Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

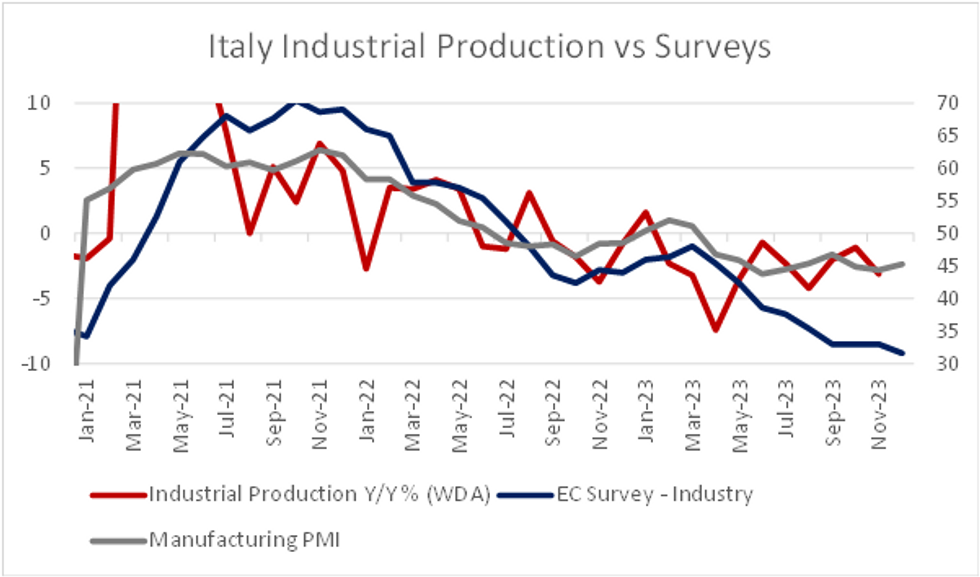

In contrast to the Spanish reading out earlier Thursday, Italian November industrial production was weaker than consensus on a monthly basis. Seasonally and working day adjusted IP was -1.5% M/M (vs -0.2% cons; -0.2% prior), while the 3m/3m growth rate was -0.8% (vs -0.3% prior).

- The SWDA index is now almost -7.5% lower than the post-Covid peak in April 2022, just slightly less of a decline than Germany's where production is almost -8% below December 2020 levels. The annual rate (in WDA terms) was negative for the 10th consecutive month, at -3.1% Y/Y (vs -1.1% prior).

- The outlook for IP in December, as implied by the latest survey data, suggests continued weakness. The EC Industry survey measure fell to -9.2 points (vs -8.5 prior), the 17th consecutive negative month, with expected production component turning negative.

- Meanwhile, the December manufacturing PMI remained sluggish at 45.3, with respondents citing "domestic and foreign demand weakness" as drivers for output and new order contractions.

- The sub-components of the IP index were all negative on a SWDA monthly basis, with consumer and intermediate goods falling -1.8% M/M each (these components make up 59.1% of the overall index). On a WDA annual basis, these components both fell -5.7% Y/Y.

- Capital goods production was down -0.2% M/M SWDA though up +0.6% Y/Y WDA, while energy was -4.0% M/M SWDA and +1.0% Y/Y WDA).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok