Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

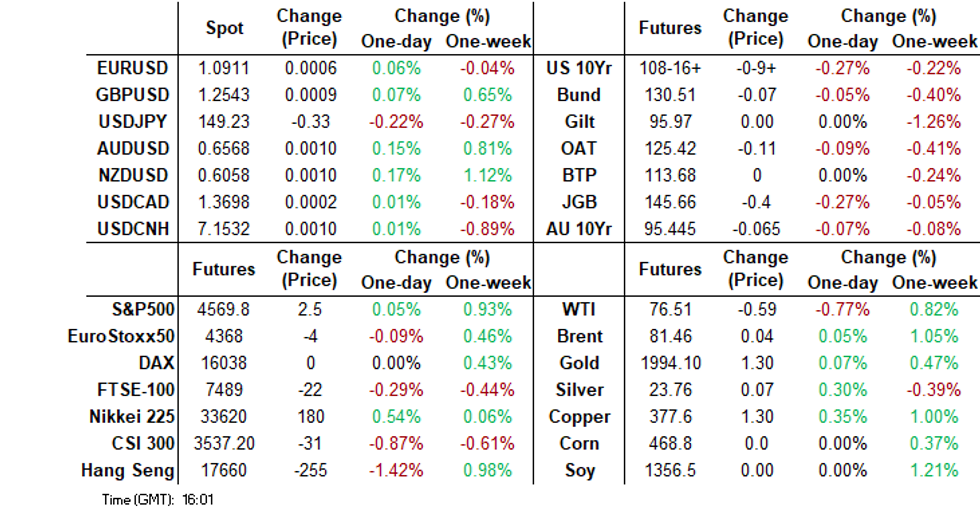

- US and Japan cash bond markets have returned, with yields higher, tracking leads from EU fixed income markets on Thursday. TY futures briefly dipped below Thursday lows. JGB futures are also lower, despite Oct CPI data missing estimates. The core details still showed a tick higher in m/m terms though.

- In the FX space, the USD/CNY fix was again set lower, but USD/CNH has consolidated, as HK/China equities have tracked lower. Other Asia FX is also weaker against the USD.

- For the majors, the USD hasn't been able to sustain upward momentum. Oil and gold have largely tracked sideways.

- Looking ahead, the docket is light in Europe today, further out we have flash US S&P Global PMIs.

MARKETS

US TSYS: Narrow Ranges, TY Breaches Thursdays Low

TYZ3 deals at 108-17, -0-09, a 0-05+ range has been observed on volume of ~102k.

- Cash tsys sit 4-5bps cheaper across the major benchmarks, the belly is leading the cheaps.

- Tsys have ticked lower through today's session, albeit in a narrow range. There was little meaningful macro news flow as Tsys reopened after light holiday trade on Thursday. The downtick was seen alongside a light bid in the USD and pressure on regional equities.

- TY has breached Thursday's lows before marginally paring gains. The short-term structure in TY remains bullish, resistance comes in at 109-08+ the Nov 17 high. The 50-Day EMA (108-05) provides support.

- The highlight flow wise was a block seller (2k lots) in UXY.

- The docket is light in Europe today, further out we have flash S&P Global PMIs.

JGBS: Futures Consolidate After Earlier Drop, 40yr Supply On Tap Next Week

Post the lunch time break, JGB futures have largely tracked sideways. We were last at 145.74, -.32, which is slightly above session lows of 145.66. Highs were near the open, coming in at 146.03.

- This mirrors US Tsy futures to a large extent, with TYZ briefly breaching Thursday lows before consolidating (last 108-16+ -09+).

- Earlier the data front delivered slightly weaker than expected Oct CPI, but with firmer m/m core trends. The manufacturing PMI softened further to 48.1, but the services PMI painted a more upbeat picture (51.7).

- In the cash JGB space, the benchmark 10yr sits slightly below session highs in yield terms, last at 0.77% (+4.5bps). Earlier lows in the week were sub 0.70%. The 20yr yield is near 1.49%, also down slightly from session highs.

- In the swap space, the 10yr is near 0.98%, +5bps.

- Next week the data calendar has retail sales, and jobless rate figures as the main focus points. Q3 Capex is also out. There is BoJ speak on Wednesday and Thursday.

- On the supply front, we have a 40yr bond sale on Tuesday.

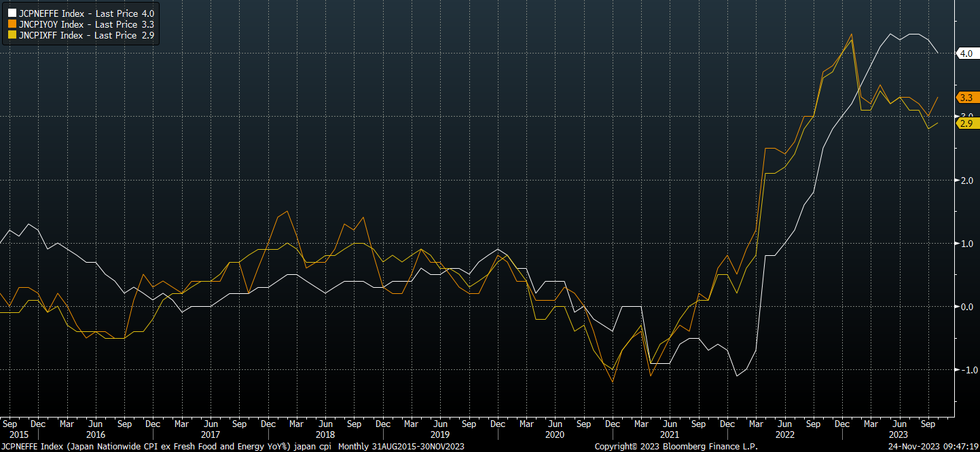

JAPAN DATA: Oct CPI Softer Than Expected, But Core M/M Numbers Firm

Japan October CPI was a touch below estimates. Core CPI ex fresh food and energy was 4.0% y/y, against a 4.1% projection and 4.2% prior. We continue to gradually move off recent highs in terms of this measure (see the chart below, with this core measure the top white line). The headline measure was also below expectations at 3.3% y/y (forecast 3.4%), but a step up from the prior pace. The ex fresh food measure was 2.9% y/y, also below expectations but slightly firming versus September.

- In terms of the detail, the core measure which excludes all food and energy ticked up to 2.7% y/y (from 2.6%), but it remains within recent ranges.

- In m/m terms this metric was +0.4% up from flat prior. Most core metrics were higher in m/m terms versus the September outcomes.

- Utility prices rose 6.0% m/m, while entertainment rose 0.9%, after both measures fell in September. Household goods inflation also firmed to 1.0% m/m.

- In y/y terms, fresh food prices spiked to 14.1% (from 9.6%), while other sub-indices were mixed. Household goods (6.9% y/y) and entertainment (6.4% y/y) saw firmer y/y momentum, but other categories were mostly softer.

Fig 1: Japan CPI Trends Mixed In October

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Cheaper, Curve Steepens on Friday

ACGBs sit 4-7bps cheaper across the major benchmarks, light bear steepening is apparent.

- XM (-0.075) and YM (-0.06) have ticked lower through todays session dealing in narrow ranges for the most part.

- RBA dated futures price a terminal rate of 4.50% in June 24 with ~15bps of cuts by Dec 24.

- There was little in the way of meaningful domestic news flow, ACGBs ticked lower in narrow ranges today alongside Global FI. There was no headline driver and the move was seen alongside a light bid in the USD and pressure on regional equities.

- Looking ahead next week we have Oct CPI provides the highlight; a downtick in CPI to 5.2% Y/Y is expected, the prior read was 5.6% Y/Y.

NZGBs: Tick Lower Through Asia, RBNZ Due Next Week

NZGBs have ticked lower through today's Asian session, however ranges have been narrow and there has not yet been much follow through on the move lower. NZGBs sit 2-6bps cheaper across the major benchmarks, light bear steepening is apparent.

- Pressure has been seen alongside an uptick in the USD and lower regional equities are weighing on sentiment.

- 10-Year NZ US Swaps are stable and well within recent ranges, last printing at +55bps.

- With next week's RBNZ Meeting in view; OIS remain stable, pricing no change in the OCR next week with ~40bps of cuts by Oct 24.

- A reminder that the NZ Government Coalition will look to narrow the RBNZ's remit to focus on price stability (BBG). PM-Elect Luxon noted that his first economic job is to get inflation controlled.

- Looking ahead, the aforementioned RBNZ monetary policy decision headlines next week's docket. Also due next week are October Building Permits, November ANZ Business Survey and Consumer Confidence.

RBNZ: New Government Considering Broader RBNZ Changes

The new NZ government, which is made up of 3 coalition partners (led by the NZ National Party, along with the NZ First and ACT parties), has announced it will consider broader changes to the RBNZ remit.

- As expected, the new government will shift the central bank back to a single mandate focused solely on price stability, removing the current dual mandate, which included employment and was introduced by the previous Labor government in 2018.

- Other changes under consideration are that the new government "will take advice on giving the RBNZ time targets for monetary policy, removing the Treasury Dept. observer from the Monetary Policy Committee and returning to a single decision maker model." (per BBG, see this link).

- The RBNZ is on the record as stating that it doesn't agree with changes to the timing around when inflation should return to the target range.

- On balance, these are hawkish developments but not completed unexpected.

- NZGBs sit 1-6bps cheaper across the major benchmarks have ticked marginally lower through the session however ranges remain narrow thus far.

NZ DATA: Q3 Volumes Better Than Expected, But Y/Y Momentum Still Weak

Q3 NZ retail sales volumes were unchanged on the Q2 outcome. This was better than the consensus expectation of a -0.7% dip. in y/y terms we were at -3.5%, only a slightly improvement on the Q2 y/y outcome at -3.5%.

- NZ Stats noted the following industries moves:

- motor vehicle and parts retailing – down 3.4 percent

- hardware, building, and garden supplies – up 2.9 percent

- fuel retailing – down 3.4 percent

- supermarket and grocery stores – up 1.0 percent

- clothing, footwear, and personal accessories – up 4.0 percent.

From a trend standpoint, retail volumes are still 6% sub end 2021 highs. At the margin, the result paints a more resilient consumer spending picture, particularly given the detail in terms of where the strength was in some of the spending categories. Note we get the next RBNZ meeting next Wednesday.

JAPAN DATA: Inflows Into Japan Stocks Stretches To 8 Straight Weeks

Offshore investors continued to buy Japan stocks last week. We saw ¥285.9bn in further net inflows. This stretches the weekly inflows run to eight consecutive weeks, albeit with last week's pace of inflows slightly down on the prior week.

- Offshore investors returned to local debt markets, with ¥422.6bn in inflows last week, but the trend remains mixed on a week to week basis. We have had net selling since mid September, following a couple of large outflow weeks.

- In terms of Japan outflows to the rest of the world, purchases of offshore debt were close to flat.

- Japan net buying of offshore stocks returned last week (¥120.5bn), which has been the general trend going back to late September.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending Nov 17 | Prior Week |

| Foreign Buying Japan Stocks | 285.9 | 384.2 |

| Foreign Buying Japan Bonds | 422.6 | -296.1 |

| Japan Buying Foreign Bonds | 2.5 | -65.8 |

| Japan Buying Foreign Stocks | 120.5 | -73 |

Source: MNI - Market News/Bloomberg

FOREX: Greenback Marginally Firmer, Moves Limited In Asia

There have been narrow ranges across G-10 FX on Friday, with little follow through on moves thus far. In the cross asset space WTI is down ~0.8% as discord within OPEC+ forced the group to delay an upcoming meeting. US Cash Tsys have reopened after being closed for Thanksgiving and are 4-6bps firmer. BBDXY is marginally firmer.

- AUD/USD is little changed from opening levels last printing at $0.6565/70. Technically the trend needle points north, resistance comes in at $0.6589 high from Nov 21. Support is at $0.6453, low from Nov 17.

- Kiwi is a touch higher however NZD/USD has observed a $0.6045/55 range in Asia. On the wires early in the session Q3 Retail Sales ex Inflation printed at 0.0% Q/Q, the prior read was revised a tick higher to -0.9% Q/Q. A fall of 0.7% had been expected.

- Yen is marginally firmer, USD/JPY is down ~0.1% however we remain comfortably above the ¥149 handle. The pair looked through this morning's mixed CPI and PMI report's. Resistance comes in at ¥150.00, the 20-Day EMA, and support is at ¥147.15, low from Nov 21.

- Elsewhere in G-10 CAD is down ~0.1% and EUR and GBP are little changed.

- The docket is light in Europe today, further out we have flash US S&P Global PMIs.

EQUITIES: HK/China Soften, Mixed Trends Elsewhere

On balance, regional equities are lower in first part of Friday trade. Hong Kong and China markets are weaker, unwinding some of the optimism seen around policy support for the property sector in recent sessions. US futures are a touch higher, but have tracked tight ranges overall. Eminis were last near 4570, while Nasdaq futures were around 16062.

- US yield have pushed higher as cash markets have re-opened following the Thanksgiving holiday, but this looks to be largely catch up with higher EU yields from Thursday (as Germany looks to suspend its debt brake). This hasn't impacted sentiment too negatively though in the equity space.

- At the break, the HSI is off 1.38%, while the China CSI 300 index is down 0.53%. A Bloomberg gauge of China property developers is down around 1% at this stage, after rallying around 15% in the first 4 sessions of this week. Banks are also under pressure amid concerns around unsecured loans to developers (see this BBG link for more details).

- Earnings headwinds in Hong Kong is the other factor cited, with some disappointment around Q3 outcomes (see SCMP here).

- Elsewhere, Japan markets have returned, with the Topix up around 0.65% at this stage. The ASX 200 has also crept higher, +0.25%.

- Most other markets are weaker at this stage, although losses aren't large. The Kospi is down 0.50%, while The Taiex is close to flat.

- In SEA, only the Philippines is marginally higher at this stage.

OIL: Higher For The Week, All Eyes On Nov 30 Opec Meeting

Brent sits unchanged versus end Thursday levels, last near $81.40/bbl. Earlier highs were just above $81.80/bbl. The benchmark hasn't been back above $82/bbl, since Wednesday's plunge on headlines around the delay of the OPEC+ meeting. At this stage Brent is around 1% higher for the week, which would be its first gain in 5 weeks. WTI is tracking near $76.50/bbl in recent dealings, following a similar trajectory to Brent (+0.80% higher for the week).

- Focus remains on the Nov 30 OPEC+ meeting. An Angolan official stated the country’s intent to remain in OPEC, somewhat settling the markets Thursday.

- Still, Nigeria and Angola are the main nations pushing for higher production quotas, disrupting normal OPEC+ meeting proceedings. Both nations are aiming to boost their production in the short term.

- Saudi and Russia are expected to sustain or deepen cuts into 2024 when they meet November 30.

- In terms of levels, key short-term resistance for Brent is seen at $83.97 (Nov 14 high). For WTI, resistance is seen at $78.55 after which lies a key short-term $79.65 (Nov 14 high).

GOLD: Tracking Sideways, Up For The Week, But Resistance Still Evident Above $2000

Gold has largely drifted sideways in the first part of Friday dealing. The precious metal was last near $1992, little changed from Thursday closing levels. We sit higher for the week at this stage ($1980.82 last week's closing level), but Gold has been within fairly tight ranges over recent sessions.

- Resistance is evident on moves above $2000. The bull trigger at $2009.4 (Nov 7/Oct 27 high) having come close in earlier sessions this week.

