Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

JPY

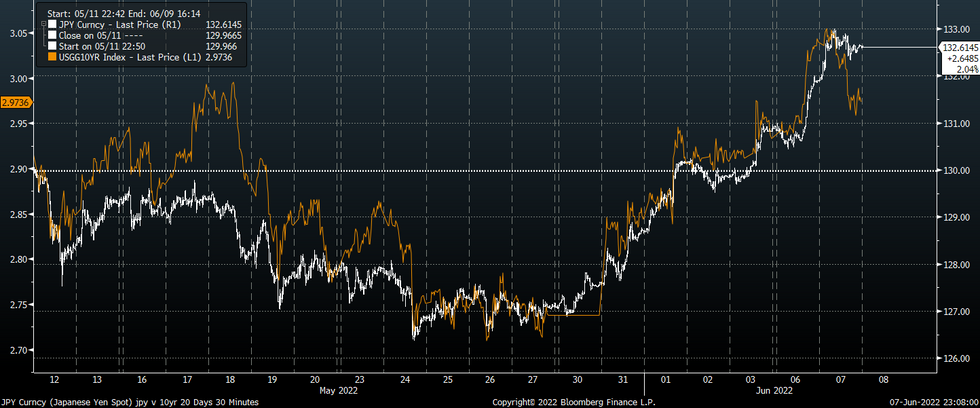

Demand for USD/JPY emerged in early Tokyo trade Tuesday and intensified as BoJ Gov Kuroda reiterated his ultra-dovish policy mantra, with the pair printing a fresh two-decade high at Y133.00. The rate managed to remain afloat through the rest of the day despite a pullback in U.S. Tsy yields (see fig. 1).

- A decline in the VIX index to 24%, the lowest level since Apr 22, may have served as an offset to lower U.S. Tsy yields (carry trades are supported by lower equity vol). But if U.S. Tsy yields keep correcting, we may well see USD/JPY losing ground.

- In addition, the yen remained pressured via other currency pairs as the BoJ remains the lone dove among major central banks. A hawkish RBA rate decision pushed AUD/JPY above Y96.00, while EUR/JPY soared above Y142.00 ahead of this week's ECB meet.

- USD/JPY 1-month risk reversal extended gains after rising above par for the first time since May 11 on Monday, as bullish sentiment among option traders kept strengthening.

- Final quarterly GDP figures and monthly BoP current account balance will hit the wires shortly, with Eco Watchers Survey due later in the day.

- Yen weakness persists this morning, with USD/JPY trading +19 pips at Y132.78 as EUR/JPY rips through yesterday's best levels. Should USD/JPY break above round figure/ Apr 4, 2002 high of Y133.00/11, bulls could set their sights on Apr 1, 2002 high of Y133.84. Bears keep an eye on the 50-DMA, which intersects at Y127.96.

Fig. 1: USD/JPY vs. U.S. 10-Year Tsy Yield (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok