source: MNI - Market News/ABS

NZGBS: Closed Richer Ahead Of Easter Weekend Despite A Cheapening In US Tsys

NZGBs closed 3bps richer and just off the session's best levels. This came despite cash US tsys cheapening 1-4bps in today’s Asia-Pac session following aftermarket comments from the Federal Reserve Governor Waller.

- Fed Waller said the Fed should wait a "couple months" to get a better understanding of the trajectory of inflation, but he still expects the central bank to begin reducing the target range for the federal funds rate this year. (See MNI link)

- The move away from session cheaps was likely aided by decent demand metrics at today’s weekly supply. Bid cover ratios printed 2.25x to 2.92x for the Apr-29 and May-34 lines respectively.

- ANZ Business Confidence lost 11.8 points from a month earlier to 22.9 in March.

- (Bloomberg) -- NZ appointed Carl Hansen and Prasanna Gai to the Reserve Bank Monetary Policy Committee, Finance Minister Nicola Willis says in an emailed statement. (See link)

- Swap rates closed 2-5bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed 2-3bps softer for meetings beyond May. A cumulative 71bps of easing is priced by year-end.

- The local market is closed until next Tuesday for the Easter long weekend.

- Later today, the US calendar sees Weekly Claims, GDP, PCE, PMI and UofM Sentiment.

NZ DATA: Consumer Confidence Weakens As Economy Slows

ANZ Roy Morgan consumer confidence fell sharply in March by 8.6% bringing the level to its lowest in six months. Both the assessment of current and future conditions and most components were weaker. ANZ believes that the slowing economy and easing labour market as well as talk of “recession” drove the decline.

- ANZ believes that sentiment took a hit from media reports of a “recession” after Q4 GDP showed the economy had shrunk for two consecutive quarters. Responses after Q4 GDP was released on March 21 were “markedly weaker” than those from earlier in the month, but all weeks showed a decline on February.

- Inflation expectations for two years ahead were steady at 4.5% but still above pre-pandemic levels and so the RBNZ would likely want to see them fall further to ensure wage inflation follows.

- Perceptions of the economic outlook were particularly weak falling 14 points for a year ahead and 10 for 5-years. Personal finance and time to buy were also soft.

Source: MNI - Market News/Refinitiv

NZ DATA: Business Survey Signals Soft Growth, Easing Inflation Expectations

ANZ business confidence and activity outlook can be added to the list of NZ indicators slowing and like consumer sentiment took a sharper step down after the Q4 data confirmed a “technical recession”. They fell to their lowest in six months in March but remain positive. Confidence fell almost 12 points to 22.9 and the outlook 7 points to 22.5. Activity is slowing as the RBNZ wants and while inflation is easing, some survey measures remain high suggesting that it is not contained yet.

- Business inflation expectations continued to ease falling 0.2pp in March to 3.5%, the lowest since October 2021 and moving in the right direction for the RBNZ. But pricing intentions, while they continue to ease gradually, remain too high at 45.1 as business costs rose in March to 74.6, also elevated. Wage expectations were higher at 80.5 from 78.9 driven by retail and construction. Cost pressures need to ease for inflation to return sustainably to target.

- Past wage increases were steady at 4.4% y/y and expectations for the coming year eased slightly to 3.3% from 3.4%.

- Inflation-related issues are becoming less of a problem for businesses but interest rates, competition and turnover are taking over.

- Reported past activity, which ANZ says has the closest correlation with GDP, declined 2 points to -7 in March but is consistent with ANZ’s +0.2% q/q forecast for Q1. It showed stronger retail, agriculture and construction but all other sectors fell.

- In line with the sharp drop in consumer confidence, labour demand fell in March to 3.5 from 6.2, while still positive was the lowest reading since September 2023.

- Exports, investment intentions, and profit expectations are all lower.

Source: MNI - Market News/Refinitiv

FOREX: USD Index Higher, Supported By Yields, NZD Hits Fresh YTD Low

The USD index sits a touch higher for the session, the BBDXY last near 1244. The USD spiked higher at the open, amid a slump in US Tsy futures, as the Fed's Waller pushed back on early rate cuts.

- US yields are slightly off session highs but still around 1-4bps firmer across the benchmarks, led by the front end (2yr back to 4.605%).

- NZD/USD has been the weakest performer making fresh YTD lows near 0.5980. Outside of the US yield move we have seen quite soft consumer and business sentiment readings, pointing to a weaker economic backdrop.

- AUD/USD is also lower, but only marginally. The pair last near 0.6530/35. A rebound in HK/China equity sentiment (post yesterday's President Xi meeting with US executives) has helped.

- USD/JPY has tracked recent ranges, last near 151.35/40. The BoJ Summary Of Opinions largely in line with recent BoJ rhetoric. We did see the cabinet secretary also warn around excessive yen moves, but this was in line with recent comments by the FinMin.

- Looking ahead, German retail sales figures are out. Later in the day, final readings for Q4 US GDP, initial jobless claims, MNI Chicago PMI and pending home sales are all scheduled, alongside Canada January GDP.

CHINA & HK EQUITIES: HK & China Equities Head Higher, Markets Awaits Property Results

Hong Kong and China equities are higher today, with tech names surging higher to be the top-performing sector. There is a raft of corporate earnings due out today, following on from a busy day on Wednesday the major focus today is the property names including China Vanke and Country Garden, while some of China's largest banks have reported an increase in bad loans due to the prolonged property downturn. Elsewhere President Xi met with US CEOs where he pitched China as a good investment, the US has asked allies to tighten servicing of chip gear in China.

- Hong Kong equities are higher today, with HSTech Index the top performer up 3.65%, the Mainland Property Index opened down 2.00%, however has recovered all of those loses to now trade up 1.35%, HSI is up 1.63% while the HS China Enterprises is up 2.20%. In China, equities markets are lagging the moves by HK listed stocks the small-cap CSI1000 up 2.82%, ChiNext up 1.88%, while the large-cap CSI300 is up 1.22%

- China Northbound flows were -7.2billion yuan on Wednesday, with the 5-day average at -1.22billion, while the 20-day average sits at 1.81 billion yuan.

- In the property space, Sunac China FY revenue beats estimates, while Country Garden Services reported a 85% slump in net income for 2023. China's largest state-owned banks, including Bank of Communications and Industrial & Commercial Bank of China, are experiencing an increase in bad loan ratios due to the prolonged property downturn, with pressure to maintain asset quality amidst sluggish home sales and developer liquidity. Despite scant profit gains and narrowing interest margins, their resilience in the face of a slowing economy heavily reliant on bank lending remains a focal point for investors.

- Chinese President Xi Jinping met with American business leaders, including figures from companies like Blackstone and Qualcomm, aiming to restore confidence in China's economy and maintain stable relations with the US. Xi emphasized the importance of cooperation between the two countries while addressing concerns about domestic economic issues and geopolitical tensions, amidst ongoing disputes and uncertainties in US-China relations.

- The US is urging its allies to impose stricter restrictions on servicing chipmaking equipment in China, as part of efforts to hinder Beijing's semiconductor development goals. American officials are particularly concerned after Huawei's recent launch of a 5G smartphone powered by an advanced Chinese-made chip, which still relied on equipment from US and Dutch suppliers. This move reflects ongoing US efforts to limit China's access to advanced technology, with Washington pressing for tighter controls on servicing equipment deployed at blacklisted Chinese entities.

- Looking ahead, Hong Kong has Budget Balance later today, while China has 4Q BoP Current Account Balance on Friday

ASIA PAC EQUITIES: Asian Equity Markets Mostly Lower, Yen Intervention Risk Grow

Regional Asian equities are mostly lower today, with Australia the top performer, the ASX hit new all-time highs despite a slowdown in retail sales in Feb, while New Zealand also rose following a drop in consumer and business confidence. Japanese markets face growing risk of government intervention in FX markets, impacting exporters. Foreign investors turn to selling regional equities as outflows increase, South Korean equities have been the exception. Malaysian & Philippines markets are closed, while most others will be closed tomorrow for Good Friday.

- In Japan, equities are lower due to rising risk of government intervention in the FX market, particularly affecting exporters. The yen remains steady at 151.36 to the dollar, with Assistant Governor Tokiko Shimizu of the Bank of Japan expecting inflation to remain around 2%, emphasizing accommodative policy and plans to maintain current JGB purchases Several companies are trading without right to the next dividend which has impacted equity prices. The Topix is down 1.34%, while the Nikkei is slightly above 40,000, down 1.22%.

- South Korean equities are slightly lower today. Finance Minister Choi Sang-mok highlighted export-driven recovery but cautioned about high prices and borrowing costs, aiming to stabilize inflation at 2%. President Yoon Suk Yeol expressed hope for the Bank of Korea's active role in financial market stabilization. The Kospi is down 0.10%.

- Taiwanese equities are lower today with foreign investor flows negative for 7 of the past 10 days. Interest rate swaps declined as the central bank hinted at holding rates in June after a March hike. CB Governor Yang Chin-long suggested unchanged rates in June if CPI stays between 2%-2.5%. The Taiex is down 0.32%.

- Australian equities made fresh all time highs earlier, touching the 7,900 mark, we closed just off those levels and up about 1% for the day. Miners and Real estate names are the top performers. Earlier, Private sector credit beat estimates at 0.5% m/m vs 0.4%m/m expected, while Retail Sales missed estimates coming in at 0.3% vs 0.4% m/m down from last month of 1.1%.

- Elsewhere in SEA, New Zealand Equities are higher, the NZD made fresh YTD lows after consumer and business confidence showed a steep drop while Singapore equities are down 0.30%, Indonesian equities are down 0.40%, Indian equities are up 0.80%, while Malaysia and Philippines equity markets are closed for the day.

JAPAN DATA: Offshore Investors Sell Local Equities For Second Straight Week, Dump Local Bonds

Offshore investors remained net sellers of Japan stocks last week. Whilst the outflows were more modest than the prior week it was still the first back to back weekly outflows since the first half of Dec last year. We are still comfortably positive in terms of year to date inflows, but momentum has clearly waned. This trend came despite the better equity backdrop into the tail end of last week.

- Offshore investors also dumped local bonds, with nearly -¥3900bn in outflows. Last week obviously marked the departure from NIPR for the BoJ. This was the largest weekly outflow since early 2023.

- In terms of Japan outbound flows, we saw a decent pick up in offshore bond flows. We saw modest outflows to global equities as well, but this is only partially offsetting the prior week outflows.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending Mar 22 | Prior Week |

| Foreign Buying Japan Stocks | -891.4 | -1461.9 |

| Foreign Buying Japan Bonds | -3892.5 | 2161.6 |

| Japan Buying Foreign Bonds | 762.3 | -818.8 |

| Japan Buying Foreign Stocks | 81.9 | -522.2 |

Source: MNI - Market News/Bloomberg

ASIA EQUITY FLOWS: Foreign Investor Equity Flow Turns Negative, SK The Exception

- China equities were lower on Wednesday led by decent sell-offs in small-cap and growth stocks. There was little in the way of economic data to drive the selling, although there was a raft of corporate earnings released with many companies missing estimates, recently the CSI300 failed to break important technical resistance, Morgan Stanley noted it also been noted that hedge funds have started to sell Chinese stocks and add short positions via Hong Kong markets and finally President Xi did meet with American Business leaders on Wednesday to try and convince them to invest into China. China equities saw an outflow via northbound connect of 7.2b yuan, the most since Jan 17th. The 5-day average is now -1.2b, the 20-day average is 1.81b while the longer term trend has fallen now at just 0.48b yuan.

- South Korean equities were a touch higher on Wednesday and the only market in the region to see inflow. This could be signs that investors have faith that the SK regulators and government can close the "Korea Discount". $257m entered the market, taking the 5-day average to $604m, the 20-day average to $191m while the longer term 100-day average is $185m

- Taiwan equities have now marked three days of net outflows, while also seeing outflows in 7 of the past 10 trading days. Government officials have been warning about equity market bubbles over the time, which may be causing foreign investors to start to trim their positions. Equity markets did however close higher. The 5-day average is now -$37m, 20-day average is $45m, both well below the longer term 100-day average of $184m

- Indonesia marked the third day of net selling, there has been questions from presidential candidates that the President elect had rigged the elections and that they want the results overturned which could be spooking some foreign investors while other have question the cost of the free meals election promise and it's impact on futures budgets. Equities were 0.75% lower on Wednesday, while the 5-day average is -8.21m, 20-day average is 20.8m inline with the 100-day average of 20.7m

- Indian equities have seen the largest outflow for the past 5 days of any other market in the region, there has been little in the way of market catalyst. The Nifity 50 bounce off the 20-day EMA. The 5-day average is now -$222m, the 20day average is $190m, well above the 100-day average of $90m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | -7.2 | -6.1 | 65.9 |

| South Korea (USDmn) | 257 | 3024 | 11536 |

| Taiwan (USDmn) | -236 | -185 | 5729 |

| India (USDmn)** | -380 | -1274 | 591 |

| Indonesia (USDmn) | -54 | -41 | 1710 |

| Thailand (USDmn) | 19 | 68 | -1901 |

| Malaysia (USDmn) ** | -7 | 88 | -99 |

| Philippines (USDmn) | -6 | -44.2 | 163 |

| Total (Ex China USDmn) | -408 | 1635 | 17728 |

| * Northbound Stock Connect Flows | |||

| *** Data Up To March 26 |

OIL: Crude Headed For Strong Q1 Rise

Oil prices are higher during APAC trading today after being little changed on Wednesday but they are off their intraday highs. Prices recovered after dipping on Governor Waller’s comments that the Fed should wait before easing. WTI is up 0.5% to $81.72/bbl after approaching $82, and Brent is 0.3% higher at $86.36 after reaching a high of $86.58. The USD index is unchanged.

- Oil prices look likely to end March around $10/bbl higher than the end of 2023 or around 13% higher. March itself probably saw an increase just over 5% on the month. Prospective Fed easing, geopolitical tensions, improved demand prospects and OPEC supply cuts buoyed prices but there remains a lot of uncertainty around China’s consumption and OPEC members’ quota compliance. Sentiment is positive going into Q2 though.

- OPEC has extended its 2mbd output cuts to end June and quotas will be reconsidered in June. Next week’s review meeting is unlikely to result in any changes, as delegates have already said that they aren’t necessary.

- The US said it destroyed 4 Houthi drones that were targeting a warship in the Red Sea.

- EIA data showed a 3.17mn barrel crude inventory build despite a small drawdown being expected, which weighed on oil prices at the start of the APAC session. Gasoline stocks increased 1.3mn barrels after drawdowns over the past weeks, but distillate fell 1.19mn. Refinery utilisation rose 0.9pp to 88.7%.

- Later final Q4 US GDP, jobless claims, March MNI Chicago PMI & Uni of Michigan consumer sentiment print.

GOLD: Third Straight Session Of Gains

Gold is unchanged in the Asia-Pac session, after closing 0.7% higher at $2194.79 on Wednesday.

- Wednesday’s move was the third straight session of gains.

- Today’s softness appears tied to aftermarket comments from the Federal Reserve Governor Waller. Fed Waller said the Fed should wait a "couple months" to get a better understanding of the trajectory of inflation, but he still expects the central bank to begin reducing the target range for the federal funds rate this year. (See MNI link)

- Cash US tsys are 1-5bps cheaper in today's Asia-Pac session.

- Bullion sits just below of its all-time high of $2200.89 ahead of Friday’s release of US PCE deflators, the Federal Reserve’s preferred inflation gauge. That said, the scope for any major surprises should be limited in Good Friday trading, with the CPI and PPI figures feeding into that release.

- According to MNI’s technicals team, sights remain on $2230.1 next, a Fibonacci projection. Key short-term trend support has been defined at $2146.2, the Mar 18 low.

USD/Asia Pairs Off Recent Highs As Month End Approaches

Most USD/Asia pairs are lower, unwinding earlier dollar gains. Downside is fairly modest at this stage though, with higher US yields (post hawkish Fed speak), providing some offset to a firmer HK/China equity backdrop. Still, only MYR has recorded a rise against the USD in March to date.

- USD/CNH is back near 7.2500, but hasn't seen much downside follow through. Spot USD/CNY is close to 7.2260, little change for the session so far. China/HK equities are up strongly, with optimism around potential further policy support after yesterday's meeting between President Xi and US business executives aiding broader sentiment.

- Spot USD/KRW is back sub 1350, we got to highs near 1353 not long after the open. Headlines cross though of exporter related USD selling, which likely helped curb gains. The 1 month NDF is back into the 1344/45 region, slightly stronger in won terms for the session. Multi-month highs in the pair may make it more attractive for exporters to convert offshore earnings ahead of month end.

- Spot USD/TWD is a touch off recent highs, last just under 32.00, likewise for the 1 month NDF.

- USD/IDR is steadier today, but not far off recent highs. We were last in the 15865/70 region. Headlines crossed yesterday that BI was in the market to stabilize FX supply and demand. Highs back to early Nov last year is likely to keep the central bank in the market in the near term. The general trend towards month end has been portfolio outflows across both equities and bonds (although bond outflows have been larger in USD terms).

- Elsewhere we are seeing fairly modest gains against the USD. USD/PHP is in the 56.20/25 region. PHP is the second best performer in March to date behind the MYR. Malaysian markets are shut today. The PHP continues to show outperformance given higher US yields and a worsening terms of trade backdrop. An elevated policy rate and declining inflation rate is likely providing some offset.

- USD/THB holds near recent highs (baht being the worst EM Asia performer in the past month). The pair is just under 36.40. Portfolio outflows remain negative for March, amid continuing growth concerns, although we have seen a more positive flow backdrop in recent sessions.

INDONESIA: Indonesian Sov Debt Curve Flattens, Bond Demand Drops

Indonesian USD sovereign debt curve is slightly flatter today, yields are 1-3bps lower. Indonesian bond demands sinks on the incoming Presidents pledge to boost spending.

- The INDON sov curve is flatter with the 2Y yield 1bp lower at 4.92%, 5Y yield is 1.5bps lower at 4.865%, the 10Y yield is 2bps lower at 4.995%, while the 5-year CDS is unchanged at 72.5bps

- The INDON to UST spread is slightly tighter in the front-end today after US Treasury curve bear steepened on Feb Gov Wallers comments earlier, the 2yr is 31bps (-3bps), 5yr is 64.5bps (-1bp), while the 10yr is 78.5bps (+1bps).

- In cross-asset moves, the USD/IDR is 0.09% higher, the JCI is 0.11% lower, Palm Oil is unchanged, while US Tsys yields are flat to 4bps higher.

- The most recent data shows an outflow of $335m on Monday. The 5-day average is now -$86m, the 20-day average is -$57m while the longer term 200-day average is -$3.10m

- (Bloomberg) -- Indonesian Bond Demand Sinks Amid Fears Over Widening Deficit (See link)

- Looking ahead: Indonesia has a very quiet rest of the month in terms of data, with the next major data release not until April 1st

PHILIPPINES: Philip Sov Debt Curve Slightly Flatter, ANZ Raises Infl Forecast

The Philippines USD sovereign debt curve is largely unchanged on Thursday, yields are flat to 2bp higher. ANZ has raised its inflations forecast for Philippines, while most of Philippines markets are closed today for Maundy Thursday.

- The PHILIP curve is largely unchanged on Thursday, out-performing the move by US treasuries, the 2Y yield is unchanged at 4.79%, 5Y yield is 0.5bp lower at 4.945%, the 10Y yield is 1bp lower at 4.98%, while 5yr CDS is 0.5bp higher at 63bps.

- The PHILIP to UST spread difference tighten in the front-end throughout the day as the US treasury yields moved higher post Waller comments this morning, the 2y is 18bps (-2bps), the 5yr is 69.5bps (-0.5bp), while the 10yr is 77bps (+1bps)

- Cross-asset moves: Philippines Markets closed, US tsys yield are flat to 4bps higher.

- ANZ Research raised its inflation forecast for the Philippines to 3.8 percent this year, citing risks that could push inflation above the central bank's target range of two to four percent. This increase, if realized, would be higher than the BSP's forecast of 3.6 percent but lower than the six percent average in 2023. ANZ highlighted the need for policy intervention in food and energy markets to address the inflationary pressures, expecting the BSP to begin easing its policy stance by December, with a 50-basis-point cut in the key rate, followed by an additional 100-basis-point reduction next year.

- Looking Ahead: Calendar is light for the remainder of the month

MARKETSUP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/03/2024 | 0700/0700 | *** |  | UK | GDP Second Estimate |

| 28/03/2024 | 0700/0700 | * | | UK | Quarterly current account balance |

| 28/03/2024 | 0700/0800 | ** |  | DE | Retail Sales |

| 28/03/2024 | 0700/0800 | ** |  | SE | Retail Sales |

| 28/03/2024 | 0800/0900 | ** |  | CH | KOF Economic Barometer |

| 28/03/2024 | 0855/0955 | ** | | DE | Unemployment |

| 28/03/2024 | 0900/1000 | ** |  | EU | M3 |

| 28/03/2024 | 0900/1000 | ** |  | IT | ISTAT Business Confidence |

| 28/03/2024 | 0900/1000 | ** | | IT | ISTAT Consumer Confidence |

| 28/03/2024 | 1100/1200 | ** | | IT | PPI |

| 28/03/2024 | 1230/0830 | *** |  | US | Jobless Claims |

| 28/03/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 28/03/2024 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 28/03/2024 | 1230/0830 | * | | CA | Payroll employment |

| 28/03/2024 | 1230/0830 | *** | | US | GDP |

| 28/03/2024 | 1345/0945 | *** | | US | MNI Chicago PMI |

| 28/03/2024 | 1400/1000 | ** | | US | NAR Pending Home Sales |

| 28/03/2024 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 28/03/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 28/03/2024 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 28/03/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 28/03/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 28/03/2024 | 1600/1200 | ** | | US | USDA GrainStock - NASS |

| 28/03/2024 | 1600/1200 | *** | | US | USDA PROSPECTIVE PLANTINGS - NASS |

| 29/03/2024 | 2330/0830 | ** |  | JP | Tokyo CPI |

| 29/03/2024 | 2330/0830 | * | | JP | Labor Force Survey |

| 29/03/2024 | 2350/0850 | * | | JP | Retail Sales (p) |

| 29/03/2024 | 2350/0850 | ** | | JP | Industrial Production |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.