- Dips sub $1990 have been supported on the downside. Note the 20-day EMA sits back near $1973.

- The firmer core yield backdrop hasn't impacted sentiment much, although the USD is only marginally above recent lows, a gold support point in the past week.

ASIA FX: USD/Asia Pairs Mostly Higher To End The Week

Most USD/Asia pairs are higher in Friday dealings. Less positive regional equity sentiment, particularly in HK/China has weighed, while firmer core yields is a likely additional headwind. THB and KRW have lost the most ground this week, CNH has outperformed, although it has consolidated in recent trading. Next week we have the official China PMIs for Nov, along with the BOK and BOT decisions, among the highlights.

- We saw another step down in the USD/CNY fix (7.1151), a sharp drop over the past week. However, there wasn't much follow on USD/CNH selling, with the pair back above 7.1500 this afternoon (earlier lows were 7.1426). Onshore equities are under pressure, as well as HK markets. Local banks are struggling amid concerns over unsecured loans to property developers, which has been reported to be part of the latest efforts to help the ailing sector.

- 1 month USD/KRW has pushed higher in Friday dealings. The pair last near 1303, around Thursday session highs. Local equity sentiment has weakened, the Kospi off around 0.60% at this stage. Higher core yields have also likely weighed at the margin. The won rally has stalled this week, unable to sustain breaks sub 1300.

- USD/THB sits off session highs, last near 35.40. Earlier highs were at 35.48. This is fresh highs back to mid November, from last week. Baht is down around 0.40% for the session so far, and -0.90% for the past week, leaving it the worst performer in the EM Asia FX space over this period. Recent weakness in Thailand equities hasn't helped THB sentiment, while offshore investors have remained net sellers of local shares this week, -$145mn in net outflow so far. The Government is pushing ahead with its digital wallet plan, while the BoT has stated the country needs to preserve monetary and fiscal space.

- The SGD NEER (per Goldman Sachs estimates) is little changed this morning, we remain a touch off recent cycle highs. The measure sits ~0.3% below the top of the band. USD/SGD is dealing in a narrow range above the $1.34 handle this morning. The pair is ~0.5% above November lows as some of the month's losses have been trimmed in recent dealing. Weaker regional equities and firmer US Tsy Yields are weighing on sentiment in Asia today. Industrial Production rose 7.4% in October, a fall of 2.3% Y/Y had expected.

- The Ringgit has opened dealing little changed from yesterday's closing levels in a muted start to today's session. The wider USD/Asia space is also flat and ranges have been narrow. CPI in October ticked lower to 1.8% Y/Y, it had been expected to hold steady at 1.9%.

- The Rupee has opened dealing little changed in a muted start to Friday's dealing. US Tsy Yields have ticked higher this morning and Oil is pressured. Looking ahead, the highlight of next week's docket is Q3 GDP print on Thursday. A rise of 6.9% Y/Y is expected, the prior read was 8.0%. Also due on Thursday is the October Fiscal Deficit and the Eight Infrastructure Industries survey. On Friday S&P Global Mfg PMI crosses.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/11/2023 | 0700/0800 | *** |  | DE | GDP (f) |

| 24/11/2023 | 0700/0800 | ** |  | SE | PPI |

| 24/11/2023 | 0800/0900 | ** |  | ES | PPI |

| 24/11/2023 | 0900/1000 | *** | | DE | IFO Business Climate Index |

| 24/11/2023 | 1000/1100 |  | EU | ECB's Lagarde participates in "Europe in the Future" event | |

| 24/11/2023 | 1300/1400 | | EU | ECB's De Guindos remarks and Q&A | |

| 24/11/2023 | 1330/0830 | ** |  | CA | Retail Trade |

| 24/11/2023 | 1330/0830 | ** |  | US | WASDE Weekly Import/Export |

| 24/11/2023 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 24/11/2023 | 1445/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 24/11/2023 | 1445/0945 | *** | | US | S&P Global Services Index (flash) |

| 24/11/2023 | 1600/1100 | | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.