Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

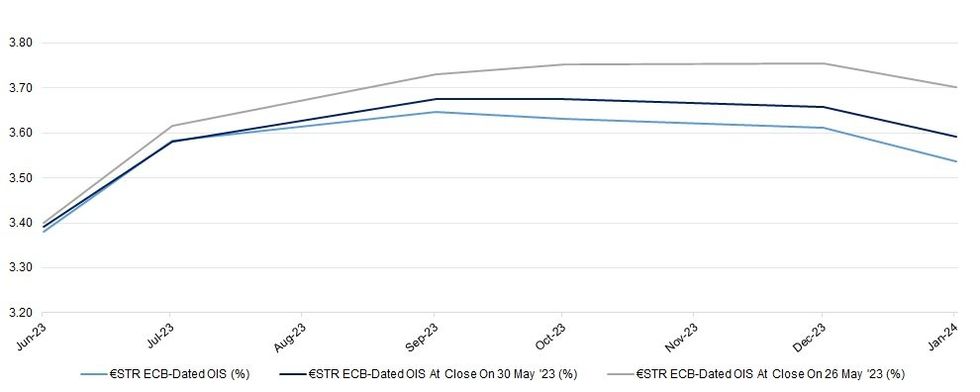

NRW CPI dynamics out of Germany help ECB-dated OIS adjust lower in early Wednesday trade. That leaves ~50bp of hikes priced in before terminal rate levels are reached (3.75% in ECB deposit rate terms), with terminal rate pricing shifting lower by 10bp vs. Friday’s close, as well as moving forwards to September vs. December.

- A quick reminder that the NRW CPI release covers the most populous region in Germany. The print saw a 0.2% M/M dip alongside a slowing in the headline Y/Y reading to +5.7% from +6.7% in April. The national reading was expected to print at +0.2% M/M & +6.5% Y/Y (per the BBG survey), meaning that this state CPI represents a softer than expected reading.

- State and preliminary CPI data out of Germany will continue to filter in on Wednesday, with French & Italian CPI readings further bulking out the regional docket. ECB speak from Villeroy, Muller & Visco is also due, as is the full release of the Bank’s latest Financial Stability Review.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jun-23 | 3.380 | +23.2 |

| Jul-23 | 3.583 | +43.5 |

| Sep-23 | 3.647 | +49.9 |

| Oct-23 | 3.631 | +48.3 |

| Dec-23 | 3.611 | +46.3 |

| Jan-24 | 3.537 | +38.9 |

source: MNI - Market News/Bloomberg

source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok